►

From YouTube: OKC Post Employment Benefit Trust - February 13, 2023

Description

No description was provided for this meeting.

If this is YOUR meeting, an easy way to fix this is to add a description to your video, wherever mtngs.io found it (probably YouTube).

A

A

Today

we

have

some

items

for

consideration,

including

the

presentation

of

the

quarterly

investment

report

for

the

oh,

don't

we

have

minutes

to

consider.

Maybe

I

went

too

far.

Oh

first

item

on

our

business

today

is

approval

of

minutes

for

the

November

14

2022

Oklahoma

City

Post

employment

benefits

trust

meeting.

So

if

I

could

entertain

a

motion

on

that

item,.

A

And

the

minutes

have

been

approved,

so

the

next

item

on

our

agenda

is:

are

the

individual

items

for

consideration?

First,

we

have

the

presentation

of

the

quarterly

investment

report

for

the

period

ended,

December,

31st,

2022,

or

also

receiving

our

monthly

investment

reports

for

November

30th

December

31st

and

January

31st

2023

I'd

like

to

welcome

Doug

Anderson

to

the

podium

and

Doug.

What

do

you

have

to

tell

us

today,

good.

B

Exactly

yeah

and

I

think

that

the

headlines

are

strange

right

now

to

say

the

very,

very

least,

but

the

fourth

quarter.

We

saw

some

improvements

in

the

market.

Some

stabilization

in

the

markets

in

January

was

also

a

good

month,

so

we'll

go

through

that

as

well.

First

off

on

this

quarter-

or

this

is

our

year-end

report

and

so

on.

The

next

slide,

you'll

see

perfect

you'll,

see

a

letter

from

our

chairman

and

CEO

Mike

Welker

thanking

our

clients,

primarily

that's

the

most

important

thing.

B

B

Is

the

right

time

of

year

to

do

this?

Yeah?

Yes,

please

let

me

know

I'd

be

happy

to

to

take

everyone

down

there,

so

that's

the

the

gist

of

that.

The

next

slide

is

our

organization

chart

again

you

can

see

93

people

you

can

see

on

the

upper

left-hand

side.

That's

our

partnership!

Those

are

the

partners

of

the

firm.

Our

firm

has

a

distinct

leadership

structure

where

it

is

separate

from

most

of

the

Consulting

duties.

B

Next

slide,

please-

and

one

more

so

here

we're

going

to

start

talking

about

the

market,

environment

and

2022

is

a

very

difficult

year.

There's

no

two

ways

about

it:

we

started

with

a

hint

of

inflation

during

January

that

seemed

to

be

somewhat

pacified,

but

then

in

February

I

think

it

was

very

close

to

this

date.

B

Last

year,

I

think

I,

remember

talking

about

the

potential

of

Russia

invading

Ukraine

and

saying

it's

a

very

remote

possibility,

but

of

course

that

did

happen

and

that

defined

a

lot

of

the

year

last

year

between

that

and

the

balance

between

inflation

and

unemployment

in

the

United

States

last

year

was

a

a

transitive

year.

We

saw

a

lot

of

things

changing

the

next

slide

shows

you

performance

in

the

markets,

the

upper

side

there,

the

quarterly

performance.

You

saw

that

the

fourth

quarter

of

the

year

had

a

nice

recovery.

B

That's

seven

percent

seven

point:

six

percent

return

for

the

s

p:

you

can

see

the

international

Equity

indexes

are

in

Gray,

so

they

had

a

great

fourth

quarter.

Part

of

that

was

appreciation

of

share

prices

on

foreign

markets.

A

large

part

of

that

was

also

the

depreciation

of

the

dollar

versus

other

currencies.

The

markets,

the

world

economy,

seemed

to

stabilize

a

bit

during

the

fourth

quarter

and

saw

the

dollar

trade-off

versus

other

currencies.

We

actually

had

positive

return

on

bonds

during

the

quarter

and

then

T

bills

or

cash

at

point

nine

percent.

B

But

then

we

looked

back

at

the

last

year

and

last

year's

it's

a.

This

is

a

very

difficult

picture

to

look

at

normally

when

you

see

equities

the

s

p,

Etc

down

19

percent,

usually

in

that

case,

lower

risk

assets,

I.E

bonds,

that

lower

segment

in

green

is

a

positive

return.

Those

are

our

two

major

asset

categories

here,

the

blue

and

the

green,

and

both

of

them

were

down

tremendously.

If

you

look

at

this,

the

only

Market

I

guess

you

could

say

that

was

positive-

was

t-bills

up

one

and

a

half

percent.

Now

remember.

B

B

I'll

we'll

take

another

look

at

that

in

a

moment,

but

going

on

to

the

next

slide,

you

see

performance

value,

outperformed

growth,

even

during

the

fourth

quarter,

but

you

look

out

over

the

last

year

value,

although

at

a

loss,

outperformed

growth

by

tremendous

margins

and

I

think

I

remember

two

years

ago

saying

this

growth

Market

rally

the

Fang

stocks,

that

was

the

buzzword

at

the

time:

Facebook

Amazon,

Apple,

Netflix

and

Google.

This

cannot

go

on

forever,

because

75

percent

of

the

Market's

return

was

generated

by

those

five

companies,

and

that

was

unsustainable.

B

It

looked

like

it

would

go

on

forever.

It

felt

like

it

would

probably

go

on

forever

and

if

you

were

going

to

take

a

look

at

value

stocks,

I.E,

Banks,

insurance,

company

and

energy,

you

would

have

thought.

Why

are

we

looking

at

this?

Those

are

those

companies

are

past,

their

Prime

we'll

never

have

any

they'll,

never

generate

the

returns

that

these

technology

companies

will

now

go

on

to

the

next

slide

and

we

can

see

what

happened

to

those

technology

companies.

B

So

when

we

look

at

the

Russell

1000

communication

Services

down

for

the

year,

which

is

the

lighter

column,

40

percent,

40

percent

of

that

sector

is

I,

believe

Facebook

and

Amazon

I.

Think

they're

quote

they're

classified

very

strangely,

but

40

of

that

index

is

down,

but

that

an

entire

index

is

down

40

percent.

On

the

year

you

look

at

consumer

discretionary.

Obviously,

a

slowing,

uncertain,

Market

environment

they'll

sell

off

also

down

36

percent

Consumer

Staples.

B

We

have

to

have

those

so

they're

down,

just

not

as

much

not

nearly

as

much

and

then

energy

the

one

standout

player

right.

If

there

was

one

thing

that

folks

were

very

worried

about

last

year

and

we

saw

Energy

prices

go,

you

know

above

a

hundred

dollars

a

barrel

of

WTI,

we

saw

natural

gas

prices

explode

to

that's,

probably

how

to

go

much

higher,

very,

very

yeah

I,

don't

I!

Don't

like

this?

B

Let's,

just

let's

use

a

different

adjective

on

that

adverb

sorry,

but

as

we

we

verb

as

as

it

went

higher

as

pipelines

had

problems

under.

You

know

see

if

we

had

other

issues

about

how

is

Germany

and

the

rest

of

of

Europe

going

to

heat

themselves,

much

less

run

into

this

run.

Industry

we

saw

natural

gas

prices

go

extremely

higher

in

the

United

States.

B

We

saw

them

go

from

under

two

to

about

nine

for

a

brief

period

of

time,

the

price,

but

in

Europe

we

saw

them

go

over

a

hundred

and

twenty

dollars

for

the

same

price

equivalent

in

the

United

States.

Now

it's

down

to

less

than

20,

because

the

winter

has

been

very,

very

mild,

but

I

think

long

story

short

the

things

that

led

the

market

two

years

ago

in

simpler

times

in

more

stable

times,

if

you

will

definitely

have

taken

the

back

seat

during

the

last

year.

B

If

you

look,

there

were

two

sectors

last

year

that

had

positive

returns

in

the

Russell

1000

energy

up

64

and

a

half

percent

right

leagues

ahead

of

everybody

else,

and

then

utilities,

which

is

the

most

defensive

sector

up.

1.3

percent

utilities

are

paid,

pay

a

decent

yield,

so

it's

probably

around

four

percent

now,

but

even

they

on

a

capital.

Appreciation

came

back

a

little

bit

last

year.

So

when

you

look

at

the

U.S

Equity

market,

energy

or

nothing,

that

was

the

only

place

that

performed

well.

B

So

next

slide

shows

the

performance

of

the

top

10

weighted

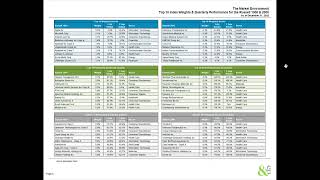

stocks.

And

if

you

look

at

these

Apple

down

26

Microsoft

down

28

for

the

one-year

column

there

Amazon

down,

50

percent

Berkshire

Hathaway

can't

get

much

more

basic

than

that

right.

3.3

percent,

positive

return

and

then

alphabet

which

is

Google

down

39.

B

If

you

look

there

meta

is

not

even

in

the

top

ten

anymore.

That's

Facebook

Facebook

was

down

70

last

year.

It's

come

back

quickly

this

year,

but

it

was

one

of

the

biggest

losers.

If

you

look

at

the

bottom

10

performers,

you

can

see

some

really

dramatic

losses

here,

and

these

are

companies

that

we

were

looking

at

a

few

years

ago.

Being

industry

leaders

right

carvana

right,

that's

the

you

know

we'll

buy

whatever

used

car

you

have

and

then

we'll

resell.

B

It

wework

one

of

my

favorites

right

they're,

going

to

re

completely

reconfigure

the

office

real

estate

market

in

in

the

world

down

83

percent

last

year

and

then

Tesla

down

65

percent.

Now

we

look

at

the

top

performers

Therapeutics.

Obviously,

some

of

those

are

great.

You

see

discount

retailers

like

Burlington,

and

then

you

see

Halliburton

right

and

Halliburton

was

a

great

performer

during

the

quarter,

but

a

great

performer

for

the

year.

So

I'm

calling

it

Back

to

Basics

I'm

saying

that

cash

is

an

investment.

An

option.

B

Matthew

and

I

have

talked

about

the

cash

that

is

being

held

outside

of

the

of

the

Investment

Portfolio,

because

if

you

look

at

checking,

accounts

balances

they're

getting

about

half

a

percent

income

right

now

or

yield

on

them,

but

the

money

market

fund

that

it's

invested

in

it's

not

in

cash

money.

Market

fund

is

a

little

bit

more

than

four

percent

and

if

you

think

on

a

million

dollars,

I'm

going

to

get

a

half

percent

or

four

percent,

that's

pretty

meaningful

increase,

and

luckily

it's

been

in

there

the

entire

year.

B

So

next

slide

International

Equity

performance,

sort

of

paralleled,

the

U.S,

except

for

it's

a

little

bit

worse,

the

first

three

quarters

of

the

year

and

a

little

bit

better

during

the

fourth

quarter

of

last

year.

Big

picture

right

now,

when

it

comes

to

International

markets,

is

obviously

China.

China's

reopening

China

coming

back

into

the

market,

is

going

to

have

supply

and

demand

implications,

but

right

now

I

think

that

one

thing

in

the

back

to

basics,

the

world

is

short

oil

production

capacity.

B

If

China

comes

back

on

strong,

like

they,

they

might

be

expected

to,

so

there

will

be

Supply

pressures.

Europe

was

able

to

get

natural

gas

to

heat

themselves

this

year,

but

the

other

effect

was

there

were

other

countries

that

weren't

able

to

like

Thailand

weren't

able

to

get

the

natural

gas

that

they're

normally

used

to

because

they

were

bid

out

by

Europe.

So

next

slide

I'm

not

going

to

go

over

this

I'm

going

to

go

one

more

fixed

income.

This

will

be

a

year

that

lives

in

infamy

in

the

bond

markets.

B

Bonds

are

simple,

Securities

right.

They

have

a

it's

a

loan

that

you're

making

to

someone

in

a

securitized

basis.

A

bond

is

simple

right.

You

don't

have

earnings,

you

don't

have

margins,

you

don't

have

anything

else.

You

have

I'm

going

to

loan

someone

or

somebody

or

something

a

hundred

dollars

for

a

specified

period

of

time

during

that

period

of

time,

I'm

going

to

be

paid

a

rate

of

interest

and

at

the

maturity

of

that

that

period

of

time

I'm

going

to

get

my

hundred

dollars

back.

B

That's

it

very

simply

in

cases

like

that,

Securities

like

that,

we

do

not

often

see

bonds

going

down

this

much

right.

I

think

I

mentioned

the

two

times

in

American

history.

Where

they've

been

down

this

much

and

they

were

existential

threats

to

the

United

States.

It

was

not

a

a

year

where

we

had

seven

percent

inflation.

It

was

like

we

don't

know

if

the

government's

going

to

be

around

to

pay

pay

these

off

when

they

come

due.

B

So

I

think

the

Bond

Market

may

have

over

over

overreacted

to

some

of

the

issues,

but

that's

also

what

the

bond

market

does.

We

look

at

the

quarter.

Things

finally

started

to

come

around

nicely,

but

the

aggregate

Bond

index

for

the

year

was

down

13,

that's

our

normal.

Our

main

Benchmark

here

treasuries

were

down

12

and

a

half

percent

mortgage

is

down

11.8

corporate

bonds

down

15-8

high

yield

we're

down

11-2,

which

is

less

and

there's

a

couple

of

reasons.

Why?

B

But

but

Ironically

in

a

year

that

the

bond

market

sold

off,

you

had

corporate

bonds,

there

were

investment

grade

and

he

had

corporate

bonds

that

were

below

investment

grade

below

investment

grade

bonds

performed

better

that's

because

they

have

shorter

duration

and

they

pay

more

income,

and

that's

why

they

did

better.

It

was

a

year

that

in

the

next

slide,

please,

where

we

saw

the

yield

curve

we

on

the

bottom

there

you

can

see

the

treasure

yield

curve.

B

This

shows

you

the

yield

of

Treasury

Bonds

on

various

maturities

at

four

different

dates,

so

the

first

one

or

the

lowest

one

is

the

is

331

of

last

year.

So

this

is,

you

know

the

very

beginning

of

the

interest

rate

hiking

cycle,

and

you

can

see

that

the

yield

curve

was

fairly

normal.

It

was

low,

but

it

was

fairly

normal

with

a

yield

of

25

basis

points

at

the

front

end

and

two,

and

about

two

and

a

half

at

the

30

year.

Now

look

at

the

yellow

line

there.

B

That's

very

interesting

where

the

one

month

went

from

25

basis,

points

to

about

425

basis

points.

That's

a

rapid

increase

in

interest

rates

by

the

Federal

Reserve,

trying

to

reduce

inflation

in

the

economy,

and

so

that's

one

thing.

The

other

thing

that's

very

interesting

here

is

that

the

yield

curve

is

inverted,

meaning

that

you

can

make

more

money

lending

someone

six

months,

then

you

could

lending

somebody

for

seven

years

right.

B

What

does

that

make

people?

Do

I'm

not

going

to

lend

money

to

anybody

for

seven

years,

I'm

going

to

do

a

very,

very

short

term,

and

so

that

has

a

slowing

effect

and

I.

Think

the

old

saying

is

that

an

inverted

yield

curve

is

predicted

seven

out

of

the

last

five

recessions,

meaning

it

does

not

always

precede

recessions,

but

it

usually

does

so.

This

is

some

sense

of

economic

slowing

in

the

future.

B

Just

because

the

way

the

markets

work

the

way

the

markets

fund

themselves,

so

that

is

the

long

and

short

story

of

the

market

environment.

If

we

could

go

to

the

portfolio

report

itself,

like

I

said,

this

is

a

very

difficult

year

down

17

percent.

This

is

one

of

the

most

difficult

years

that

I've

ever

seen

as

an

investor

as

an

advisor

to

folks

like

yourselves,

this

feels

as

bad

as

the

2008-2009

period.

B

The

great

financial

crisis,

where

it

felt

like

the

world's

Financial

system,

was

going

off

a

cliff

and

we

didn't

know

if

it

was

going

to

be.

There

I

think

it's

going

to

be

there.

We

might

have

a

slower

economy.

This

year

we

started

with

interest

rates

very,

very

low,

which

was

punishing

for

the

bond

portfolio.

But

if

there's

one

positive,

that

I

will

say

out

of

this

expected

returns

for

60

40

portfolios

at

the

beginning

of

last

year,

given

how

low

bond

yields

were

and

how

high

or

how

expensive

stocks

were.

B

B

So

I

guess

that's

the

shiny

side

of

the

penny

that

we

just

picked

up

on

the

sidewalk

there,

but

that's

we're

we're

not

invested

exclusively

in

those

two

asset

classes.

We're

Diversified

beyond

that

and

I

think

that

this

year

it

helped

us

in

ways.

I

certainly

didn't

expect.

So

next

slide

Will

Go

On.

Here

you

can

see

that

over

time

the

strategy

has

worked

right.

The

long-term

asset

allocation

has

increased

the

value

of

the

portfolio

at

this

point

at

the

end

of

last

year

was

85.6

million

dollars.

So

this

is

December

31..

B

This

goes

all

the

way

back

to

2009.

We

started

with

6.018

million

dollars

and,

as

we

ended

the

year

85.6

over

that

period

of

time

we've

seen

151

million

dollars

contributed.

We've

seen

105

million

dollars

pulled

out.

We

have

seen

gains

on

market

value

or

capital

appreciation

of

33.3

million

dollars.

The

ending

market

value

is

right.

There

we've

also

seen

income

of

11.1

million

dollars

and

hopefully

in

the

future

we

will

see

a

larger

contribution

of

income

to

the

total

return

here.

So

over

the

entire

period

of

time,

the

cumulative

return

has

been

140

percent.

B

B

That

was

the

first

time

we

saw

that

now

we

saw

a

strong

rebound

during

the

fourth

quarter,

thankfully,

and

that

52

million

dollars

is

the

net

I.

Guess

you

would

call

that

the

Corpus

that

has

been

or

the

net

of

all

positive

cash

flow

over

time,

so

the

amount

in

total

contributed

is

52

million

dollars.

We

still

have

85.6

after

what

I

would

consider

one

of

the

worst

years

that

we've

ever

seen

next

slide.

Please

asset

allocation

has

been

roughly

stable.

It's

been

stable

over

time.

B

You

can

see

we

started

out

slow

with

less

domestic

equity

and

we

we

supplanted

that

with

fixed

income,

because

again

2009

was

a

period

where

we

didn't

know

what

was

going

to

be

happening.

Next

next

slide

is

our

asset

allocation

here,

so

we

have

63

percent

domestic

Equity

16

core

fixed

income.

We

have

11

percent

in

non-us

equities,

so

our

total

allocation

to

equities

is

about

75

percent.

We're

active

that

way.

B

We

are

more

in

equities

than

a

lot

of

folks

and

actually,

ironically,

last

year,

having

16

of

fixed

income

didn't

help

us

as

much

as

we

thought

it

would.

So

that's

one

of

the

reasons

that

we

have

that

return.

You

can

see.

We

have

a

couple

of

other

fixed

income

allocations

and

then

point

two

percent

in

cash.

This

is

Cash

in

the

Investment

Portfolio

Matt.

How

much

is

in

the

outside

of

the

Investment

Portfolio.

B

So,

outside

of

this,

we

have

the

cash

buffer,

which

is

about

two

million

dollars

which

which

allows

us

to

not

to

have

to

hit

this

portfolio

on

a

quarter

by

quarter

basis.

The

next

slide,

please

is

our

manager

allocation.

Here

you

can

see

largest.

Is

our

S

P

500

Index

Fund,

then

our

International

Equity.

Then

we

have

small

cap,

U.S,

equities,

mid

cap,

us

equities

and

then

Bond

portfolios

managed

by

limit

sales

double

line

Hoisington.

B

Well

then,

we

have

our

mid

cap

portfolio

and

then

the

Lord

Abbott

high

yield,

so

at

the

very

top

of

the

portfolio

is

a

passive

exposure

to

the

U.S

Equity

Market

bonds.

Much

lower,

we

have

half

of

our

mid

cap.

Exposure

is

indexed

because

we

kind

of

went

round

and

round

trying

to

find

the

right

manager

there

for

a

while

all

of

our

International

Equity.

All

of

our

small

cap

is

actively

managed,

as

is

our

Equity

portfolios.

Next

slide,

please.

B

C

D

C

D

B

And

trustee

Barry,

that's

that's

been

an

I

guess,

a

evolving

area

and

I

think

it's

smart

to

have

that

much

cash

on

the

outside,

because

in

a

worst

case,

environment

I

would

rather

have

that

and

not

have

to

tap

assets

when

they're

down.

So

looking

at

the

portfolio

here,

not

a

lot

of

surprises

right.

You

have

more

Equity

than

most

funds

out

there,

because

this

plan

has

a

very

long

time.

Horizon,

possibly

exceeding

our

own

lifespans.

For

the

quarter

portfolio

was

great.

It

had

Equity

exposure,

it

did

very,

very

well.

B

16.95

now

going

to

the

quarter

going

back

to

the

quarter,

you

can

see

that

our

fixed

income

exposure

was

up

1.1

percent.

We

had

widely

dispersed

returns

there

Loomis

sales,

2.81

percent-

well,

thankfully

all

but

one

we're

we're

positive.

Second

percentile

double

line

bond,

which

is

a

more

macro

oriented

portfolio

1.13,

but

they

ranked

in

the

92nd

percentile

and

then

Lord

Abbott

down

3.75

in

the

71st

first

percentile

and

then

also

I

I.

B

Don't

has

said

irony

once

I,

don't

want

to

use

that

word

again,

but

surprisingly,

Hoisington

was

down

1.95

and

they

had

an

absolutely

rotten

year.

Last

year,

they're

economists,

the

biggest

economic

surprise

last

year,

was

that

inflation

was

not

transitory.

It

fooled

the

Federal

Reserve,

it

fooled

the

treasury

Department,

it

fooled

Wall

Street.

It

fooled

these

folks

too,

although

their

rationale

still

appears

to

be

sound

going

forward

because

they

are

expecting

a

Slowdown,

it

did

not

help

their

portfolio

a

bit.

That's

why

we

have

a

reasonably

small

allocation

here

and

in

Market

environments.

B

In

the

past,

where

equities

went

down,

this

portfolio

went

up

in

the

opposite

Amer.

If

the

market

was

down,

equities

were

down

20.

This

portfolio

would

be

up,

20

I'll

show

you

and

an

example

of

that

in

just

a

moment,

but

in

this

case

because

inflation

was

driving

the

market

uncertainty

on

the

equity

side,

it

also

hurt

this

portfolio,

which

is

invested.

A

hundred

percent

in

U.S

treasury

bonds.

B

B

B

This

is

one

part

of

the

picture

that

you

don't

see

because

last

year

was

so

awful.

Hoisington

has

always

been

a

very

volatile

manager,

they

own

long

duration,

U.S

treasuries,

which

have

the

highest

volatility

within

the

bond

market.

Sometimes

that's

bad

volatility.

Sometimes

it's

good

volatility.

So

you

look

down

here.

You

can

see

the

year

to

date,

gosh

I,

hope,

I,

never

see

a

return

like

that

out

of

the

bond

market,

anything

that

pays

interest

and

has

maturity

date,

much

less

U.S

treasuries.

I.

Don't

ever

want

to

see

that

again,

but

you

look

at

2021.

B

They

were

down

4.9,

which

was

bad

too,

but

you

look

at

2020.

You

look

at

2019.

You

look

at

those

returns.

That's

what

they're

capable

of,

unfortunately,

those

two

years

that

we've

had

recently

completely

obliterate,

that

from

the

record

that

we

look

at.

If

we

stop

it

and

look

back

from

12

31.,

so

it's

unfortunate

that

they

were

down

that

much,

but

they

do

have

some

utility

in

the

future.

I

want

to

make

sure

that

they

know

that

we're

watching

them

very

carefully.

So.

B

B

This

this

happens

to

be

probably

the

simplest

investment

strategy

that

we

have.

They

look

at

the

future

of

interest

rates,

which

is

the

future

of

inflation

and

they

construct

their

portfolio

to

produce

an

absolute

return.

Based

on

that

forecast.

They

expect

a

slowing

economy,

which

means

that

they

will

own

30-year

treasuries.

B

B

If

it

goes

interest

rates,

go

up,

one

percent

that

portfolio

will

be

down

18.

If

interest

rates

go

down,

one

percent

portfolio

will

gain

18.

So

it's

a

higher

volatility

strategy

and

in

other

cases,

I

mean

2020.

You

remember,

you

know

that

was

the

first

year

of

covid

and

the

equity

markets

went

down

dramatically.

They

went

the

opposite

direction,

but

these

are

all

great

questions

and

things

that

do

you

keep

me

up

at

night

about

Hoisington?

B

If

they're

not

on

the

watch

list,

they

definitely

should

be,

but

I

wanted

to

make

sure

that

we

had

the

whole

picture.

Endpoint

sensitivity

when

you're

looking

at

returns

is

real

right.

If,

if

before

we

turned

this

slide,

if

I

said

you

know,

they

were

up

20

in

2020

and

17

in

2019

that'd

be

hard

to

believe.

Looking

at

that,

2022

look

back,

but

it

is

the

case.

B

So

thank

you

for

your

patience

on

looking

through

that

one.

It's

a

it's,

not

a

simple

issue,

although

that

is

the

simplest

portfolio

we

have.

So

could

you

get

back

two

slides?

Please

thank

you.

So

that's

our

bond

portfolio,

our

Equity

portfolio

for

the

quarter,

was

up

8.41,

that's

for

the

year

down

17.57,

so

we

definitely

did

not

close

the

year

at

the

lows.

If

we

look

down

the

first

three

portfolios,

you

can

see

the

for

the

fourth

quarter

and

again

the

S

P

500

is

by

far

the

largest

one.

It's

almost

one.

B

It's

a

little

bit

more

than

one-third

of

the

assets.

31

million

dollars

up

7.56

percent

57

percentile,

which

is

about

what

we

would

expect

and

then

18.13

loss,

which

is

slightly

worse

than

the

Benchmark

again

acceptable

ranges

same

is

true

for

the

index

fund,

but

I

always

like

to

have

at

least

one

positive

thing

to

look

at,

and

that

would

be

Hotchkiss

and

Wiley

Hotchkiss

and

Wiley.

Two

years

was

the

one

who

was

investing

in

things

that

would

never

go

up

again.

Their

portfolio

is

unchanged.

They're

patient

portfolio

is

still

relatively

cheap.

B

B

They

don't

know

what

they're

doing

it's

time

to

to

get

rid

of

them.

If

we

do

need

to

take

money

from

a

portfolio

this

year,

this

will

be

the

one

right

we

will

be

taking

profits

from

it

and

that's

part

of

our

discipline.

So

the

next

slide

we're

going

to

go

on

to

two

of

the

other

Equity

portfolios

and

again

the

Stevens

small

cap

portfolio.

It

was

slightly

worse

than

their

Benchmark

over

the

last

three

years,

five

years

and

seven

years,

they're

above

median

and

their

Universe.

B

This

is

not

a

hyper

aggressive,

small

cap

growth

portfolio

and

we

like

it

that

way.

But

then

look

at

our

Causeway

International

value

fund,

remember

I,

said:

equities.

International

equities

came

back,

they

stormed

back

during

the

fourth

quarter

and

you

can

see

that

this

one

was

even

a

little

bit

more

than

that.

So

11

of

the

portfolio

is

up

22

percent

during

the

quarter.

B

That's

a

remarkable,

remarkable

Snapback,

but

also

remember

that

when

markets

recover,

when

they

turn

the

corner

from

bear

Market

to

bull

market,

it's

the

early

stages,

where

you

see

the

most

dynamic

returns

so

their

last

year,

they're

down

6.76,

which

is

20th

percentile.

That's

a

lot

of

of

time

spent

on

return.

So

you

have

any

more

questions

before

I

move

on.

B

Thank

you,

I'm,

going

to

jump

ahead

a

few

slides

here.

So

this

is

our

one

of

our

bond

portfolios.

A

little

bit

of

volatile

return.

You

can

see

that

the

returns

are

higher

on

the

scatter

plot,

but

they

are

a

bit

more

volatile

and

that

was

good

for

them.

Last

quarter

next

slide

shows

one

more

double

line,

which

is

a

little

bit

different.

They

don't

do

things

the

same

way:

they're

more

macro,

oriented,

meaning

they'll,

invest

more

in

mortgage

backs

and

have

interest

rate

strategies,

and

so

they

have

trailed

off

since

2020.

B

next

slide,

you

can

see

of

long

term

they're,

not

bad

they're,

really

close

to

their

Benchmark

next

slide.

Lord

Abbott!

This

is

our

High

Yield

Fund

again

it

was

one

of

our

better

performers

for

the

year

keeping

a

little

watch

on

them.

They

haven't

had

any

major

Personnel

changes,

but

I

don't

like

the

deterioration

when

the

blue

line

goes

down.

That's

that's

not

good,

so

keep

any

extra

eye

on

them

right

now

and

then

one

more

one

more

please.

So

this

is

the

Hoisington

experience

right.

B

We've

been

through

this

we've

had

them

for

some

time

they

are

either

the

best

or

the

worst

and

unfortunately,

I

wish

they

weren't,

always

the

worst

but

they're

a

hedging

portfolio

that

does

some

volatility,

has

some

positive

effects

on

volatility.

So

next

slide

we're

going

to

be

going

over

our

index

font.

You

can

see

this

doesn't

have

a

three-year

history,

because

remember

we

moved

to

a

share

class

that

was

extremely

cheap.

The

cheapest

Index

Fund

out

there

next

slide.

B

B

You

can

get

pretty

aggressive

in

small

cap

growth

I

tend

to

be

want

to

be

less

aggressive

in

the

really

volatile

asset

categories

and

that's

the

portfolio

that

we

have

here

and

and

I

like

it,

I

like

to

be

less

aggressive

with

higher

Returns

on

the

risk

return

plots

there,

the

the

the

scatter

plot,

with

the

two

dots

on

it,

there's

no

better

place

to

be

than

where

they

are

on

the

left

hand

side.

So

that

means

higher

return

and

lower

volatility.

That's

exactly

where

you

want

to

be

so.

B

I

think

we're

getting

really

close

to

the

end

here,

but

I

need

to

highlight

a

couple

more

things:

one

more

actually

Causeway

great

recovery

during

the

fourth

quarter.

Another

one

please!

So

let's

go

some

more

here,

another

one.

So

this

is

our

table

of

correlations

over

the

last

five

years.

This

means:

how

do

our

assets

perform

versus

one

another

when

one's

up

are

they

all

up,

or

is

there

one

or

two

that

are

down

in

the

last

year?

We

saw

really

high

correlations,

because

both

stocks

and

bonds

are

down.

That's

unusual.

B

If

we

look

at

the

column,

the

fourth

one

over

called

Hoisington.

If

you

take

a

look

at

that,

you

actually

have

negative

correlations,

albeit

small.

Let

me

explain

the

scale

the

scale

is.

1.00

means

perfect,

positive

correlation

right

if

one

asset

goes

up,

ten

percent,

the

other

one's

up,

ten

percent,

if

it's

negative

1.0,

that's

perfect,

negative

correlation,

meaning

if

one's

up

ten,

the

other

one

will

be

down

10.

B

we

like

to

have

negative

correlations

on

assets,

because

that's

diversification.

In

statistical

terms,

we

have

one

asset

Hoisington

that

they

have

negative

correlation

with

the

most

of

the

other

asset

categories

and

very

weak

correlation

with

the

total

fund

there,

you

will

notice

that

our

correlation

of

the

total

fund

on

the

bottom

line-

it

is

relatively

low

with

our

bond

portfolios,

but

it

is

much

higher

with

our

Equity

portfolios,

which

tells

you

equities,

are

the

asset

generating

asset

class

and

our

portfolio

is

geared

more.

B

So

next

slide

again

update

this

one

to

on

notice

or

on

watch

sorry

for

Hoisington

I

guess

they

would

be

surprised

if

we

weren't

taking

some

notice

on

the

portfolio

and

then

fees

fees

are

very,

very

important

here.

The

expense

ratio

on

a

weighted

average

basis

is

44

basis

points.

The

average

of

those

categories

when

we

total

it

up

at

our

asset

allocation

would

be

90

basis

points

which

means

that

we

are

46

basis

points

less

expensive

than

average,

so

we're

paying

half

of

average

in

the

mutual

fund

world.

B

Right

now

we

are

below

in

every

category

except

for

Hoisington,

which

is

slightly

above

and

makes

me

watch

them

even

closer.

So

at

the

total

market

value

at

the

end

of

the

quarter,

which

was

85

86

million

dollars,

the

annual

savings

through

selection

of

low-cost

funds

is

352

thousand

dollars.

So

that's

good

and

then

I

think

that

is

it

for

the

quarterly

report.

Can

we

go

another?

This

is

the

dashboard.

Where

essentially

no

surprise

is

here.

B

B

in

non-us

equities

and

even

and

even

fixed

income

was

at

a

nice

return

during

the

month

of

January.

Next

slide

shows

this

sort

of

spoiling

the

punch

here:

91.8

million

dollars

that's

one

month,

that's

a

good

month,

I'm

going

to

spoil

it

even

worse

and

say

that,

as

of

last

night,

we

were

still

at

91

million

dollars,

so

we've

maintained

that

that's

good

at

a

volatile

month

and

then

the

next

slide

shows

the

return.

So

the

month

7.18,

which

is

good

for

the

quarter,

we're

up

8.82

through

the

trail

in

one

year.

B

Can

you

believe

that

one

month

you

drop

one

month

off

and

we

go

from

a

loss

of

16.9

percent

to

a

loss

of

6.9

percent?

This

is

how

returns

work.

Remember

we're

looking

to

The

Far

Side,

the

three

years,

the

five

years,

the

since

Inception,

which

doesn't

change

much

at

all

over

time,

but

the

quarter

was

strong.

You

look

at

our

bond

portfolios

for

the

month.

You

can

see

we're

up

anywhere

from

3.09

to

6.47.

B

B

You

know

we're

hearing

a

lot

of

scrutiny

on

the

big

energy

companies

right

now

you

know

you're,

making

all

this

money

and

you're

not

going

to

you

know

drill

any

new

wells

or

or

anything

back

you're.

Just

going

to

reward

shareholders,

and

that's

probably

going

to

continue

to

happen,

the

one

thing

that

I

did

ask

Stan

about

is

share

BuyBacks,

which

is

a

popular

way

to

reward

shareholders.

When

things

are

good,

there's

a

one

percent

tax

on

share

BuyBacks

right

now

for

domestic

companies.

B

He

said

that

could

go

up,

but

if

that

were

to

happen,

they

would

probably

shift

the

balance

between

share

BuyBacks

and

dividends.

So

there

are

multiple

level

levers

there

and

I

did

remind

Stan.

Also

that

don't

fall

in

love

with

energy.

There

are

other

cheap

parts

of

the

marketplace

out

there

and

he's

absolutely

value.

Managers

can

be

that

way

once

they

find

once

they

hold

a

trade

for

a

while

think

about

it.

He's

held

these

for

five

years.

They've

only

performed

great

in

the

last

two.

He

sees

a

lot

of

Runway

ahead

of

them.

B

It's

very

tempting

for

the

Investor's

mindset

to

say

this

is

just

going

to

go

on

forever

and

then

you

can

see

Causeway

had

another

great

month

and

that

led

to

26

return

for

the

quarter

and

very

interestingly

enough.

We

have

two

portfolios

with

positive

returns

for

the

12

months

ended

131,

which

is

a

remarkable

turn.

Those

are

both

value,

they're,

both

Equity

managers,

and

that

is

kind

of

what

you

do

see

when

markets

turn

from

dramatic

downturns

to

Rises.

B

Just

a

minute

on

the

market

slides

here,

I'll

take

just

a

couple

of

minutes

here,

put

some

things

in

perspective:

this

is

long-term

Market,

history,

I

think

we've

been

through

this.

We

are

still

you

know.

We

have

drawdowns,

we

have

increases

and

over

time

the

market

does

go

higher

because

of

what

it

represents

next

slide.

This

is

the

bond

market

right.

It's

going

to

take

a

while

longer

for

the

bond

market

to

recover,

but

it

has

recovered

quickly

in

the

past.

B

B

The

bottom

of

the

bond

market

to

climb

10

and

a

half

34

and

a

half

and

12.55

percent,

so

the

returns

can

be

strong

going

forward

and

we've

kind

of

seen

some

of

that

next

slide,

I

think

I'm

going

to

end

with

this

one.

This

is

a

scatter

plot,

so

this

shows

you

in

return.

Space

What

returns

generally

look

like

for

the

U.S

Equity

investor

and

that's

assuming

that

you're

too

big

enough

two

biggest

asset

classes

or

S

P

500

and

the

aggregate

Bond

Index

right.

B

So

the

vertical

shows

you

the

return

of

the

S

P

500

for

each

of

these

years,

so

1985

or

1982.

That

return

was

about

21

right

the

where

and

then,

if

you

look

at

the

horizontal

axis

from

left

to

right,

that

shows

you

the

return

of

the

bond

market.

So

when

I'm

looking

at

these

years,

1982

the

equity

Market

was

up

20,

the

bond

market

was

up

32

percent

right.

That's

what

that

shows

you

in

this

case.

The

best

place

to

be

is

the

North

East

quadrant,

as

you

look

at

it.

So

that's

phenomenal.

B

Where

are

we

we're

22

2022

I

argued

that

that

dot

shouldn't

be

green,

but

that's

because

our

corporate

color

is

that

color

should

be

red.

No,

it

all

feels

that

way.

But

on

that

column

you

can

see

that

the

bond

market

was

down

18

and

the

stock

market

was

down

13.

again,

nothing

anywhere

near

that

even

in

2008,

which

was

the

financial

system

and

the

world

economy.

B

That's

a

good

question:

I

will

have

to

get

back

to

you.

I

can

get

back

to

you

before

I

leave

today,

but

it

is

if

we

I

want

to

I

want

to

answer

that.

Give

you

a

good

question.

It

is

not

our

International

Equity

exposure.

The

total

is

about

10

percent

I'm,

going

to

ask

you

to

go

to

one

slide

for

me

really

quickly

and

it's

in

the

it's

in

the

1231

report.

It's

near

the

beginning.

B

Think

it's

a

wonderful

question

there,

so

this

is

The

Benchmark

index

that

Causeway

uses.

If

you

look

on

the

right

hand

side,

this

is

international

Equity,

so

we

use

what

is

called

the

acqui

index,

that

is

the

all-country

world

x-us.

So

it's

all

countries

in

the

world,

except

for

the

United

States,

and

it's

weighted

on

a

GDP

basis,

so

that

gray

column

tells

you

the

waiting.

B

B

Those

two

might

go

negative

at

the

same

time

that

is

12

or

13

percent

of

the

28

percent.

That's

Emerging

Markets,

so

they're,

almost

40

percent

of

the

entire

Emerging

Markets

complex,

is

in

those

two

countries

which

I'm

cautious

on

them.

Right

now.

For

a

lot

of

reasons,

one

thing

also

to

notice:

there's

no

Russia

in

that

index

anymore.

If

you

remember

last

February

yeah.

A

B

They

were

completely,

they

were

part

of

the

index.

It

was

relatively

small

last

year,

but

the

Morgan

Stanley

Capital

International,

that's

the

index

provider

said

you're

out

of

the

index,

which

means

that

you're

virtually

uninvestable

and

if

you

had

any

Holdings,

which

we

did

tiny

bit

in

Russia,

it's

still

been.

It's

been

marked

down

to

zero

and

you

still

cannot

trade

it.

B

A

A

A

F

E

The

cafe

anymore,

no

I,

just

have

a

few

points

to

make

about

the

June

30

financial

report.

The

first

point

is:

if

you

look

on

page

one,

the

financial

report

was

giving

given

an

unmodified

opinion

from

the

Independent

Auditors,

which

is

what

we

want,

and

the

full

report

can

be

found

on

page

one

and

then

from

there.

If

you

can

turn

to

page

nine

and

the

statement

of

plan

net

position,

what

I

wanted

to

point

out

there

is

that

at

June,

30th

2022,

the

trust

reported

a

net

position

of

85.86

million.

E

The

next

thing

I

would

like

to

talk

about

or

point

out,

is

the

funded

ratio,

and

if

you

can

turn

to

page

35,

they're

going

to

be

several

pages,

but

the

the

trust

funded

ratio

looks

at

how

much

Actuarial

liability

the

trust

has

versus

how

much

the

net

position

or

money

it

has

to

pay

that

liability

at

June.

30Th

katpa

could

pay

52

percent

of

the

liability

with

the

funds

that

it

has

and

that's

an

increase

of

3.9

percent

over

the

prior

year

ratio

of

48.1.

E

A

A

Hey

we

have

a

motioned

and

a

second.

If

everyone

would

vote

the

actor

is

accepted.

Thank

you.

You

can

go

ahead

and

move

on

to

the

next

item,

which

is

the

acceptance

of

the

interim

financial

report

for

the

period

ended.

December,

31st,

2022.

I

hope

that

just

like

Doug

lifted

our

Spirits

with

the

monthly

report

I.

E

Know

this

one

here:

I

only

have

one

point:

I

wanted

to

talk

about,

and

it's

on

Page

Six

and

I'm,

just

turning

it

and

that's

the

statement

of

changes

in

plan

net

position

at

December,

31st

2022

the

report

that

the

report,

the

trust,

reported,

a

net

position

of

86.75

million.

This

is

an

increase,