►

From YouTube: San Bruno City Council Meeting October 23, 2012 10a. State Pension Reform Legislation Report

Description

San Bruno City Council Meeting

October 23, 2012

10a. State Pension Reform Legislation Report

A

B

Mayor

members

of

the

City

Council

and

councilmember

O'connell

on

skype,

I'm

pleased

to

present

you

with

a

short

presentation

on

the

pension

reform

bill

which

runs

about

39

single-spaced

pages.

We've

tried

to

condense

it

down

into

just

a

few

slides.

So,

as

you

can

see

from

the

first

slide,

this

was

recently

adopted.

It's

going

to

be

in

effect

or

start

being

in

effect

at

the

beginning

of

the

year,

and

it

covers

pretty

much

all

state

pension

plans,

not

not

all

of

them,

but

most

of

them

and

we'll

talk

about

the

ones

that

it

doesn't

cover.

B

B

So

the

takeaway

from

that

is

that

in

essence,

cities

across

the

state,

including

San

Bruno,

essentially

assume

the

risk

that

changing

demographics,

variations

and

investment

returns

and

so

on

won't

exactly

match

purses

actuarial

model

that

they've

used

to

set

the

rates

for

any

particular

year.

So

that's

why

the

city

sees

fluctuating

rates

over

time

and

why

employees

pay

a

fixed

percentage.

B

So,

let's

just

take

a

quick

look

at

how

pers

itself

has

done

over

the

years,

and

the

answer

is

not

not

too

bad.

Considering.

There

are

a

lot

of

other

pension

funds

that

are

in

worse

shape

than

pers

they're

about

75%

funded

for

both

miscellaneous

and

safety,

and

purses

position

is

that

the

unfunded

liability

is

really

an

accounting

issue,

not

a

solvency

issue.

B

The

reason

for

that

is,

they

don't

have

to

pay

the

entire

amount

out

in

one

year

or

even

five

or

ten

or

twenty

years,

it's

essentially

a

very,

very

long

term

system,

and

so

it's

okay

for

them

to

be

in

the

neighborhood

of

about

75%

funded.

They

don't

have

to

be

a

hundred

percent

funded.

The

other

piece

of

good

news

from

pers

is

that

their

average

rate

of

return

over

the

last

30

years

has

exceeded

what

they've

assumed

by

about

two

percent,

and

so

that's

pretty

good.

B

However,

as

you'll

see

in

the

next

slide

that

average,

that

actual

rate

of

return

really

fluctuates

significantly

and

that's

what

causes

their

investment

return

to.

Look

like

this,

so

we're

hoping

that

nobody

here

in

the

audience

or

at

home

has

an

IRA

or

an

investment

fund

whose

performance

looks

like

this.

That

would

be

a

very

volatile

fun

to

have,

but

purse

can

have

it

because

they

have

such

a

long

investment

horizon.

This

is

not

the

kind

of

performance

volatility

that

you

would

even

expect

or

want

for

your

own

pension

fund.

B

The

effective

of

this

volatility

is,

it

does

affect

the

employer

contribution

rates

on

a

yearly

basis

and

we'll

see

why

that

is

in

just

a

minute.

So

let's

talk

about

the

actual

law

and

what

it

what

it

doesn't

do.

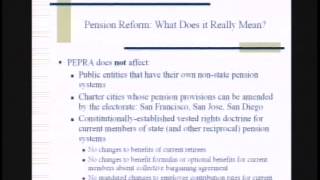

First

of

all,

it

doesn't

affect

public

entities

that

have

their

own

non

state

pension

system.

There

are

a

few

of

those.

B

There

are

charter

cities

where

the

electorate

can

set

pension

benefits

and

those

are

the

ones

you

tend

to

read

about

in

the

newspaper,

San

Francisco,

San,

Diego,

San,

Jose

I

think

they've

got

something

on

the

ballot

there,

and

the

new

law

does

not

affect

the

vested

rights

of

current

members

of

either

pers

or

other.

What's

called

reciprocal

pension

systems

and

all

the

reciprocal

system

is

is,

is

one

that

says.

If

you're

in

our

system,

then

you

can

transfer

over

into

pers

or

some

other

system

that

has

that

reciprocity.

B

So

the

bottom

line

is

no

changes

to

current

retiree

benefits,

no

changes

to

benefit

formulas

or

optional

benefits

for

current

members,

absent

some

sort

of

collective

bargaining

and

the

employee

contribution

rates.

The

eight

and

nine

percent

that

we

saw

on

the

slide

before

our

are

not

required

to

be

changed

until

2018,

and

even

that

with

a

few

caveats

and

we'll

look

at

that

in

just

a

second

all

right.

So

let's

take

a

look

and

see

how

the

law

affects

current

san

bruno

employees.

So

the

first

thing

is:

the

law

requires

that

is

an

employee.

B

You've

got

to

contribute

at

least

half

of

the

normal

cost

of

your

pension

by

2018,

but

what

the

law

does

is

set

a

cap

of

eight

percent

for

miscellaneous

twelve

percent

for

safety.

Well,

if

you

remember

from

the

previous

slide

miscellaneous

already

paying

eight

percent,

so

under

the

new

law,

they

wouldn't

have

to

pay

anymore,

even

though

eight

percent

isn't

necessarily

half

of

the

normal

cost

of

the

pension

now

or

may

not

be

in

the

future.

B

As

far

as

safety

is

concerned,

right

now

they're

at

nine

percent,

they

could

go

to

12,

but

that

has

to

be

collectively

bargained.

So,

there's

a

little

bit

of

ambiguity

in

the

law

about

whether

the

the

city

can

impose

that

in

2018

or

whether

there's

some

other

process

that

will

have

to

be

used

and

the

the

most

of

the

opinion

at

the

moment

is

that

it

will

have

to

be

bargained

for.

So

that's

how

it's

going

to

affect

current

employees.

B

It's

also

going

to

affect

current

employees

because

they

won't

be

able

to

purchase

service

credit

after

the

first

of

the

year.

So

if

you're,

a

city

employee

in

this

city

or

anywhere

else

in

the

state,

if

you

want

to

buy

that

extra

service

credit,

now

is

the

time

to

do

it.

There's

no

retroactive

pension

enhancements.

If

you

can

get

convicted

of

a

felony,

you

don't

get

part

of

your

pension

and

you

can't

come

back

to

work

as

an

employee

except

under

limited

circumstances.

So

that's

how

the

law

affects

current

san

bruno

employees.

B

Let's

take

a

look

for

a

second

and

see

how

the

law

is

going

to

affect

new

members.

That

is

new

members

in

pers

people

who

have

never

been

in

pers

before

or

in

any

other

reciprocal

system.

What's

going

to

happen

after

the

first

of

the

year,

and

the

answer

is

that

for

those

new

people

coming

into

the

system,

there's

a

new

retirement

formula

for

miscellaneous

employees,

as

you

see

two

percent

at

62

maximum

benefit

of

two

and

a

half

at

67.

So

right

now

the

city

has

a

more

favorable

formula

than

that.

B

The

new

safety

formula

is

going

to

be

2.7

at

57,

and

employees

aren't

going

to

be

able

to

use

their

their

highest.

Your

performance

in

terms

of

pay

they'll

have

to

average

over

three

years.

In

addition

to

that,

they

can't

use

overtime

or

other

kinds

of

payouts

to

enhance

their

pension

and

their

income.

That's

pensionable

is

going

to

be

captive

132,000.

So

that's

a

significant

difference

for

new

members

that

come

in

and

there's

really

just

a

couple

of

other

changes.

B

There's

no

supplemental

plans,

oftentimes

cities,

would

would

adopt

other

defined

benefit

plans

in

order

to

supplement

purrs

and

you're

not

going

to

be

able

to

do

that

anymore.

For

new

members

who

come

in

after

the

first

of

the

year

and

then

last

but

not

least,

our

contributions

to

a

deferred

comp

plan,

like

a

457

plan,

is

no

longer

going

to

be

invested

right.

It's

not

frankly

clear

that

it

was

a

vested

right

to

begin

with,

but

the

law

makes

it

clear

that

employers

can

are

free

to

to

change

that

if

they

wish

all

right.

B

So,

let's

take

a

look

and

see

how

the

new

law

is

going

to

affect

the

city's

pension

costs,

if

at

all.

Well.

First

of

all,

the

new

law

only

applies

to

these

new

members,

people

who

have

never

been

in

pers

or

any

other

reciprocal

system,

but

we're

told

by

the

human

resources

department

at

about

eighty

percent

of

the

city's

new

hires

in

the

past

five

years

were

actually

new

members,

and

so

what

that

tells

us

is

if

that

trend

continues.

B

Over

the

longer

term,

we

are

going

to

see

a

decrease

in

those

pension

costs,

because

most

of

the

new

hires

are

new

members

that

are

going

to

be

subject

to

the

new

and

less

expensive

rules.

However,

the

short

term

costs

are

likely

to

increase

that.

Why

is

that?

Well,

pers

says

that

it's

going

to

increase

for

the

employer

about

half

a

percent

25

percent.

That's

a

pretty

big

swing,

in

fact.

That's

an

order

of

magnitude.

B

Afterward

and

the

lows

are

smoothed

out

over

several

years,

so

they

don't

catch

up

with

each

other

and

that's

why

you

see

the

rates

going

up.

So

finally,

what's

next

we've

yet

to

see

whether

there's

going

to

be

in

effect

on

retention

or

recruitment?

We

don't

know

the

answer

to

that

yet

and

I

think

it's

safe

to

say

that

it's

not

over

yet

I.

Think

that

you'll

see

some

additional

legislation

for

some

more

reforms,

especially

to

have

the

employees

take

on

some

of

that

risk.