►

Description

San Bruno City Council Meeting February 11, 2014

10b. Accept CAFR for Year Ended June 30, 2013

A

A

B

Vice

mayor

and

members

of

the

council,

the

california

government

code

requires,

at

all

general

lost

cities,

complete

annual

independent

audits

of

their

financial

statements.

Part

of

a

city

council,

members,

governance

and

fiduciary

responsibility

includes

generally

understanding

the

financial

condition

of

the

city.

B

It

is

for

this

reason

that

auditors

communicate

with

the

city

council

at

the

beginning

of

the

audit

to

ascertain

any

issues

or

areas

of

concern

by

the

City

Council.

The

audit

for

the

city

of

San

brew,

the

the

audit

of

the

city

of

San,

Bruno's

financial

statements

for

the

year

ended

june.

30

2013

was

completed

right

at

the

end

of

last

year.

B

It

was

a

deadline

that

permitted

us

to

again

submit

our

kafir

document

for

the

annual

award

that

is

presented

by

the

g

fo

a

so

we

did

complete

it

on

time

at

the

end

of

the

year

to

do

that.

So

the

the

kafir

report

that

you

have

tonight

and

the

other

reports

were

completed

at

that

time.

The

city

council

has

a

resolution

on

the

agenda

tonight.

C

Good

evening

my

name

is

Ahmad

Gorobei.

I

am

the

partner

in

charge

of

the

audit

of

the

city.

You

have

the

comprehend

the

comprehensive

annual

financial

report.

This

is

an

annual

financial

report.

This

is

the

results

of

operations

for

this

city.

As

of

jun

30

2013

thats

prior

fiscal

year,

it

is

used

by

regulators.

It

is

used

by

Grant,

Grand

Tours.

It

is

used

by

creditors.

C

It

is

used

by

many

different

parties

and

I'm

going

to

walk

you

through

the

different

components

and

I

know

it's

about

140,

page

report,

but

a

few

pages

in

there

that

are

important

when

reading

these

financial

statements.

That

will

give

you

a

brief

overview

about

the

financial

health

of

the

city.

I

have

a

an

index

here

as

to

or

a

somehow

a

table

of

content

of

the

division

of

this

financial

statement

of

the

comprehensive

annual

financial

report.

It

includes

a

letter

of

transmittal

included

in

the

introductory

section,

a

financial

section,

a

statistical

section.

C

C

It

kind

of

briefly

describe

significant

transactions

that

the

city

had

entered

into

in

2000

and

13

the

basic

financial

statements,

some

notes

explaining

these

financial

statements.

Statistical

sections

are

interesting

component

of

the

financial

statements

of

the

kafir.

They

give

you

information

about

the

residents

about

income

per

capita

and

so

on

and

so

forth.

C

Just

to

pinpoint

you

I

know

it's

a

big

report,

but

just

so

that

you

would

know

the

financial

condition

of

the

city.

I

want

to

pin

point

you

to

a

page

18

in

the

financial

statements

which

includes

a

consolidation

of

the

city

funds,

all

the

city

funds,

alongside

with

some

what

we

call

converging

entries

to

include

long

term

assets

on

long

term

liabilities

and.

C

We

call

it

a

statement

of

net

position.

It

combines

all

the

governmental

funds,

such

as

your

general

fund

and

all

the

enterprise

funds,

such

as

your

utility

funds

and

the

best

way

to

know

the

financial

condition

of

the

city

is

to

take

a

look

at

the

net

position.

This

is

what

we

call

equity.

This

is

how

much

money

is

left

over

after

using

assets

against

the

liabilities

and

the

equity

shows

for

the

city.

C

Sorry,

the

pension

obligation

bonds

that

the

city

had

issued

and

thereby

increasing

your

non-current

liabilities

from

about

40

million

253

million

other

than

that

the

assets

current

assets,

capital

assets,

I

mean

capital

assets

increased

slightly

because

of

some

construction

projects

netted

against

depreciation.

Current

assets

remain

the

same

you

currently,

but

it

is

almost

remain

the

same.

Your

equity

almost

remains

the

same

I'm

going

to

go

through

that

component

of

the

net

position,

where

we

have

restricted

and

unrestricted.

This

is

the

spendable

amount

of

your

the

various

components

of

funds.

C

C

Now

it's

a

good

thing

that

the

city

did

issue

a

pension

obligation,

bonds

and

recognized

that

liability

in

2015

all

cities

all

governments

are

gana,

are

going

to

recognize

pension

liability,

possibly

after

the

opieop

liabilities,

are

going

to

be

recognized

on

the

financial

statements

right

now,

when

we

talk

about

pension,

when

we

talk

about

oh

pep,

it's

just

a

reporting

requirement.

It

does

not

go

in

those

two

columns.

They

are

reported

in

the

notes

to

the

financial

statements.

There

are

legal

liabilities

for

these

governments,

but

right

now

they

are

not

reported.

C

The

accounting

standards

are

changed

or

are

being

changed

whereby

these

liabilities

will

have

to

be

reported

on

these

statements.

Of

net

position

some

highlights

cash.

Increased

revenues

are

higher

this

year,

because

property

taxes

economy

is

getting

better

investment

in

capital

assets,

which

is

again

capital

assets.

That's

due

to

some

of

the

construction

that

the

city

had

done.

C

Again,

it's

also

noted

on

page

20

I

know

it

looks

really

big

but

here's

the

summary,

a

kind

of

consolidated

into

one

column

where

you

see

revenues,

minus

expenses

equals

change

in

net

position,

and

if

you

see

it,

net

position

did

decrease,

but

mainly

because

of

that

pension

obligation

bond

that

the

city

had

issued.

Otherwise

it

would

be

flat

between

the

two

different

tears.

If

you

look

at

revenues

last

year

there

were

82

million

this

year

there

are

70

million

theres.

C

Some

timing,

differences

and

I

think

that

the

main

reason

as

to

why

revenues

decline

is

you

no

longer

get

the

property

taxes

related

to

the

RDS

as

the

main

reason

as

to

why

these

decline

expenses

are

extremely

comparable

to

the

prior

year?

I

mean

this

is

just

inflation

adjustment.

That's

what's

happening

over

there.

The

special

item

is

the

recognition

of

that

pension

obligation

bond,

which

I

would

go

through

very

quickly.

At

the

end

of

this

presentation,.

C

Again,

revenues

improved

in

areas

in

general,

fund

tax,

increment

sales,

tax

transit,

occupancy

tax

and

card

room

tax.

General

revenues

decreased

as

a

result

of

the

loss

of

RDA

property

tax

revenues,

and

then

expenses

are

almost

comparable

to

prior

year

increased

because

of

inflation,

mainly

because

of

retirement

costs

increases.

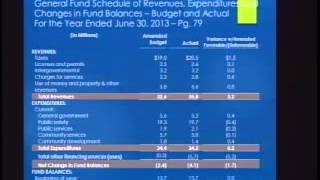

C

We

have

a

schedule

of

revenues.

Expenditures

specifically

for

the

general

fund.

General

fund

is

the

main

emphasis

for

the

operation

of

the

city.

It's

the

main

operating

fund

of

the

city,

most

of

the

expenses

operating

expenses,

are

posted

to

that

particular

fund

and

I.

Have

it

summarized

in

this

PowerPoint,

and

you

can

actually

see

that

on

page

79

of

the

audit

report.

C

And

it

shows

what

the

budget

is

original

and

amended,

and

the

variances

between

the

budget

and

the

actual

it's

a

good

budget,

not

significant.

There

are

not

so

many

significant

variances,

actually

they're,

all

small.

The

budgeted

fund

balance

with

that

city

projected

that

the

ending

fund

balance

would

be

about

10

million.

C

Ok,

so

we

as

auditors,

you

see

these

numbers

here

on

the

financial

statements,

the

way

that

we

audit

them.

We

get

a

trial

balance,

we

get

a

download

from

their

accounting

system

and

we

go

out.

We

confirm

these

balances,

we

confirm

your

cash

with

banks.

We

confirm

your

receivables

with

the

state

with

the

county,

with

the

feds

whoever's,

giving

you

the

future

funds.

We

make

sure

that

your

payables

are

fairly

stated.

C

C

Alright,

we

do

two

more

supplemental

audits,

because

you

receive

federal

grants.

You

have

to

adhere

to

federal

requirements,

they

have

stricter

requirements

than

what

the

state

has,

especially

when

you

spend

federal

money,

the

time

certification,

time,

accounting

a

purchasing

requirements,

strict

purchasing

requirement.

We

audit

the

federal

grants

on

a

sample

basis

and

I'm

pleased

to

let

you

know

that

we

had

an

unmodified

opinion

or

a

clean

opinion.

C

We

know

also

that

you

are

required

to

have

an

annual

audit

on

the

sales

tax

that

you

received

from

SamTrans

from

San

Mateo

County,

Transportation

Authority

we

go

in

and

we

take

a

look

at

these

expenses.

We

compare

them

with

the

ballot

language

and

we

make

sure

that

these

expenses

are

in

compliance

with

the

ballot

language.

C

We

are

required

to

let

you

know

if

we

had

any

difficulties

in

the

moments

of

the

audit.

We

can

finish

the

audit,

but

sometimes

if

we

encounter

any

difficulties,

we

are

required

to

communicate

that

to

you

and

I'm

pleased

to

let

you

know

that

we

encountered

no

difficulties

in

the

performance

of

the

art

as

part

of

the

audit.

Also,

we

take

a

look

at

the

internal

control,

we'd

like

to

see

segregation

of

functions

in

duties.

C

Now

governments,

unlike

commercial

entities,

the

government's

adhere

to

what

we

call

Government

Accounting

Standards

Board,

while

commercial

entities

adhere

to

financial

accounting,

stanza

sports

and

little

by

little,

those

two

are

lining

up

with

each

other.

With

governments

the

there

are

certain

liabilities

that

are

reported

in

the

notes

to

the

financial

statements,

as

opposed

to

putting

them

on

the

balance

sheet

and

the

mint

and

the

way

that

the

government

or

Gatsby

requires

these

governments

to

recognize

these

liabilities

is

to

amortize

them

over

10

to

30

years.

A

popular

one

is

open.

C

Another

one

is

the

pension,

the

both

liabilities

they're,

both

for

past

services,

that

the

employees

had

done

for

these

governments,

and

there

are

funds

that

pers

will

collect

from

the

city

once

the

person

retires

and

same

thing

with

open.

Your

Teamsters

are

going

to

collect

on

the

required

funds

in

order

to

pay

for

these

invoices.

C

Now,

with

before

I,

go

very

quickly

in

20

peb,

there

is

a

new

standard

for

pension

now

Oh

peb,

but

they're

almost

basically

the

same

their

their

payments

for

future

services,

gatsby

68

it

came

out

about

a

year

ago.

It

requires

all

governments,

nation

wyd,

to

recognize

that

pension

liability.

Now

a

lot

of

these

governments

are

saying:

well,

the

pension

liability

is

located

with

CalPERS

and

CalPERS

pulls

all

these

employees

all

together

into

one

big

plan.

How

am

I

going

to

calculate

that

liability?

Calpers

will

give

you

that

liability.

C

They

are

in

the

process

of

calculating

that

amount,

and

you

will

have

to

report

it

and

record

it

on

the

financial

statements

similar

to

the

open,

Oh

pip

is

not

operated

by

CalPERS

every

city.

Every

governmental

agency

has

its

own

plan,

so

it

has

the

ability

to

measure

what

that

liability

so

going

back

to

open

again,

you

amortize

it

over

20

to

30

years,

and

you

recognize

that

liability

on

those

two

columns

set

of

financial

statements

that

we

showed

you

at

the

beginning

of

that

presentation.

C

75

and

your

actual

liabilities,

46

million

what

you've

recognized

already

on

the

financial

statements,

is

12

million.

Nevertheless,

your

liability

is

46

million

when

it

comes

to

open,

and

then

you

also

have

another

liability,

just

like

any

other

government

for

pensions,

and

that

also

will

be

calculated

by

CalPERS

and

given

to

you,

and

that

also

will

have

to

be

reported

on

the

financial

statements.

A

A

C

I

believe

our

DA's

word-

and

you

know,

excuse

me

I,

remember

all

the

numbers,

but

I

think

they

were

collecting

about

three

million

dollars

every

year

in

property.

Taxes

3.6

is

what

the

RDA

was

collecting

in

property

taxes.

Now

that

will

funnel

back

to

the

other

governmental

agencies,

including

yourself,

so

I'm

not

sure

what

the

net

came

out

to

be.

After

all,

that

amount

was

funneled

out,

but

it's

not

I

I

doubt

it's

a

big

number.

It's

probably

going

to

be

like

twenty

percent

or

fifteen

percent

I'm,

not

sure

exactly

what

the

amount

is.

C

A

C

What

we

actually

did

is

we

went

to

the

Cree

three

credit

agencies.

We

asked

them

the

question.

You

know

these

pension

liabilities

were

out

there

a

long

time

ago.

It's

not

like

they

were

not

there.

They

were

not

calculated

or

reported

because

of

the

manner

that

these

government's

work.

They

pull

all

these

pension

liabilities

into

one

plan

in

Sacramento

with

CalPERS

and

it's

kind

of

hard

to

know

the

specific

liability

for

each

governmental

agency.

C

We

don't

anticipate

that

there

will

be

an

impact

on

your

credit

rating.

So

that's

a

good.

That's

the

good

news

that

we

know

about

you,

don't

know

what

will

happen

10

or

15

years

down

the

road,

but

in

the

short

term

it

wouldn't

make

sense

for

these

credit

agencies

to

say.

Oh

now,

we

didn't

know

about

that

liability

because

they

didn't

know

about

it

and

they

didn't

know

that

it

existed

back

in

the

days

from

from

an

old

time

other

than

that

it

will

impact.

We

were

reporting

it.

C

Even

if

the

kafir

did

report

these

liabilities,

it

did

report.

The

OPEC

did

report

the

pension

liabilities

in

the

notes

to

the

financial

statements,

and

now

what

Gatsby

wants

you

to

do

is

take

that

from

a

reporting

requirement

into

a

recording

requirement.

It's

not

a

funding

requirement,

it's

just

a

recording

requirement

and

what

the

recording

the

difference

between

reporting

and

recording

is

that

it

impacts

your

equity,

that

net

position

that

we've

had

on

the

slides

over

here,

the

very

bottom

at

the

very

bottom.

You

have

110

million

dollars.

That's

your

equity!

That's

your

assets!

C

Minus

your

liabilities!

Now

it's

significant

component

of

your

SSN.

We

the

way

that

Gatsby

wants

you

to

split

it.

They

know

that

you're

as

a

government,

you

can

sell

your

capital

assets.

So

when

you

present

equity

at

and

you

want

to

adhere

to

Gatsby,

they

tell

you

take

out

the

capital

assets

component

of

equity

and

split

it

into

a

separate

line

item.

So

the

last

two

line

items

are

your

spendable

equity.

That

is

what

you

have

in

money

on

a

consolidated

basis

throughout

the

city.

Add

you're

going

to

subtract

from

that

amount,

the

pension

liability.

C

Now

we

did

because

you

replace

your

pension

liability,

which

was

a

reporting

requirement,

because

the

city

replaced

it

with

a

a

pension

obligation

bond.

It

begins

an

actual

accounting

liability

and

therefore

you

did

recognize

a

significant

component

of

your

pension

liability

in

there,

but

nevertheless,

all

cities

or

governmental

agencies

will

have

to

recognize

a

pension

liability

that

would

reduce

those

last

two

numbers

that

you

see

in

there

on

the

financial

statements.

Now

they

were

reported

these

these

pension

liabilities

were

reported

and

you

can

see

them

on

page.

C

73

as

well

you'll

see

how

much

do

you

have

money

with

CalPERS

and

how

much

is

the

actual

pension

liability

and

how

much

is

the

unfunded,

but

you

do

have

two

plans

with

CalPERS.

You

have

one,

we

call

it

the

miscellaneous

plan.

There

is

another

plan

where

it's

kind

of

hard

to

calculate

it

because

they

pull

all

the

categories

of

employees

together

is

called

the

safety

plan,

the

safety

plan.

We

don't

know

what

that

number

is

CalPERS

will

calculate

it.

C

A

B

Two

additional

comments

not

related

to

the

financial

statements,

so

I

don't

know

if

there's

if,

if

there's

any

other

questions

would

would

be

glad

to

respond,

I

guess,

but

the

two

things

I

would

like

to

comment

on

is

I

think

the

council

is

well

aware

that

I

SAT

here

for

many

years,

taking

all

the

credit

for

work

that

I

actually

never

did,

but

I

would

feel

remiss

if

I

took

any

credit

this

time

around,

especially

the

in

the

middle

of

the

audit.

The

finance

director

left

the

city

and

Darlene

Wong.

B

Our

accounting

manager

picked

up

really

significant

responsibility

for

completing

the

audit

and

getting

it

and

we're

working

with

the

auditor.

Darlene

had

really

not

experienced

that

role

before

and

in

the

time

I've

been

here.

The

six

weeks

I

came

until

the

the

audit

was

completed

I,

I

watched

next

door.

What

Darlene

was

going

through

and

and

so

I

just

wanted

the

council

to

know

that

Darlene

just

made

a

very

significant

effort

in

the

completion

of

this

unqualified

audit.

B

So

I

would

like

to

mention

that

the

other

comment

I

would

have

is

that

the

finance

department

believes

that

the

auditors

significantly

and

rigorously

adhered

to

the

contract

requirements

and

to

let

you

know

that

this

particular

audit

is

the

third

and

final

year

of

the

contract

as

it

currently

exists.

It

was

a

three-year

contract.

B

There

are

probably

competing

interests

in

engaging

in

a

new

contract.

There

could

be

higher

costs,

there's

the

effort

of

going

through

the

bid

process

or

the

or

the

the

the

proposal

process

from

the

finance

perspective,

there's

also

when

there

are

quality

auditors,

that's

a

good

thing.

From

our

perspective,

when

someone

new

comes

in

there

is

the

first

year

is

a

significant

significant

increase

in

the

workload

to

explain

every

transaction

to

the

to

the

new

auditors.

Now

some

people

say

well,

that's

a

good

thing.

You

have

new

new

eyes,

looking

and

so

forth.

B

So

there

is

somewhat

competing

several

times

in

the

past

years

that

I'm

aware

of

a

three-year

contract

has

been

extended

to

five

years

and

it

would

be

the

recommendation

based

on

what

we

think

is

a

quality

service

by

a

quality

firm.

It

would

be

our

recommendation

that

this

would

be

a

time

to

consider

extending

the

contract

for

the

firm

for

two

additional

years.

If

the

council

would

entertain

that

possibility,

finance

would

be

prepared

at

your

next

meeting

to

bring

back

a

an

agreement

amendment

extending

the

work

through

the

year

2015

any.

A

Of

the

questions

council,

any

action,

I

counsel

to

the

chair,

I

thought

you

were

new

I

thought

you

were

a

Kelly

girl

or

something

yeah

anyway.

I

know

I

I

realize

how

complicated

and

then

the

previous,

the

previous

finance

director

learned

everything

she

did

from

you.

I'm

sure

and

and

I

know

that

whole

department

is

very

proficient

and

very

deserves

all

the

all

the

credit

and

all

the

accolades

that

I'm

sure

you're

going

to

receive

the

next.

The

next

award

and

the

recommendation

to

you

know

it's.

A

It

needs

to

come

from

that

department

needs

to

come

from

your

department,

my

in

my

opinion,

working

together

with

with

this

firm

and

if

that's

the

case-

and

you

know

I'd

be

in

favor

of

that.

With

that

do

we

need

a

formal

resolution

and

I'd

like

to

introduce

a

resolution

to

accept

this

audit

girl,

council,

member

I,

birra

hi,

councilmember,

Salazar,

art,

councilmember,

O'connell

I

thanks

bear

modena

high

and

also

mr.

A

Leary

had

asked

if

we

wish

to

have

it

considered

to

be

brought

back

at

the

25th

meeting

in

February

for

an

extension

of

the

agreement.

Is

that

the

council's

desire?

Please

have

that

put

on

the

twenty-fifth

agenda

and

Darlene.

Thank

you.

I'll

be

half

the

council

in

America

for

all

your

working,

your

effort

to

have

this

brought

forward.

You

taken

care

of,

and

thank

you

for.