►

Description

Introduction: @juanjuan

Working Group Presentation (0:02:06): @SebVentures

Presentation 1 (0:04:06): Centrifuge

Presentation 2 (0:28:01): 6s Capital

Agenda and Discussion:

https://forum.makerdao.com/t/agenda-discussion-collateral-onboarding-call-8-wednesday-september-16-17-00-utc/4062

Governance Forum:

https://forum.makerdao.com/

Disclaimer: The videos in this playlist are produced by MakerDAO community members. Content produced by the community may not be representative of the views held by the Maker Foundation.

A

A

Again

we

have

seen

him

a

couple

times

it's

good

to

to

reinforce

and

be

able

to

discuss

more

about

it

and

same

thing

for

the

second

half,

when

we

will

have

matthew

ravinovitz

from

6s

capital

presenting

his

project

so

well

more

on

it.

On

a

personal

note,

I

think

that

well,

I

won't

see-

and

I

think

everyone

else

joining

me

here-

we

want

to

see

real

world

assets

in

in

the

platform,

not

only

the

community

but

the

community

at

large.

A

So

almost

everyone

there's

like

a

pressure,

so

we

want

to

see

a

little

bit

of

progress.

I

think

we

have

a

lot

of

information

scattered.

We

have

a

lot

of

industry

experts,

a

lot

of

people

that

have

essay

so

we're

at

the

point

where

we

need

to

organize

and

structure

a

working

plan

and

move

things

forward.

A

B

Yeah

sure

so,

I'm

kind

of

leading

this

group

to

find

a

way

to

get

rid

of

assets

on

maker

as

soon

as

possible,

and

mainly

to

offer

a

third

view

because

we

have

centrifuge.

We

propose

one

kind

of

collateral,

many

collaterals

by

the

way

and

success.

That

prop

was

something

a

bit

different,

but

still

a

real

asset.

And

I

want

to

explore

a

third

way

to

try

to

find

how

we

can

merge

those

kind

of

assets

to

get

rid

of

saturn

maker

as

soon

as

possible

and

in

the

better

shape

for

all

maker.

A

So

yeah

to

add

a

little

bit

and

to

answer

on

the

questions

on

the

chat.

Frank

asked

if

this

meeting

is

happening

every

wednesday,

so

not

yet,

but

ideally

we

would

leave

with

some

action

points

that

could

be

one

of

them

and

again

there's

this

forum,

both

that

sebastian

posted.

So

ideally,

we

would

get

people

value

around

that

and

get

something

concrete

going

on.

B

C

A

B

C

So

this

call,

to

put

it

very

simply,

just

for

the

people

that

don't

know

about

centrifuge

centrifuge

is

a

set

of

a

technology

that

allows

asset

originators

to

bundle,

different

loans,

not

in

form

of

nfts,

creates

pools

of

assets,

so

sort

of

securitize

them

and

issue

tokens

against

them

that

they

represent

a

share

in

this

pool.

These

tokens

are

interest

bearing

and

sort

of

entitled

the

own,

the

holder

of

these

tokens

to

an

interest

in

the

in

the

in

the

pool,

and

also

in

sort

of

in

case

of

default.

C

Six

proposals

that

allow

these

to

to

start

this

process

of

onboarding.

These

assets

to

maker

I've

mentioned

before

we

have

like

freight

shipping

invoices,

real

estate,

inventory,

trade,

finance

and,

and

so,

if

we're

sort

of

looking

into

all

these

different

kinds

of

assets.

Because

of

course

we

believe

that,

like

as

a

big,

a

big

variety

of

different

real

world

assets

is

in

the

end,

but

a

system

like

maker

needs,

and

so

we've

been

working

with

with

different

ones.

C

C

We

went

live

in

may

with

sort

of

this

product,

mostly

focusing

on

direct

investors,

buying

buying

these

drop

tokens

and

investing

in

these

assets.

These

were

all

settled

in

crypto,

al,

so

settled

in

die,

and

so

the

borrowers

actually

got

die

and

the

the

investors

got

their

interest

paid

and

died,

and

so

on.

This

is

sort

of

based

on

what

we've

been

doing

with

sort

of

very

closely

with

the

maker

community.

C

For

over

a

year

now

we

did

our

first

sort

of

transactions

with

other

asset,

originators,

new

silver

and

and,

for

example,

at

the

time

was.

It

was

our

first

transaction

that

we

did

together

so

showing

how

this

could,

in

the

future,

lead

to

real

world

assets

being

onboarded

into

maker,

but

also

sort

of

all

of

d5,

because

of

course,

by

bringing

real

world

assets

into

d5.

C

We've

actually

been

sort

of

working

with

the

domain

teams,

but

also

by

on

our

own,

by

ourselves,

sort

of

looking

for

trying

to

find

issues,

questions

and

propose

solutions,

and

we've

done,

we've

published

a

few

formal,

mid

proposals

and

informal

blog

forum

posts

to

start

these

different

discussions,

and

we

now

sort

of

in

in

the

last

couple

of

weeks.

We've

come

to

a

point

where

sort

of

I

think

objectively,

we

can

say

that

centrifuge

is

ready.

C

The

asset

originators

are

ready

and

I

think

I

hope

to

a

point

as

well,

or

at

least

that

is

my

understanding

of

the

maker

community,

that

we

are

ready

to

actually

talk

about

onboarding

these

assets

concretely,

and

so

we've

done.

We've

put

forward

a

declaration

of

intent,

this

this

mip

13

that

talks

about

sort

of

how

we

want

to

start

this

onboarding

process,

and

this

should

sort

of

lead

up

to

to

a

collateral,

onboarding

application.

C

It's

sort

of

similar

to

the

current

mip

12,

but

is

modified

slightly

to

be

more

specific

on

real

world

on

the

questions

that

you

have

to

ask

and

answer

on.

The

real

world

assets

in

in

parallel

sort

of

mip

22

is

a

proposal

that

we

did.

That

came

out

of

solving

one

of

the

trickiest

questions

in

in

real

world

assets.

C

We

can

lick

either

liquidate

these

assets

off

chain,

refinance

these

assets

off

chain,

so

just

find

another

bank,

for

example,

that

will

want

to

extend

credit

against

these

assets

or

just

let

them

age

to

maturity,

which

is

actually

a

lot

of

times,

not

even

that

long.

For

example,

our

sort

of

console

phrase

invoices

have

an

average

maturity

date

of

of

less

than

45

days.

So

it's

actually

quite

fast

to

just

let

this

portfolio

sort

of

mature

and

and

liquidate

it

through

that,

and

so

this

this

is

sort

of

the

third

piece.

C

That's

in

progress,

so

in

the

request

for

common

phase,

so

we're

here

right

now,

maybe

a

little

bit

more.

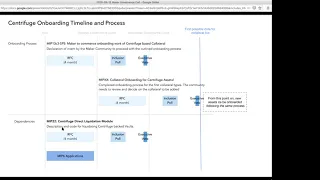

This

graphic

is

a

bit

outdated,

so

we

are

in

the

in

the

request

for

common

phase

for

these

two

mips

and

and

sort

of

working

on

on

the

map

that

will

onboard

some

of

this

first

collateral

going

into

detail

a

bit.

The

mip

13

declaration

of

intent

is

a

way

for

the

maker

community

to

declare

something.

C

What

does

that

mean?

It

means

that

a

statement

is

sort

of

written

iterated

on

together

with

the

community

and

then

brought

forward

to

a

vote

on

chain,

and

so

in

then,

in

the

governance

cycle.

Mkr

holders

are

able

to

vote,

and

so

the

way

we've

we're

using

this

as

sort

of

to

think

of

it

as

a

term

sheet

that

the

maker

community

can

say.

Okay,

we

roughly

agree

with

the

process

that

centrifuge

is

proposing

to

bring

these

assets

online

and

sort

of

to

follow

this

process.

C

Of

of

onboarding

these

assets-

and

so

you

can

read

the

map13

component,

three

subproposal

five,

which

is

our

specific

declaration

and

sort

of

in

in

four

bullet

points.

What

we're

proposing

is

we

we

want

we're

saying

we

want

to

start

small

meaning

around

5

million

died

debt

ceiling

for

collateral

type,

no

more

than

15..

The

reason.

C

The

second

component

is

that

we

will

be

working

supporting

this

as

much

as

we

can

as

centrifuge

centrifuge

has

a

team

of

software

engineers

that

have

extensive

experience.

Writing

smart

contracts.

We

also

are

very

familiar

with

maker

and

maker's

code

base,

and

so

I

think

we're

in

a

good

position

to

actually

do

a

lot

of

integration

work

ourselves.

That

doesn't

mean

we

don't

need

any

help

from

the

domain

team

and

sort

of

the

the

team

that

is

designing

large

parts

of

the

of

the

smart

contracts.

C

The

the

component

we're

working

on

now

is

mip.

I

call

it

xx

just

because

we

don't

know

the

specific

number

yet,

but

this

is

intended

to

and

I'm

not

looking

at

the

chat,

but

I

can

try

to

jump

in

if

there's

something

or

maybe,

if

you

want

to

interrupt

me-

feel

free

to

interrupt

me

for

questions

as

well,

but

yeah

so

so

this

this

mip

is

really

is

what

mip,

12

and

component

do

component

2

does

for

assets

like

rap

bitcoin

and

k

and

c

and

zero

x

token.

So

it's

it's!

C

The

the

final

executive

vote

that

the

dow

will

decide

on

to

onboard

a

specific

collateral

type.

So

it's

it's

the

spell

the

technically

the

spell

that

will

onboard

this

collateral.

If,

if

enough,

mkr

voters

hold

on

a

vote

on

it,

the

the

work

that

sort

of

has

to

be

done,

of

course

in

the

in

the

in

the

governance

in

governance

to

go

through.

This

is

sort

of

doing

the

risk

model,

doing

the

audit

of

the

smart

contracts

doing

so.

Setting

up

this

spell

and

publishing

it,

and

so

in

a

way.

This

follows

very

similar.

C

It's

very

similar

to

I've

posted

an

example

here,

and

I

can

share

those

slides

later

to

what

like

a

collateral.

Onboarding

would

look

like

for

a

crypto

asset,

and

so,

but

it

will

be

slightly

different

in

differences

that

I'll

go

go

into

in

in

a

bit.

So

this

is

really

the

final

milestone

and

our

goal

is

to

get

to

that

final

milestone

with

one

or

two

first

assets

as

soon

as

possible.

C

We

all

know

that

we

need

to

scale

the

dye

supply

significantly

and-

and

I

think

the

community

is

convinced

that

real

world

assets

is

a

way,

is

one

one

way

to

do

it

a

good

way

to

do

it,

and

so

this

is

what

we're.

What

centrifuges

is

sort

of

focusing

on

right

now

and

pushing

this

this

process

forward?

C

So

I

want

to

highlight

a

few

of

the

key

differences

between

the

regular

mips

to

make

12

process

and

what

we're

what

we're

proposing.

We

talk

a

lot

about.

I

thought

we

had

a

lot

of

chats

and

forum

posts

and

and

calls

about

the

differences

just

how

real-world

assets

work

and

how

how

crypto

assets

work.

C

I

would

if

you're

interested

go,

look

at

them

happy

to

answer

specific

questions

as

well,

but

I'm

mostly

this

might

be

a

bit

too

too

much

in

detail

for

for

some

of

the

audience,

and

so

I

would

recommend

you

like

sort

of

dig

through

the

forum

posts

a

bit

to

get

to

catch

up.

But

let

me

jump

right

in

here.

C

C

C

We

won't

be

trying

to

feed

in,

like

exchanges

or

or

sort

of

real-time

market

data

to

find

out

what

the

price

of

these

assets

are,

but

that

is

rarely

needed.

So

our

tin

lake

pools

have

a

way

to

calculate

a

nav

model

that

the

nav

on

chain

nav,

is

just

net

asset

value

sort

of

which

means

it

tries

to

determine

the

current

value

of

all

of

the

assets

in

this

pool.

C

It

takes

into

account,

for

example,

factors

in

probability

of

default

and

sort

of

expected

revenue,

so

interest

revenue

that

is

owed

by

by

borrowers

and

can

price

the

entire

pool.

So

as

a

so

for

maker's

perspective,

it

can

look

at

that

nav

model

and

if

it

determines

it

to

be

accurate,

then

that

can

be

used

as

the

as

a

price

source.

C

The

goal

can

be

that

we

can

have

these

this

data,

that

the

astro

originator

reports

be

verified

by

third

parties

and

have

oracles

that

provide

this

data

on

chain,

and

so

this

could

be,

for

example,

data

like

the

credit

score

of

the

borrower.

If

it's

a,

if

it's

a

consumer,

it

could

be

a

real

estate

estimate

or

it

could

be

like

some,

some

other

kind

of

asset

liquidation.

C

I've

mentioned

this

is

a

mip

22,

and

I

see

I'm

I'm

running

a

bit

over

time.

So

I

want

to

end

it

quickly,

but

liquidation,

just

there's

a

specific

way.

We

liquidate

these

because

there's

no

liquid

market,

the

actually

the

best

way,

is

to

have

the

asset

originator,

refinance

these

loans

or

let

the

portfolio

mature,

and

so

the

liquidations

work

slightly

differently

in

this

survey,

published

in

in

map22

again,

please

ask

your

questions

and

sort

of

engage

here,

the

risk,

the

risk

work.

C

We

are

sort

of

still

needs

to

happen,

and

that's

where

we

have

been

working

with

the

asset

originators

to

provide

like

data

package

on

as

much

information

that

we

can

give

to

to

sort

of

determine

what

this

should

be

and

there's

different

inputs

that

we're

sort

of

providing.

We

have

the

asset

originators

underwriting

process

so

how

they

make

decisions

themselves.

C

We

will

ask

them

to

publish

information

about

their

past

performance,

but

also

competitive

offers,

so

a

lot

of

them

have

offers

from

banks

reputable

banks,

sort

of

showing

okay

like

this

is

a

realistic

cost

of

capital

for

them.

But

then

also

we

can

look

at

sort

of

what

the

industry

performance

is

and

we're

hoping

that

we

can

sort

of

work

with

the

real-world

asset

working

group

here

in

finding

finding

a

way

that

we

can

define

these

and

sort

of

get

get

a

risk

assessment

by

the

by

the

community.

C

D

C

Taking

these

these

differences,

all

together,

will

ultimately

result

in

this

mip

that

will

outline

exactly

how

this

asset

should

be

onboarded.

What

risk

parameters

will

be

will

be

proposed

and,

as

as

sebastian

mentioned,

I

am

proposing

that

we

will

meet

every

other

wednesday

at

the

same

time,

we're

meeting

now

so

alternating

with

the

collateral

community,

call

that

we've

been

doing

and

sort

of

discussing

these.

These

points.

C

A

C

C

B

C

But

in

summary,

the

idea

is

that

maker

itself

is

not

an

illegal

entity,

and

so,

if

you're

buying

these

tokens

that

represent

a

share

of

security,

then

of

course

you

will

have

to

go

through

kyc

and

you're

acquiring

a

regulated

security

token

maker,

when

an

ass

originator

deposits,

these

assets

as

collateral

in

in

the

dao.

It

is

not

actually

issuing

the

security

because

you're

merely

using

it

as

an

escrow,

and

it

never

leaves

this

decentralized

entity.

C

And

so

because

of

that,

we

don't

have

this

issue

that

we

would

need

to

kyc

every

like

maker

dao

as

an

entity

or

like

think

of

okay,

we're

seeing

every

die

holder,

which

would

be

even

worse.

So

roughly.

The

idea

is

that

this

is

so.

The

security

transfer

only

happens

if

it

would

go

to

an

to

an

individual

person

which

would

maker

is

not

the

case

but

and

I'll

share.

There's

some

discussion

in

the

forum

about

that

as

well.

B

C

C

I

would

this

would

be

a

question

to

for

for

us

sort

of

to

the

maker

community.

What

is

like

the

best

format

for

us

to

do

this

and

like

we

can

set

up

a

google

drive

with

some

like

anonymized

information,

that

you

could

look

at

publicly.

Definitely

the

asset

originators.

Some

of

them

have

already

been

on

calls

and

sort

of

answered

questions

directly.

This

is

something

we

can

do

as

well.

Just

sharing

pdfs

like

we're

planning

to

do

everything,

but

yeah

definitely

we'll

do

that.

C

B

A

I

was

going

to

comment

on

that

actually,

because

maybe

it

would

be

good

and

no

not

a

comment

for

you,

but

more

for

the

working

group

to

have

like

very

clear

steps

on

on

what

do

we

have

what's

next?

What

do

we

need

from

all

the

like

risk?

Point

of

view,

the

technical

point

of

view,

anything

any

meat

that

should

be

approved

for

it

to

happen,

and

maybe

do

like

an

faq

section

where

we

can

post

these

questions

with

answers

and

supporting

documents

like

started

wiki.

Somehow

I

think

it'll

be

very

useful.

C

A

A

D

All

right,

so

I

am

at

rabinowitz

for

success

capital

referencing

the

credit

facility

for

today

now

that

we're

getting

a

little

bit

further

in

the

weeds.

My

attorney

made

me

put

up

a

disclaimer,

so

you

guys

can

spend

your

time

reading

at

some

other

time.

But

summary

is

this

is

not

a

securities

offering

anything

that

would

be

a

securities

offering

will

be

in

an

offering

memorandum

that

goes

to

a

would-be

investor

of

which

that's

not

the

objective

of

this

call.

D

So

fundamentally,

please

everybody

ask

questions.

Public

private

multiple

conference

calls

whether

or

not

we're

doing

this

on

the

forum

posts

feel

free

to

reach

out

to

me

personally,

etc.

It's

important

to

get

everybody

engaged

in

this,

not

only

for

my

proposal

for

centrifuges

for

the

next

five

that

come

after

that.

The

only

way

this

is

going

to

work

is

if

we

really

optimize

the

solutions

and

make

it

work

better

for

everybody.

So

what

are

we

trying

to

accomplish?

D

D

Nothing

we're

using

or

discussing,

is

new

in

terms

of

legal

structuring.

Most

importantly,

lenco

never

actually

touches

die

I'll

get

to

that

asterisk.

In

a

moment.

What

is

fundamentally

different

is

while

using

common

structures

and

common

agreements,

we're

taking

input

variables

from

mkr

governance,

that's

the

difference.

D

D

In

that

context,

everything

that

happens

from

a

smart

contract

perspective

of

maker

is

largely.

I

would

use

the

word

almost

agnostic-

it's

not

it's

very

relevant,

but

not

relevant

for

lenco.

It

just

happens,

which

is

somewhat

what

makes

it

elegant

lenco

then

does

its

fundamental

operations

pursuant

to

agreements

that

it

has

with

the

trust

and

why

it

could

borrow

money

in

the

first

place,

to

deploy

capital

into

would-be

borrow

codes

that

are

in

specifically

scope,

approved,

mkr

governance,

approved

structures,

specifically

credit

quality

credit

tenant

leases.

D

So

again,

let's

switch

our

perspective

if

this

structure

has

been

used

before

this

is

not

new.

In

this

scenario,

a

trust

is

being

created.

The

trust

is

the

lender.

The

trust

is

the

representative

body

of

all

mkr

holders.

Lendco

is

now

the

borrower

taking

that

money

from

the

trust

and

then

using

that

money

to

then

turn

around

and

lend

to

would

be

borrow

codes

and

there's

a

credit

agreement

between

the

two

with

an

asset

collateral

pledge

between

them

to

secure

the

loans.

This

is

nothing

new,

so

today

in

the

world

of

credit

tenant

leases.

D

D

D

Scale

from

the

eyes

of

maker,

if

we

were

to

do

every

one

of

these

projects

from

maker

we'd

be

having

to

have

a

vault

onto

our

own

into

our

own

scenario,

which

equals,

in

my

mind,

mkr

cognitive

overload

of

how

we

would

handle

multiple

quantities

of

vaults.

So

how

does

this

evolve?

It

evolves

by

having

a

centralized

structure

that

already

has

raised

equity

that

gets

married

with

a

with

a

maker

facility

into

one

centralized

structure

that

gets

audits

that

gets

inspection

that

has

inspection

rights.

D

That

then

turns

around

and

lends

money

out

to

the

would-be

projects.

All

of

those

projects

will

have

scope

approved

tenant

approved,

so

the

credit

quality

will

be

known

from

it

from

the

isa

developed

from

a

developer.

They

just

see

a

100

percent

loan

to

cost

from

a

would-be

lender

from

the

eyes

of

a

debt

facility

from

a

senior

debt

facility

right

now,

making

it

generic

whether

or

not

the

capital

is

100

or

whether

or

not

some

of

it's

done

with

equity.

D

D

If

there's

ever

a

default,

the

senior

lender

facility

is

the

one,

is

senior

to

everything

and

wipes

everybody

else

out.

So

how

do

we

do

this

on

scale

from

a

success

capital

perspective?

We

do

with

an

execution

team

and

we

break

everything

down

into

phases:

different

tenants,

different

structures.

Just

like

we're

building

an

aircraft.

D

We

start

off

by

figuring

out

how

much

we're

going

to

need

in

terms

of

time

we

make

the

developer

the

borrower.

In

this

case

they

do

all

of

the

front-ended

research

they

do

all

of

the

development

work

work

that

we

never

even

see

or

touch.

We

only

show

up

with

capital

when

we

have

a

shovel

ready

project

when

the

project

can,

when

the

lender

can

have

a

senior

lien

on

the

project

and

a

general

contractor

is

committed

to

do

the

projects.

D

Projects

can

last

anywhere

from

between

six

months

to

18

months

and

between

18

to

24

is

the

divestiture

period,

and

at

that

point

all

capital

is

returned

and

recycled

so

fundamentally,

phase

one

reach

excuse

me

real

estate

research.

This

is

where

developers

go

out

and

find

selection,

they're

negotiating

with

people

they're,

building

up

a

package

to

share

with

a

tenant

to

get

their

blessing.

D

Who

takes

the

risk?

The

developer,

senior

lender

and

the

investor

don't

touch

anything

here

same

thing

on

the

development

stuff.

They

engage

with

tenants.

They

work

on

getting

together

a

package

and

executing

the

bill

to

suit

and

the

ground

lease.

The

developer

takes

all

of

this

risk.

The

senior

lender

touches

nothing

here.

D

We

talk

about

when

there's

a

shovel

ready

project

is

at

the

point

where

everything

has

culminated

to

the

point

where

there

is

an

actual

closing

where

the,

where

there

is

a

guarantee

in

favor

of

the

lender,

where

there's

a

general

contractor

committed

the

land

is

simultaneously

acquired

into

a

newly

formed

llc

in

exchange

for

the

capital.

To

do

all

of

that,

success

receives

a

senior

lien

over

the

entire

project.

D

This

takes,

as

I

mentioned

before,

anywhere

between

five

to

18

months,

depending

on

the

scope

of

the

project

and

the

depth.

Some

of

them

have

much

more

horizontal

construction

than

our

other

that

are

otherwise

needed

and

at

the

very

end

we

die.

The

excuse

me.

The

developer

is

incentivized

to

divest

and

dispose

of

the

project.

The

developer

makes

zero

dollars

until

the

project

is

sold.

When

the

project

is

sold,

the

senior

lender,

success,

development

is

repaid

and

whatever

is

left

over,

goes

to

the

developer.

D

So,

let's

evaluate

like

the

three

fundamental

big

picture

risks-

and

these

are

clearly

not

totally

comprehensive

again.

My

attorney

made

me

say

it

fundamentally:

we've

got

smart

contract

risk.

Legal

risk

tenant

risk,

so

let's

go

through

those

now.

These

are

all

the

legal

contracts,

so

smart

contract

risk.

So

if

we

were

to

just

break

this

down

like

what

happens,

if

lenko

break

loses

his

private

keys

or

they're

compromised,

lenco,

never

touches

the

die,

so

largely

all

lenco

does

is

cause

the

dye

to

be

moved,

but

never

actually

takes

possession

of

it.

D

D

We

just

wait

till

there's

a

fix.

That's

been

implemented

same

thing

on

the

lend

co

side.

If

there's

a

risk,

we've

mitigated

the

risk

related

to

having

a

trust,

that's

providing

a

loan

by

implementing

a

trustee

with

legal

enforceability,

the

same

component

for

all

of

these,

where

every

enforceability

of

the

loan,

a

trust,

has

a

court

of

law,

a

standing

in

law

trus.

The

trust

can

cause

the

foreclosure

of

any

pledge

collateral

to

recover

proceeds,

and

one

of

my

favorites

lenko

manager

me

gets

hit

by

a

bus

right.

D

D

If

we

do

a

bad

deal,

lenco

has

to

recapitalize

itself

before

the

determination

period

or

this

whole

project

gets

unwound

and

lenco

gets

liquidated

when

the

money

that

gets

hit

first

would

be

the

equity,

because

30

percent

of

the

capital

has

to

be

in

the

form

of

equity

for

a

new

construction,

as

per

my

proposal

or

15,

if

it's

already

stabilized,

meaning

that

we'd

have

to

have

all.

If

there's

a

liquidation,

the

senior

money

gets

paid

back

first

and

if

there's

a

haircut

that

goes

down

to

the

equity.

D

So

at

the

borrow

co,

what

happens

if

there's

a

risk

of

bad

title

now?

All

of

our

closings

are

done

through

title

companies

that

issue

title

insurance.

We

make

sure

that

we

have

clear

title

and

that

the

senior

lender

receives

first

position.

Lien

on

everything.

Borroco

is

exposed

to

operational

risks.

If

there's

a

weather,

what

happens

weather

delays?

Well,

they

they

have

to

wait,

but

they

ultimately

pay

more

interest.

If

there

are

overruns,

the

principles

of

borrowco

end

up

having

to

inject

more

cash.

They

make

nothing

until

the

project

is

divested.

D

Now

the

real

question

comes

down

to

the

market

and

tenant

risk

of

what

happens

with

pricing,

because

the

piece

that

we

can't

de-risk

is

our

tenants

and

how

they

run

their

operations,

but

we

can

decide

which

tenants

we

can

select

and

why

fundamentally

we're

in

the

business

of

making

money

and

we

need

to

borrow

money

to

make

money

so

we're

only

going.

We

are

highly

motivated

to

only

pick

credit

worthy

tenants

and

we

only

get

investors

capital

because

they

believe

in

the

structure

we're

putting

forth.

D

Why

we're

not

putting

right

now

in

the

middle

of

covid,

putting

together

movie

theaters,

which

would

be

obviously

catastrophic,

so

we

can

cause

borrowers

to

have

insurance.

We

can't

obviously

control

the

weather

or

the

storms,

but

if

there

is

a

an

environmental

issue

that

causes

a

massive

destruction,

insurance

will

reinvent

reimburse

them

and

they

can

continue

with

their

project.

D

Worst

case

scenario,

market

conditions,

deteriorate

and

borrow.

Co

cannot

sell

the

completed

project

at

which

point

lenco

forecloses,

on

the

project

that

is

producing

a

yield,

which

is

c,

which

is

better

than

the

cost

of

capital

that

we're

getting

from

maker.

In

the

first

place,

we

collect

rent

payments

and

continue

to

do

so

until

we

sell

the

project

which

we're

not

in

the

business

of

holding

projects,

we're

in

the

in

business

of

lending

for

them,

we

wouldn't

fire

sale

it,

but

we

would

divest

it

appropriately

and

the

borrow

co

would

forfeit

all

of

its

profit.

D

The

real

issue,

I

think,

we're

going

to

find

in

six

months,

is

just

raw

concentration

between

a

large

amount

of

dye

going

into

very

few

entities.

Until

there

are,

you

know,

a

portfolio,

a

cohort

of

five

or

ten

other

equivalent

lencos

out

there

that

have

substantial

amounts

of

dye

to

get

people

comfortable

very

similar

to

the

stable

coin

issue

we

have

today

with

usdc.

D

So

let's

compare

and

contrast

so

assets

pros

and

cons.

You

know:

we've

got

eth

it's

decentralized,

but

it

relies

on

lots

of

centralized

on-ramps

wbtc

large

market

cap,

but

it's

somewhat

quasi-centralized

custodian.

We

go

down

this

list

and

real-world

assets

not

specific

to

credit

tenant

leases,

but

just

in

general,

using

a

trust

and

a

lendco

structure

which

is

known

and

battle

tested.

D

As

long

as

we

price

it

correctly

and

competitively,

we

will

have

almost

unlimited

demand

for

credit

and

then

the

issue

turns

into

credit

concentration

and

do

only

a

few

lend

codes.

Well,

initially,

one

or

ten

we

wanted

to

get

it

to

ten.

It

has

many

benefits,

and

the

only

con

is

that

it's

semi-liquid.

D

This

piece

I've

already

discussed

or

I've,

shown

this

before

I'm

happy

to

go

through

it.

I

don't

think

we

can

go

through

parts

of

it

now.

Fundamentally,

the

big

key

takeaway

here

is

that

success

capital

partners,

quote-unquote

lenco,

ends

up

with

a

portfolio

a

diversified

portfolio

of

lend

of

lenders,

senior

lend

senior

liens

in

a

variety

of

different

projects

that

are

geographically

distributed

with

different

tenants

and

that

tenant

list

is

expanding

based

upon

the

quantities

of

developers

that

want

to

use

our

services.

D

D

So

our

fundamental

generic

sequence,

you

know

we've

submitted

our

declaration

of

intent.

We

are

in

the

process

now

of

the

community

community

discussion

we'll

get

through

a

formal

cycle

here.

The

real

important

piece

here

is

because

we're

talking

about

actual

legal

structures

being

implemented

and

these

structures

are

not

cheap,

in

fact,

they're

very

expensive.

D

We

are

going

to

go

through

an

executive

vote

in

effect

to

approve

the

term

sheet,

as

lucas

had

outlined,

of

our

mip

13.

and,

if

accepted,

which

would

be

great

we're

going

to

conditionally

set

the

debt

ceiling

to

zero.

So

we're

going

to

vote

on

an

actual

number,

but

the

implemented

debt

ceiling

would

be

zero.

So

up

until

the

very

last

step,

the

community

is

going

to

take

basically

zero

risk.

D

It's

only

after

the

success

team

working

alongside

the

maker

representative

put

together

and

show

the

community

all

the

documents,

all

the

structures

that

have

been

implemented.

Then

the

community

would

have

another

executive

vote

to

further,

basically

ratify

it.

If

you

will

and

then

re-implement

the

previously

approved

debt

ceiling

going

from

zero

to

whatever

is

approved,

and

at

that

point,

success

would

be

able

to

borrow

against

it

pursuant

to

the

credit

facility

agreement,

which

has

a

whole

lot

of

covenants.

That

say

that

we

can't

borrow

money.

D

D

D

D

Understood

yeah

the

challenge:

here's

the

biggest

issue

on

that

is,

we

haven't

selected

the

trust,

the

trustee,

yet

the

trust,

company

and

they're

going

to

require

us

to

use

their

form.

There

is

no

scenario

where

we

present

an

agreement

and

say:

is

this

okay

use

us

they

have

their

own

form.

We

don't

get

a

choice

on

that,

but

the

law

that

we're

going

to

follow

is

the

delaware

statute,

delaware,

statutory

trust

and

that

actually

put

in

one

of

the

forum

links

it's

defined

there.

D

C

D

D

So,

in

effect,

from

a

tenant

to

a

developer

perspective.

Forget

us

for

a

second

from

a

tenant

to

a

developer

perspective.

The

tenant

is

looking

at

the

at

the

developer

as

being

almost

their

outsourced.

Investment

bank

they're

almost

creating

a

bond

with

these

net

lease

properties

and

that's

how

they

trade

in

the

market

once

they're

stabilized

and

the

temp.

The

these

net

lease

properties

are

a

very

liquid

market.

D

D

A

D

Yeah,

so

this

is

one

where

I

very

much

want

the

community's

insight

on

this,

because

that

the

rub

is

going

to

turn

into

that

success.

Capital

as

a

lender

comes

in

contact

with

confidential

information

and

some

of

that

information

it

just

cannot

share

under

privacy

laws

period.

End

of

discussion,

with

external,

with

the

public

quote

unquote

and

maker,

is

a

public

protocol,

so

we

have

to

come

up

with

some

other

mechanism

that

gets

the

community

comfortable

and

also

meets

the

legal

obligations

that

success

capital

has

with

would-be

borrowers

and

tenants.

D

D

You

know

yeah

it's

great,

but

I

still

want

somebody

else.

I

want

literally

five

people

from

this

call.

10

people

from

this

call

all

of

you

to

be

a

maker

representative

review,

the

transaction

in

depth

and

report

back

to

everybody

else

that

you

reviewed

it

also

that

this

is

a

legit

transaction

here,

all

the

check

boxes,

here's

the

package,

we've

reviewed

it

and

matt's

not

getting

a

car

out

of

this

we're

just

financing

a

insert

the

name

of

the

tenant

location

in

virginia,

for

example,.

D

I

don't

I

that

that

part

is

part

of

I

would

call

it

version

two

or

in

the

future.

There

are

areas

where

we

could

do

that.

The

question

turns

into

what

is

the

approved

scope

and

how

do

we

scale

it

and

to

me

the

model

is

really

much

more

of

not

necessarily

trust

but

verify

but

verify,

and

if

you

don't

do

it

right,

we

liquidate

and

liquidation

on.

This

scenario

is

so

epically

nuclear

because

it

not

only

impacts

lenco,

which

obviously

impacts

me.

It

impacts

all

the

borrowers

and

it

impacts

everything.

D

It's

something,

that's

possible,

but

I

don't

see.

I

actually

see

that

that

almost

introduces

liability

to

a

maker

representative

and

that's

not

really

the

objective.

The

objective

is

just

to

be

a

proxy

to

be

able

to

convey

the

equivalent

of

specific

information

in

a

translucent

environment

where

it's

more

the

substance

where

all

these

boxes

checked.

D

Yes,

did

he

do

the

annual

audit?

Did

the

audit

come

back

clean,

okay

that

part

much

we

can

do?

Did

you

see

that

the

money

transferred

from

a

to

b

to

c-

and

this

is

the

fund?

This

is

the

specific

project

that

it

went

into.

Yes,

okay,

that's

fine,

but

we

don't

have

to

release.

For

example,

the

borrowers

who

are

borrowing

from

success

capital

may

very

well

have

to

share

their

personal

financial

statements

with

success

capital.

None

of

that

information

is

going

to

be,

public

can

be

public,

it

has

to

be

private.

D

C

A

C

General,

like

my

question,

matt

was

I

I

fully

agree

with

you

like

sort

of

having

an

opt-in

on

every

asset,

and

every

transaction

would

be

it's

better

to

say,

like

there

should

be

a

mechanism

to

halt

something.

It

holds

the

this

whole

mechanism

if

it

goes

out

of

bounds-

and

this

is

also,

of

course,

what

we're

proposing

with

our

asset

originators,

because

I

I

I

see

that

make

sense

and

sort

of

to

some

extent.

D

The

answer

is,

it

depends

right.

So

we

are.

We

are

going

to

be

set

up

with

multiple

tranches,

but

we

have

a

fundamental

requirement

that

we

have

to

deploy

the

equity

first

into

any

given

project

that

ultimately

gets

capital

deployed.

So

if

we

go

after,

let's

just

pick

and

we're

not

doing

mcdonald's

but,

let's

just

say

we're

doing

a

mcdonald's

right

and

the

mcdonald's

needed

and

I'm

picking

easy

numbers

for

math,

because

I'm

tired,

so

let's

just

say

it

was

a

million

dollars.

D

We

have

to

deploy

the

300

grand

first

out

of

equity

first

and

then

the

remainder

comes

out

of

the

the

maker

facility.

Now

how

we

raise

that

equity

is

actually

not

almost.

I

know

where

you're

going

with

it,

but

it's

almost

it

doesn't

even

matter

at

that

point,

because

what

mattered

was

the

fact

there

was

a

buffer

and

the

buffer

is

that

there's

a

million

dollars

worth

of

value

and

maker

has

the

first

position

on

only

700

on

the

full

million

of

value,

but

they

get

700

grand

they

got

sold.