►

From YouTube: Audit Committee - May 29, 2019 (1 of 2)

Description

Audit Committee meeting - May 29, 2019 - Audio Stream

Agenda and background materials can be found at http://www.ottawa.ca/agendas.

A

A

C

A

Thank

you

very

much.

Three

agenda

items

today.

Item

number

one

consolidated

financial

statements:

Lizzy

toffee

now

see

that

I

think

that

I

will

do

me

to

it

that

we

have

guests

from

Ernst

and

Young,

who

will

have

a

presentation

and

from

our

staff

we'll

have

a

presentation.

Let's,

let's

hold

this

item

item

number

two.

The

sinking

fund

financial

statement

did

any.

There

is

no

presentation

on

that,

and

there

are

no

speakers.

A

A

D

Okay,

Thank

You

mr.

chair

I

will

present

the

financial

statements

for

the

year

ended:

December,

31st

2018.

We

also

have

Ernst

and

Young

with

us

today,

Susie

jean

jean

yak,

the

ey

partner

responsible

for

this

audit

and

the

audit

manager.

Lisa

go

Dane

they're

here

they

are

here

to

present

the

results

of

the

audit

after

I've

made

my

presentation,

Sivaji

Ernst,

&,

Young

Kimo,

presently,

a

total

of

vilification,

digital

finance

e.

At

a

conclusion,

the

map

presentation

suitable

any

fiscal

Scotty.

Are

they

sound

doom

industries.

D

So

the

city's

financial

status

remains

strong.

We

are

reporting

a

surplus

for

the

year,

ended

December,

31st

2018

of

609

million,

which

is

different

from

the

19

million

surplus

reported

at

the

end

of

2018

for

budget

purposes.

Financial

statements

are

reported

based

on

Canadian

public

sector

accrual

accounting

standards,

whereas

the

budget

is

reported

on

a

modified

cash

basis.

D

Their

surplus

is

higher

on

an

accrual

basis

because

it

recognizes

the

revenue

that

are

not

included

on

a

cash

or

budget

basis,

such

as

assets

contributed

from

developers

and

the

share

of

earnings

from

hydro,

also

on

an

accrual

basis.

Expenses

include

the

annual

depreciation

of

the

historical

cost

of

assets,

which

tends

to

be

lower

cost

than

what

is

contributed

to

capital

annually

on

a

budget

basis

to

replace

these

assets.

D

The

city's

overall

accumulated

surplus

increased

by

613

million

in

2018.

Most

of

that

increase

is

due

to

the

annual

surplus

overall

net

debt

has

increased,

but

so

has

the

value

of

non-financial

assets.

This

reflects

the

increased

investment

in

capital.

Our

net

debt

is

2.2

billion,

but

this

is

offset

by

total

non-financial

assets

of

16

billion.

This

represents

the

amount

to

service

future

generations

and

includes

our

tangible

capital

assets

and

reserves.

D

Less

future

liabilities

accounts

receivable

increased

merely

due

to

receivables

from

the

federal

and

provincial

levels

of

government

for

public

transfer,

public

transit

infrastructure

funding

PTF

and

at

the

combined

water/wastewater

funding

investment

in

government

business

enterprise

represents

the

net

assets

for

hydro

Ottawa,

which

we

report

on

a

financial

statements

on

an

equity

basis.

The

city

received

dividends

from

hydro

Ottawa

in

the

amount

of

22

million

in

2018

related

to

results

from

2017

operations.

D

On

the

liability

side,

we

had

an

increase

in

accounts

payable

and

accrued

liabilities,

which

included

additional

payables

for

Confederation

line,

as

well

as

additional

accruals

for

brownfields

relating

to

the

Zippy

development

on

the

Ottawa

River

deferred

revenue

primarily

includes

the

development

charges

collected,

but

not

spent.

It's

not

spent

yet

on

projects

that

were

intended

to

fund

in

2018.

There

was

an

increase

in

the

collection

of

development

charges

and

a

decrease

in

the

development

charge

transfers

to

projects

which

resulted

in

an

overall

increase

in

the

development

charge,

deferred

revenue.

D

So

employee

future

benefits

increased

this

year.

These

liabilities

represent

benefits,

earned

but

not

payable

until

future

years.

The

amount

payable

in

the

current

year

is

budgeted

for

each

year

and

changes

primarily

because

of

changes

in

actuarial

assumptions

and

legislation.

This

future

liability

is

an

estimation

and

may

or

may

not

reflect

the

actual

amounts

that

could

be

paid

in

that

future.

The

most

significant

changes

include:

post

retirement

and

post

employment

benefits

the

increase

by

39

million

dollars,

mainly

due

to

an

increase

in

long

term,

disability

claims

and

post

retirement

benefits.

D

D

When

you

look

at

the

debt

level

compared

to

the

total

costs

of

the

city's

gross

assets,

it

represents

eight

point:

nine

percent

of

those

assets-

that's

the

equivalent

of

a

thirty

five

thousand

dollar

mortgage

on

a

four

hundred

thousand

dollar

home

principal

and

interest

payments

are

restricted

in

two

ways.

Council

has

established

specific

targets

for

debt

and

whereby

principal

and

interest

payments

for

tax

and

rate

supported

debt

are

not

to

exceed

a

combined

target

of

eight

point.

Five

percent

of

the

city's

own

source

revenue

in

2018.

This

percentage

was

five

point.

D

Nine

six

percent,

the

provincial

measure,

looks

at

the

cost

of

debt

issued

including

mortgages

as

a

percentage

of

own

source

revenues,

and

that

limit

is

25

percent

in

2018.

This

measure

is

calculated

at

eight

point,

two

percent,

as

far

which

is

far

below

the

provincial

limit

compared

to

other

large

municipalities.

Ottawa

continues

to

have

one

the

lowest

total

debt

per

capita,

the

overall

value

of

the

assets

based

on

cost

increased

by

nine

hundred

and

eighty

eight

million

in

2018.

The

most

significant

construction

projects

contributed

to

the

increase

is

the

Confederation

Line

stage

one.

D

This

is

reported

under

assets

under

control

in

assets

under

construction.

It

was

a

four

the

value

about

one

hundred

fifty

six

million

Confederation

line,

Stage

two

also

reported

in

assets

under

construction

of

123

million

roads,

222

million

water

wastewater

infrastructure,

294

million

and

I

just

want

to

state

that

the

roads

number

also

includes

things

like

bridges

and

culverts.

So

it's

not

just

roads.

We

classify

other

assets

within

that

category,

as

you

can

see

from

the

chart,

water

and

wastewater

infrastructure

makes

up

20%

of

the

total,

tangible

capital

asset

net

book

value.

A

E

Thank

you

very

much

mr.

chair,

so

I'm

going

to

present

as

a

partner

on

the

audit

for

the

City

of

Ottawa

I'm,

going

to

present

our

audit

results

related

to

the

financial

statements

at

a

high

level.

We

are

substantially

complete

the

audit

we

do

completely

consider.

We

do

continue

our

procedures

until

June

12th,

which

is

the

date

when

Council

will

actually

approve

the

financial

statements.

So

we

will

inform

the

committee

if

anything

is

identified

in

that

period

we

have

you'll

see

in

the

financial

statements

our

draft

audit

opinion,

which

is

an

unmodified

opinion.

E

We

have

a

clean

audit

opinion

in

those

financial

statements

at

this

point

in

time

it

has

changed

in

its

structure.

If

you

look

at

it

so

that

the

actual

audit

report,

the

opinion

now

comes

first

and

then

the

basis

of

opinion

and

then

management

and

the

auditor's

responsibilities.

So

if

you

look

at

it,

it

has

changed

and

just

wanted

to.

Let

you

know

that

so

moving

into

our

presentation.

E

So

the

areas

of

audit

emphasis

are

generally

a

lot

of

the

larger

line

items

on

the

financial

statements

as

well

as

those

areas

where

there

are

significant

estimates.

The

first

is

the

revenue

recognition.

This

is

a

very

significant

line

item

at

4.1

billion

in

total

revenue.

We

look

at

different

types

of

revenue.

E

Investments

in

financial

instruments

is

another

area,

focus

they're

very

significant

at

the

city

at

approximately

1.2

billion,

so

we

do

confirm

that

the

investments

exist

with

the

custodian.

We

look

at

the

market

value

of

those

investments,

as

well

as

the

carrying

value

of

them,

and

we

look

at

whether

there

are

any

impairments

that

we

will

require

would

would

would

be

required

to

be

recognized

on

the

financial

statements

and

we

didn't

identify

any

issues.

E

Another

area

of

focus

is

employee

future

benefits.

There

are

a

lot

of

assumptions

in

employee

future

benefits

and

we

have

we

obtained

the

actuarial

valuation

from

the

cities

actually

actuaries,

and

we

actually

have

insight

in-house

actuaries

as

well

that

review

the

actuarial

valuation.

We

look

at

the

specific

assumptions

around

the

OC

Transpo

pension

plan,

the

CEO

SF,

so

superannuation

fund,

post

employment

and

retirement

benefits,

as

well

as

the

WSIB

accrual.

We

did

identify

two

differences

which

were

not

adjusted

on

the

financial

statements

are

corrected.

E

They

both

relate

to

issues

that

were

identified

in

prior

years

and

continue

in

the

current

year.

The

first

relates

to

the

superannuation

fund,

where

the

city

is

not

accruing.

The

cost

of

indexation

of

that

plan,

which

is

approximately

this

estimated

at

fifteen

point

five

million,

resulting

in

an

understatement

of

the

liability,

and

the

second

is

related

to

a

pre-existing

plan,

provision

of

approximately

6.5

million,

which

should

be

an

increase

to

the

liability

and

should

have

been

taken

in

a

prior

year,

but

is

being

amortized

into

the

liability

over

the

expected

average

remaining

service

life.

E

E

Other

area

focuses

tangible

capital

assets,

as

Isabel

mentioned.

These

are

a

significant

asset

on

the

financial

statements

at

16

billion

dollars.

So

we

do

do

a

fair

amount

of

work

around

additions,

disposals

amortization.

We

do

an

extensive

data,

analytic

program

with

all

of

the

data

from

the

city's

financial

statements

related

to

the

tangible

capital

assets,

and

we

also

review

significant

agreements.

In

this

case,

we

focused

on

the

Ottawa

light

rail

transit

agreement

and

how

the

costs

and

related

transfer

payments

and

commitments

were

recorded

in

the

financial

statements.

E

As

a

result

of

our

work,

we

did

identify

a

couple

of

differences

in

this

area

as

well,

both

again

related

to

prior

years

that

are

flowing

through

the

statements

in

the

current

year.

One

related

to

an

overstatement

of

the

depreciation

expense

in

the

current

year,

resulting

in

an

understatement

of

the

annual

surplus

of

15.5

million

and

the

second

related

to

an

overstatement

of

the

tangible

capital

asset

balance

of

approximately

13.5

million,

which

is

being

amortized.

It's

a

delayed

amortization,

so

it

is

resulting

in

an

understatement

of

the

annual

surplus.

By

about

point,

4

million.

E

We

focus

also

on

commitments

and

the

disclosure

related

to

commitments.

We

look

at

the

existence,

completeness

and

valuation

of

those

commitments

and

specifically

related

to

the

note

disclosure

in

the

financial

statements

and

we

focus

on

the

net

long-term

debt,

which

is

also

a

significant

balance

in

the

city's

financial

statements.

We

confirm

the

debt

the

occurrence

of

the

repayments.

We

verify

the

completeness

of

the

principal

and

the

related

disclosure,

as

well

as

the

interest

expense.

We

did

identify

a

difference

that

was

also

existed

in

the

prior

year.

E

Financial

statements

exist

again

in

the

current

year,

which

is

the

netting

of

225

million

of

long-term

receivable

with

long-term

debt.

We

would

generally

expect

this

to

be

shown

gross,

but

the

city

has

shown

at

net,

because

the

substance

of

the

transaction

is

that

these

two,

the

receivable

and

the

payable

mimic

each

other

in

their

payment

streams

and

are

expected

to

be

received

and

repaid

on

on

a

direct

essentially

directly

as

one

comes

in

the

other

goes

out

it.

The

same

is

done

with

the

interest,

income

and

expense

related

to

that

transaction.

E

It

does

result

in

an

understatement

of

total

financial

liabilities,

but

also

an

understatement

of

total

financial

assets.

So

the

net

impact

is

nil

on

the

net

debt

and

no

impact

on

the

annual

surplus

and

minimal

impact

on

the

city's

debt

service

ratio

in

the

final

area.

I

won't

go

into

a

lot

of

detail.

E

There

were

a

couple

of

other

myths

and

uncorrupted

differences

that

were

identified

primarily

related

to

payables

that

were

recorded

just

in

the

wrong

year,

so

essentially

a

cutoff

issue

which

results

in

an

overall

understatement

of

the

annual

or

surplus

of

approximately

4.4

million.

All

other

differences

were

corrected

by

management.

There

were

five

new

accounting

standards

implemented

by

the

city

this

year

and

we

were

comfortable.

E

F

E

F

F

D

For

this

cos,

f-fine

it

fund

itself

funds

55%

of

the

indexation,

the

city

annually.

We

put

in

our

budget

the

remaining

45%

to

bring

it

up

to

100%,

that's

approved

every

year

as

part

of

the

budget.

At

any

point

in

time,

Council

could

decide

not

to

supplement

that

amount,

and

so

that's

why

we

don't

show

it

as

a

future

commitment.

Okay,.

G

G

The

one

thing

that

I

noted

was

in

terms

of

as

people

move

on

to

retirement

the

the

expense

of

long-term

disabilities

and,

of

course,

if

there's

any

major

changes

coming

up

due

to

pressures

from

provincially

we're

going

to

have

more

of

that.

Is

this

something

that's

just

sort

of

getting

more

out

of

control

that,

in

terms

of

the

the

costs

of

actually

laying

people

off.

D

Are

you

responding

to

the

future

benefits

and

liability

yeah

that

that

is

an

amount

that

increases

with

each

of

the

claims?

So,

for

example,

you

WSIB

and

Ltd

for

those

claims

we

add

additional

liability

for

future

claims,

there's

an

actuarial

assumption

and

estimation

done

for

those

future

claims

every

year.

Those

claims

are

increasing

and

that's

what's

reflected

what

that's

what's

reflected

in

those

increases.

So.

D

H

Thank

you,

Thank

You,

mr.

chair

and

just

follow-up

on

the

council's

Kavanagh.

So

I

almost

I

asked

the

same

question

daily

about

the

unfunded

liability.

Are

we

in

in

compared

to

other

municipality

of

our

size?

Are

we

have

enough

funding

forceful

for

that

fire

for

the

unfunded,

because

one

thing

becomes

heaven

I'll

touch

on

and

I

think

it's

not

just

in

all

municipalities

cross

everywhere.

There

is

more,

you

know

more

you

paying

sometimes

more

than

but

you

have.

D

So

then

we

completed

a

full

review

of

our

reserves

and

the

unfunded

benefits

liability

was

one

of

them.

M&Amp;P

came

in

and

looked

at

our

risk

using

a

risk

management

framework.

Looking

at

what

is

how

much

do

you

want

to

put

us

out?

You

don't

want

to

put

a

hundred

percent

of

that

liability,

because

it

is

just

an

estimate.

D

You

want

to

put

away

a

reasonable

amount,

and

so,

in

those

years,

when

you

are

short

in

your

budget,

you

could

draw

down

on

those

reserves

and

the

they

recommended

that

we

maintain

I

believe

it

was

around

twelve

percent

of

the

overall

liability

as

a

reserve

and

the

remain

would

reign.

There

would

be

unfunded

and

that

was

based

on

best

practices.

Okay,.

H

So

it,

and

so

we're

still

followed

the

best

practice

without

the

other

question

is

about

the

22

million

dollar.

You

talk

about

the

the

endowment

from

hydro

investment.

You

said,

22

million.

Is

that

a

set

number

or

I

thought

the

number

was

anything

over.

20

million

can

go

back

to

the

operation

because

some

some

of

our

card

put

something

to

that

perspective

to

be

spent

if

it's

over

20

million,

but

in

me,

is

when

you

mention

22.

Is

there

a

set

number

in

your

mind

so.

D

That's

it's

actually

I

rounded

up

it's

twenty

one

point:

nine

million

and

that's

what

we

would

have

received

in

20:18,

reflecting

2017

operations,

anything

over

the

20

million,

but

in

our

financial

statements

we

report

the

full

21.9

and

then

but

anything

over

and

above

the

20

million.

That's

what

we

would

use

for.

Yeah

and

Marian

can

answer

at

the

row.

So

counselor.

I

There's

two

things

with

Hydra:

one

is

the

endowment

fund

and

that's

where

your

200

million

reference

is

to

and

we

earn

six

and

a

half

percent

on

that

fund,

but

that's

not

part

of

what

they

that's

just

part

of

normal

operations.

What

they're

referring

to

is

the

actual

dividend

itself

and

we

budget

every

year,

20

million

for

the

dividend,

and

last

year

we

received

21.9.

So

that's

the

reference

so

there's

there's

actually

two

sources

of

funding

coming

in

from

one

directly

from

hydro

and

one

from

when

we

basically

cashed

in

the

debt

several

years

ago.

I

J

A

Thank

you

very

much.

I

have

a

couple

of

questions

and,

and

it

picks

up

on

counselor,

Cavanaugh's

and

counsel

else,

Antares

questions

with

respect

to

future

liabilities

and

pension

and

health

I

see

on

our

report

on

page

26,

page

29,

I,

believe

health

care

inflation

rate

is

currently

at

2%

and

future

5.9

percent.

D

That

this

is

these

are

amounts

that

are

developed

by

our

actuaries

immerser,

conducts

a

review

every

three

years

and

provides

these

estimates.

There's

three

inflation

estimates

there's

one

for

overall

inflation,

which

is

at

2%,

there's

a

salary

increase

estimate

of

one

point:

nine,

nine

to

two

point:

five:

the

five

point:

nine

was

actually

graded

down

to

four

percent

and

that's

the

one

related

to

inflation

rate

related

specifically

to

health

care,

so

they

have

an

inflation

rate

associated

with

the

healthcare

costs

and

it

was

at

five

point:

nine.

A

A

E

Do

in

the

city

engages

actuaries

to

do

the

evaluation,

and

then

you

I,

as

part

of

our

audit

process,

has

internal

actuaries

as

well.

That

review

the

city's

actuaries

valuation

and

particular

look

at

the

assumptions

and

make

sure

they're

reasonable

and

resulting

in

an

appropriate

liability

on

the

financial

statements.

A

Since

the

close

of

these,

since

the

closes

these

financial

statements,

there

was

a

significant

accident

and-

and

we

were

served

with

a

notice

of

lawsuit

yesterday-

and

the

provincial

government,

which

is

a

funder

of

the

City

of

Ottawa,

has

has

said

that

there

there

would

be

cuts

and

then

they

reversed.

How

does

this

enter?

How

do

these

events

enter

into

your

report

with

respect

to

subsequent

events

and

future

liabilities?

Are

you

able

to

to

provide

us

assurance

that

you

you

are

that

these

are

accounted

for

and

reported

on.

E

So

the

event

happened

after

the

UN,

so

it

is

a

subsequent

event.

We

look

at

whether

it

is

determinable

and

whether

an

estimate

can

actually

be

made

at

this

point

in

time.

We

wouldn't,

as

we

wouldn't

accrue

in

the

2017

financial

statements,

because

the

event

took

place.

Sorry

in

the

2018

financial

statements,

because

the

event

took

place

in

2019,

but

it

is

something

that

is

caught

up

in

your

general

disclosure

related

to

your

contingent

legal

liabilities

and

I.

E

E

G

Thank

you,

I

have

a

question

in

terms

of

the

surplus

for

most

people

out

there.

They

look

at

the

numbers

and

they

see

that

in

2018

we

have

a

higher

annual

surplus

and

wonder.

You

know

why

we

didn't

spend

more

money

on

on

programs

etc,

and

one

of

the

biggest

factors

that

we

saw

in

terms

of

what

we

expect

will

see

more

spending

on

is

winter

maintenance

it's

a

beautiful

day

outside

today,

but

we

know

all

know

how

much

work

and

and

how

much

effort

it

took

this

winter

on

winter

maintenance.

D

Yes,

so

there's

a

difference

between

what

we

budget

and

what

we

report

in

terms

of

our

financial

statements.

Financial

statements

are

reported

on

an

accrual

basis,

and

it

includes

non-cash

items

so

for

I

would

give

an

example

contributed

capital

developers

put

in

assets

on

behalf

of

the

city.

That's

considered

contributed

capital,

it

shows

us

as

a

number

within

our

surplus,

but

it's

not

money

that

actually

came

over

to

the

city

that

we

have

to

spend,

and

so

what

that's?

G

Thank

you,

I'm

used

to

school

board

where

a

surplus

meant

that

we

have

our

enrollment

went

up

and

it's

always

hard

to

predict,

and

you

know

it's

one

of

those

things

that

we

we

don't

know

in

advance

and

we

just

have

to

budget

as

close

as

possible.

So

so

it's

a

little

different

here,

but

but

in

terms

of

overall

spending,

it

looks

like

that.

We,

you

know

we

could

have

spent

a

bit

more

like

on

our

programming,

because

that's

a

significant

difference,

almost

50%

more

from

the

year

before

it

was,

it

was

I.

G

D

When

I

just

need

some

clarification,

when

you

say

50%

more,

you

talk

about

the

462

million

versus

the

609

again,

those

are

mostly

non-cash

of

reflections.

The

the

surpluses

were

like

on

a

cash

basis.

The

surpluses

were

fairly

consistent

between

2017

and

2018,

so

it

would

have

been

additional,

contributed

capital

and

changes

in

depreciation

and

those

non-cash

items.

Okay,

so

in.

A

Budget

is

done

on

a

cash

basis,

while

the

the

financial

statements

are

done

on

an

accrual

basis,

and

thus,

the

and

and

in

in

your

report,

there's

a

reconciliation

of

those

yes,

which

perhaps

we

could.

We

could

talk

about

with

any

any

interested

member

of

counsel.

How

that

copy

of

that?

Oh,

thank

you

so

making.

A

Thank

you

seeing

no

further

questions.

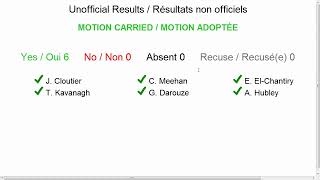

The

report

recommendation

is

that

the

Audit

Committee

recommend

Council

approved

the

draft

2018

City

of

Ottawa

consolidated

financial

statements.

Is

that

carried

carried?

Thank

you

very

much,

and

thank

you

very

much

for

your

free

report

and

for

your

service

on

to

item.

Excuse

me

on

to

item

number

three

and

the

office

of

the

Auditor

General

report

on

audit

follow-ups,

and

while

they

are

while

are

the

Auditor

General

is,

is

taking

a

seat.

I

will

ask

the

vice

chairman

to

introduce

a

motion.

Please.

A

Thank

you

for

sharing

that

Carrie

Carrie.

Thank

you.

So

the

Auditor

General

is

going

to

present

a

report

on

six

audits,

six

audit

follow-ups

that

he

and

his

office

have

completed

and

in

discussion.

We

will

stop

at

the

end

of

each

audit

for

questions

by

members

of

the

committee,

and

that

is

because

for

continuity

and

efficiency,

and

because,

as

I've

said

before,

we

will

be

revolving

into

into

a

closed

session,

and

so

I

will

leave

that

to

the

artery

general.

Please

I.

B

B

B

I'm

joined

at

the

table

by

the

two

deputy

Auditor

General's,

Sonya,

Brennan

and

ed

minor

Illya.

Do

verification

that

eyelash

wanna

be

sure

ed

minor,

a

Madame

Sonja

Brennan

I'd,

also

like

at

this

time

to

I,

know

be

going

in

in-camera

at

the

end,

but

I

didn't

want

to

go

any

further

without

thanking

the

efforts

put

into

these

into

this

work

by

the

staff.

The

the

management

and

the

staff

provide

time

to

us

when

we

do

the

audits

and

then,

of

course,

the

provide

time

to

us

again

later

when

we

do

the

the

follow

ups.

B

So

mr.

chair

I

would

like

to

to

reiterate

the

the

process

that

we

go

through

in

the

field

work,

whether

we're

doing

an

audit

or

whether

we're

doing

a

follow-up.

We

always

kick

off

our

our

project

with

a

meeting

with

staff,

and

then

we

provide

debriefings

throughout

the

course

of

our

work

and

they

can

be

they

can

be

anytime,

and

once

we've

completed

our

work,

we

debrief

the

management

of

the

area

under

audit

or

under

follow-up.

B

We

and

we

indicate

our

findings.

We

prepare

a

draft

report,

it's

sent

to

a

staff

for

fact

review

and

that

that

can

take

four

to

five

weeks,

depending

on

the

complexity

of

the

of

the

area

under

review.

And

then

we

prepare

a

final

report

where

we

require

management

comments

and

once

again,

that

can

take

another

four

to

five

weeks.

Now

that

time

period

can

change

depending

on

activities

within

the

area

under

review,

and

there

are,

there

have

been

instances

where,

for

example,

an

activity

like

the

flood.

B

B

So

the

standards

also

indicate

that

the

timing

and

scope

of

both

audits

and

follow-ups

or

at

the

discretion

of

the

Auditor

General

but

I,

can

assure

you

that

that

before

we

do

any

work,

we

absolutely

make

sure

that

we

provide

adequate

notice

before

we

go

in

and

we

ensure

that

we're

not

going

to

that.

We're

going

to

minimize

the

effect

on

the

operations

of

the

the

area

under

review.

B

So

Michelle

appraises

now

the

processes

the

verification

can

park

at

f--

as

the

lake

at

faso,

la

planificación

de

travis,

related

a

elective,

let

abysmal

the

report,

a

finalement

of

has

the

suivi

larezo.

Also

do

a

poor

marino,

say

the

discreet

a

lease

we

V.

There

are

four

phases

in

in

our

audit

process.

The

planning

phase

the

fielding

fieldwork

phase

before

we,

where

we

actually

go

in

and

do

the

work.

B

The

reporting

phase,

where

we

developed

a

draft

report

and

a

final

report,

and

we

present

that

to

the

council

in

our

annual

report,

as

we

did

last

month

and

then

the

follow-up

phase

and,

of

course,

today

we're

presenting

reports

from

that

final

phase.

So

we

conduct

follow-up

reports

on

all

audits

and,

as

I

indicated,

we

generally

wait

to

three

years

after

an

auto

report

is

completed,

to

provide

ample

time

for

the

management

to

implement

the

recommendations

and

the

follow-up

really

closes

the

circle.

B

B

We

present

an

audit

report

and

then

management

promises

to

counsel

in

that

out

report

that

they're

going

to

implement

those

recommendations

within

a

certain

time

period,

and

then

we

do

this

follow-up

to

check

on

the

promises

that

were

made

to

to

counsel,

and

we

report

back

to

committee

and

counsel

with

the

with

the

the

progress

on

that

implementation,

leras

or

the

suivi.

The

verification

permit,

the

beautiful

guru,

the

verification

general,

the

very

FINA

program,

complete

paladin,

actual

survey,

they

project

the

verification.

B

B

So

when

we

did

those

three

audits

in,

I

T

we

brought

in

outside

experts

to

help

us

to

perform

that

audit,

and

we

indicated

that

to

you

when

we

provided

the

reports,

and

it's

no

surprise

that

that

we

brought

in

experts

from

KPMG

to

assist

us

in

the

the

follow-up

to

those

audits

to

ensure

that

we

had

acknowledged

experts.

Looking

at

that

area

of

expertise.

B

Looking

at

that's

a

subject

area,

the

final

item

will

be

provided

in

camera

when

we

presented

that

audit

a

couple

of

years

ago,

that

audit

was

was

presented

in

camera

and

there

will

be

no.

There

was

no

reporting

out

and

other

than

indicating

the

progress

on

the

recommendation.

So

far

on

that

audit

everything

will

be

presented

in

camera.

B

So

saluted

I

can

use

agave,

it's

say,

Claire

the

direction

of

Sargassum

respect

a

and

the

process.

The

verification

and

I

can

confirm

to

our

committee

that

management

continues

to

be

committed

to

the

audit

process

and

you'll

see

that

there

has

been

some

progress

on

implementation

of

the

recommendations

in

all

of

the

reports

that

that

were

providing

here,

Sankranthi

spore,

so

they

recommend

a

she

also

completed.

A

third

set

for

Sunday

recognize

Sharon

santanico.

B

Mr.

chair

50,

56

percent

of

the

the

recommendations

from

the

six

audit

reports

of

representing

today

are

complete

and

37

percent

of

the

recommendations

are

in

process

parameter,

mala

verification.

The

Persian

the

lecturer

at

MIT

is

eight.

They

can

tell,

though,

the

gestural

implement

a

tool,

a

recommendation

or

don't

pour

new

in

the

public

who

the

who

know

the

ideas,

so

no

verification.

K

Morning

sure

the

first

report

that

were

giving

the

results

of

our

follow-up

on

is

the

audit

we

did

of

the

automated

meter

reading

project

that

audit

can

conclude

for

recommendations

and

we

found

that

all

of

them

had

been

fully

implemented.

So

we

have

no

real

further

detail

comments,

although

we

willing

to

entertain

any

questions,

should

there

be

any

gave.

L

Good

morning,

mr.

chair,

the

original

audit

of

accounts

payable

was

an

independent

assessment

of

the

control

framework

in

place

for

the

processing

of

City

payables.

In

this

audit

opportunities

were

identified.

Opportunities

were

identified

in

the

use

of

potential

use

for

more

automation,

with

the

technology

already

available,

to

drive

greater

process

efficiency

and

to

maximize

potential

cost

savings.

We

also

identified

areas

where

there

were

specific

controls

that

we

felt

should

be

strengthened

in

this

process.

L

Seven

recommendations

were

made

in

our

report

in

the

follow-up

you'll

see

that

we

concluded

to

were

fully

complete

three

partially

complete

one

not

started,

and

one

no

longer

applicable.

With

respect

to

the

three

partially

completed

recommendations.

The

audit

we

recommended

that

for

a

key

control

where

enhanced

system

access

is

granted.

So

this

is

within

the

financial

system,

si

P

there

is

ability

for

users

to

have

what's

called

enhanced

system,

there's

a

risk

with

this

type

of

access

in

the

granting

process.

So

there

are

specific

controls

around

it.

L

Where

there's

a

check

to

make

sure

the

conflict

is

within

a

sort

of

a

risk,

tolerance

and

then

it's

it

appropriately

approved.

We

had

recommended

that

when

this

occurs,

there's

a

procedure

written

and

that

it's

documented

that

this

has

been

done

by

the

employee

responsible.

What

we

found

in

our

testing

is

that

the

documentation

wasn't

consistently

kept,

so

there

was

no

way

to

assure

whether

or

not

the

actual

control

would

be

carried

out

every

time.

L

So

in

summary,

there

wasn't

really

assurance

that

the

penalties

were

being

recorded

or

tracked

and

really

the

the

reasoning

behind.

That

was

that

you

know

if

we're

tracking

those

expenses

management

can

see

that

they're

incurring

charges

that

are

unnecessary

and

they

can

take

actions

to

prevent

that

from

occurring

again

and

and

third

item

that

was

partially

complete.

The

original

audit

recommended

that

the

city

leverage

existing

technology

to

automate

monitoring

of

potential

discounts,

so

another

potential

for

cost

savings

on

invoice

payments.

L

The

system

enhancements

they

were

deferred

and

they'll,

be

addressed

with

a

new

solution.

So

the

existing

solution,

where

this

was

to

take

place,

is

being

replaced.

A

management's

indicated

that

will

occur

sometime

in

2020,

so

they've

deferred

that

particular

action

and

we'll

we'll

look

to

address

it

in

the

with

a

new

solution.

L

In

terms

of

the

item

that

we've

assessed

has

not

started.

We

had

we'd

recommended

and

management

agree

that

a

control

related

to

fraud

risk

and

this

control

is

around

the

ability

to

change

sensitive

what

we

call

vendor

master

information.

So,

within

the

financial

system,

there's

a

database

of

the

vendor

information,

so

vendors

name,

address

and

banking

information,

so

the

ability

to

change

this

information

has

to

be

carefully

controlled

and

with

appropriate

approvals,

we

had

recommended

that

the

they

embed

the

control

right

in

the

system,

so

there's

no

bypass.

L

It's

it's

right

right

in

the

system

and

the

the

user

or

the

administrator

can't

can't

change

the

information

without

appropriate

approval,

and

that

approval

involves

seeing

that

there's

adequate

documentation

for

that

changes

were

made

to

the

process,

but

we

didn't

they

didn't

they

weren't,

specifically

the

same

as

what

we

we'd

recommended.

In

our

opinion,

they

didn't

address

that

that

area

of

risk

management

is

indicated

that

again

with

the

new

solution

that

they

would

that

they

would

address

this

particular

item

with

that

implementation.

L

L

That

means

what

we

had

found

that

there

was

there

was

no

way

to

to

prevent

or

detect

a

situation

when

a

vendor

when

an

invoice

from

a

vendor

was

paid

with

a

p-card.

If

that

vendor

also

emailed

the

invoice

directly

to

accounts

payable,

it

could

be

processed

again

and

paid

without

necessarily

being

noticed.

L

This

was

a

weakness

in

the

control

area

that

that

was

already

known

by

accounts

payable

they'd

indicated

that

they're

looking

on

a

way

to

to

resolve

the

issue

and

automate

the

information

so

that

they

could

they

could

analyze

and

detect

whether

or

not

there

are

any

duplicates

paid.

Through

this

method,

we

recommended

that

they

notify

purchasing

card

users

of

this

risk.

L

We're

not

sure

that

people

knew

that

this

was

a

possible

risk

to

let

them

know

that

they

were

responsible

to

put

in

a

process

to

make

sure

that

they

prevented

duplicate

payments

that

could

occur

through

this

method.

We

have

seen

that

that

notification

has

been

done

so,

as

you

you've

heard

there,

a

number

of

actions

incomplete

and

some

of

which

will

be

addressed

by

solution

replacing

the

existing

technology

in

in

approximately

a

year's

time.

So

I

can

answer

any

questions.

If

you

have

any

so.

F

L

It's

the

responsibility

of

the

cardholder,

so

each

business

area

has

people

responsible

for

the

purchasing

cards

and

then

they

may

have

say

more

other

people

who

are

processing

payments

through

the

system.

So

if

one

doesn't

see

the

other

and

an

invoice

is

sent

twice

or

pay,

it

could

be

paid

two

times.

F

F

Well,

do

we

agree

that

it

doesn't

make

sense

that

the

cardholder

does

not,

like

you

know,

Kevin

while

he's

here

he's

got

people

that

have

a

credit

card

to

go

out

and

get

you

know

what

they

have

to

buy

plywood

to

fix

something.

Why

should

they

be

responsible?

Make

sure

that

the

the

building

supply

company

doesn't

send

an

invoice

in

through

finance

I'm,

not

following?

Why

wouldn't

we

make

a

recommendation

that

accounts

payable

takes

responsibility

for

that?

The.

L

It's

within

the

business

process

they've

set

up,

who

has

responsibility

to

pay

invoices

or

control

and

monitor

purchasing

cards,

so

really

the

the

recommendation

that

we

made

isn't

specific

to

who

exactly

carries

it

out,

but

each

business

unit,

the

that

responsibility

and

they

all

do

they

need

to

look

at

what

they're

doing

and

make

sure

that

between

the

nut,

the

different

people

who

approve

payments

that

they

have

something

in

place

that

will

will

detect

these

things.

We

didn't

specify

that

it

was

the

purchasing

card

holders

because

it

may

not.

L

M

Mr.

chair,

it's

the

responsibility

of

the

person

making

the

purchase,

whether

they're,

paying

with

a

purchasing

card

or

approving

an

invoice

to

make

sure

that

they

are

only

approving

that

invoice

once

and

that

the

invoice

is

correct

and

they've

received

the

goods

and

they're

to

the

satisfaction

in

the

city

and

so

whether

that's

being

received

by

an

invoice

through

accounts

payable.

That

would

then

be

workflow

to

the

user

or

with

the

purchasing

card

directly.

It's

that

individual,

that's

responsible

for

ensuring

the

correctness

of

the

payment.

F

So

if

it

comes

in,

let's

use

that

scenario

I

drew

them

and

I

hope

Kevin

doesn't

mind,

we'll

use

them

as

an

example.

If

he

makes

a

purchase

on

the

card,

he's

obviously

responsible

to

make

sure

that

the

proper

documentation

of

that

purchase

with

the

card

is

submitted

for

approval,

but

if

they

send

an

invoice

they

be,

and

let's

say,

cash-

wait

because

they're

out

of

business,

okay,

cash

weigh

sends

an

invoice

to

the

City

of

Ottawa.

F

M

M

F

M

F

M

Mr.

charity,

the

account

to

capture

the

late

fees

was

created.

The

finding

was

around

the

communication

around

how

that

information

is

coded

in

the

system.

That

communication

has

been

updated

as

part

of

the

contract

administration

policy

and

associated

training

that

was

developed

in

response

to

the

audit

of

Road

services,

where

we

go

through

the

responsibilities

of

invoice,

receipt

and

approval

and

the

associated

components.

But.

M

That's

right:

this

is

ongoing

training,

that's

going

to

be

provided

regularly.

We

are

providing

this

this

training

across

the

corporation.

In

addition,

as

a

result

of

changes

made

to

the

construction

act,

which

are

implementing

a

prompt

payment

regime

and

associated

penalties,

we

are

working

with

our

high

volume

invoice

approvers

to

ensure

that

they

have

a

process

to

pay

their

invoices

in

accordance

with

the

legislation

and

not

incur

late

fees.

B

B

M

The

contract

administration

policy

was

finalized

in

December

of

last

year

and

the

training

is

being

implemented

throughout

this

year,

beginning

with

Road

services

and

then

across

the

corporation,

so

not

everybody's

at

each

other.

Not

everyone

has

received

the

training

yet,

but

the

policy

is

in

place

which

governs

all

contracts.

F

Okay,

not

everybody

is

trained.

Yet,

what's

the

timeline

to

get

everybody

trained

and

on

important

issues

such

as

late

fees,

would

it

not

make

sense

to

send

some

sort

of

a

memo

out

as

well

so

that

they

know

the

ones

that

are

using

it?

I

think

you

said

the

high-volume

users

are

being

trained

first

or

no.

That.

M

That

is

correct

in

it

well,

in

accordance

with

the

construction

act

changes.

So

what

I

would

say

is

that,

as

part

of

the

contract

Paul

that

contract

administration

policy

update,

communication

was

sent

out

across

the

corporation,

including

through

management

updates,

to

make

sure

that

those

people

that

are

responsible

for

administering

contracts

understand

their

roles

and

responsibilities.

M

In

addition,

we

have

an

another

layer

of

training

which

goes

through

not

only

invoice

approval

processes,

but

also

dealing

with

supplier

performance

and

in

general

contract

administration,

which

we

are

rolling

out

as

an

enhanced

level

of

training

over

and

above

the

policy.

So

the

communication

has

been

forwarded

across

okay.

Thank.

F

You

so

my

last

question

and

is

on

the

I

believe

two

of

the

six

recommendations.

At

the

time

of

your

follow

up.

Mr.

auto

general

I

believe

two

of

the

six

recommendations

were

done

and

when

I

read

the

report,

it

says

they're

following

up

on

the

other

four,

but

isn't

that

typically,

the

response

of

the

original

audit

I'm

a

little

concerned

that

that's

what

you're

getting

at

the

follow-up

stage,

because

shouldn't

everything

basically

be

implemented

by

the

time

you

do

the

follow

up

as

a

not

the

expectation.

B

Mr.

chair,

when

we

decide

to

to

do

our

follow

ups,

we

look

at

the

the

management

comments

from

the

original

audit

where

they

indicated

when

they

would

be

implementing

the

the

solutions

to

the

recommendations

and

that's

why

we

give

two

to

three

years

generally

before

we

go

in

to

do

that

work.

This

audit

was

presented

in

2015

and

we

did

our

work

in

the

late

summer

and

fall

of

2000

and

and

18,

and

this

was

what

we

found

that

some

of

the

items

hadn't

been

completed.

Thank.

F

M

Mr.

chair,

following

the

audit,

there

were

two

unexpected

changes

in

the

technology

marketplace,

both

on

how

si

P

administers

its

payment

modules

and

a

notice

to

the

city

that

the

mark

view

system