►

From YouTube: Focus On #07 | RWF Lending Principles

Description

For the 7th episode of Focus On, we will host Eric Rapp from the RWF Core Unit.

Eric will lead a deep dive into more of the nuanced lending principles in play for RWAs, including:

• Crypto Lending Comparison

• RWA Risk Assessment

• Investment Grade Standard

• Structuring an Investment Grade Senior Loan

• Arm’s Length Transaction Standard

• Case Study

We will conclude with a Q&A to answer any follow up questions from the discussion.

A

Eric

is

going

to

be

presenting

the

real

world

asset

lending

principles

that

he

and

his

team

uses

to

evaluate

real

world

asset

details

and

touch

on

the

monitos

risk

profile

a

little

bit

at

the

end

of

the

conversation

using

it

as

a

case

study

to

facilitate

our

conversation

here.

As

you

have

questions,

please

feel

free

to

drop

them

in

the

chat

or

the

qa

function

and

we'll

address

them

during

a

pause

in

the

action

or

at

the

end.

So

with

that

eric

the

floor

is

yours.

Let

me

get

your

screen

share

here

and

take.

B

It

away

is

it:

are

we

shared

okay,

all

right,

good

hi?

My

name

is

eric

rapp,

I'm

in

the

rwa

group.

You

know

in

terms

of

background

I've

been

in

traditional

finance

in

various

shapes

and

forms

by

about

20

plus

years.

You

know,

lately

I've

been

more

in

fintech

and

then

now

in

d5,

and

I

just

want

to

share

with

folks.

You

know

in

the

rwa

group.

How

do

we

think

about

looking

at

you

know:

potential

transactions,

you

know

at

the

end

of

the

day

maker

is

basically

a

senior

lender.

B

Hopefully

senior

secured

you

know,

and

how

do

you

look

at

this?

You

know

what

are

kind

of

the

principles.

What

are

some

of

the

key

processes

you

know?

Hopefully

this

will

help

folks

get

a

better

idea

of

how

we

look

at

things.

You

know

we're

certainly

open

to

innovation

and

criticism.

You

know

we're

not

saying

we

have

the

only

way.

On

the

other

hand,

I

will

say

yes

a

lot

of

what

we're

using

has

been

developed

in

the

real

world

for

hundreds

of

years.

People

have

lost

a

lot

of

money

over

the

centuries.

B

You

know

not

doing

things

certain

ways

and

there's

a

rough

way

of

doing

things.

It's

not

perfect,

but

I

think

there's

some

key

principles

that

that,

if

you

want

to

innovate,

you

should

learn

the

key

principles

in

the

real

world

first

and

then

figure

out

where

you

best

think

you

can

break

them

and

not

because

you

don't

want

to

innovate

and

how

to

find

ways

to

lose

money,

okie

doke.

B

So

in

terms

of

the

outline

here,

I

want

to

first

talk

a

bit

about

how

it

is

crypto

lending

kind

of

the

maker

core

product

compared

to

real

real

world

lending.

There's

some

similar

similarities

and

there's

some

definite

differences.

Then

I

want

to

talk

a

bit

about

the

investment

grade

standard.

You

know

it's

what

we're

roughly

trying

to

hit,

then

I

want

to

talk.

You

know

more

about

how

do

we

actually

assess

risk

a

bit

more

sense

of

the

process?

B

B

You

know

say:

there's

a

100

loans

of

a

million

dollars

each

and

they're

not

investment

grade,

but

if

you

put

them

all

together

can

maybe

the

top

70

or

80

percent

b

investment

grade.

You

know,

assuming

the

other

part

of

it.

You

know,

takes

all

the

losses

and

absorbs

the

risk.

First,

that's

part

of

the

magic.

B

Then

you

know

I

want

to

talk

a

bit

about

the

monetalist

facility

in

terms

of

risks.

You

know

returns

and

how

does

it

compare

in

in

terms

of

how

we

look

at

it?

I

I

know

there's

been

a

lot

of

publicity

in

the

forum

about

it,

so

I

I

think

it's

very

fair

to

trying

to

give

folks

a

sense,

our

perspective.

It's

not

the

only

perspective.

You

know

we're

not

the

a

or

nay,

but

using

these

different

tools,

we

will

have

gone

through

we're

going

to

apply

into

monetalis.

B

Then

I

want

to

talk

a

bit

about

an

arm's

length.

Transaction

standard,

which

I

think

is

is

a

key

thing

and

I'll

explain

why

down

the

road

then?

Finally,

let's

talk

a

bit

about

die

stability

risk.

I

think

some

of

these

topics

are

quite

in

depth

and

can

have

their

own

discussion

site.

I.E,

die

stability

risk,

but

it's

it's

a

concept.

We

really

need

to

use

when

thinking

about

making

loans

to

different

counterparties.

B

So

with

that

in

mind,

I

will

take

it

away

all

right.

So

when

we

think

about

makers,

crypto

lending

business,

you

know

what's

our

basic

strategy,

you

know

how

does

maker

get

comfort

that

it's

gonna

get

paid

back

almost

all

the

time,

because

you

know

at

the

end

of

the

day,

what

are

our

vaults

maybe

yield

two

or

three

percent,

so

if

you're

only

getting

two

or

three

percent

a

year

for

the

risk

you're

taking

that

kind

of

tells

you

you

know,

you're

you're

only

going

to

make

money.

B

If

you

get

your

money

back

almost

all

the

time,

you

know

if

you're

losing

money,

10

percent

of

the

time

you're

probably

coming

out

underwater.

Needless

to

say,

I

think

we're

doing

a

good

job

because

we're

consistently

making

money,

but

keep

that

in

mind

if

you're

only

earning

a

small

amount.

You

know

per

year

on

your

assets,

you

know

your

loans

like

two

or

three

percent,

that

pretty

much

tells

you

how

much

risk

you

can

take.

B

You

know

I.e

not

much.

If

you

were

earning

20

or

30

of

your.

You

know

on

your

assets,

you

could

take

a

different

type

of

risk

all

right.

So

how

do

we

loan?

How

do

we

make

crypto

loans?

You

know

if

you

want

to

open

a

vault

with

your

bitcoin

or

eth

one,

it's

gonna

be

supported

by

a

crypto

asset.

That's

locked

in

our

vault,

so

it's

secured

is

what

we

would

say.

You

know

maker

controls

that

collateral

maker

controls

that

specific

crypto

assets.

B

So

if

there's

any,

you

know

issues

about

getting

repaid,

we

were

the

first

person

to

hold

it.

That's

a

big

big

deal

in

the

lending

world.

You

know

you

could

probably

say:

90

of

of

of

the

law

is

who

possesses

the

assets

and

since

we

have

it

locked

in

our

crypto

vault,

we

possess

it.

Big

deal

two

another

big

deal

is

senior

in

a

sense,

we're

the

only

creditor

supported

by

that

asset,

or

at

least

we're

the

only

creditor

who's

allowed

to

get

paid

back

from

that

asset

in

our

vault.

B

Until

we're

all

you

know,

until

we're

made

whole

you

know,

maybe

they

have

someone

else

who

they

owe

money

to,

but

the

other

creditor

has

no

rights

or

has

no

ability

to

get

to

that

collateral.

Until

we're

happy

that

we've

been

paid

off

senior

and

secured

big

big

deals

and

over

collateralized,

you

know

again

say:

if

we

had

a

million

dollar,

we

loaned

a

million

dollars

to

someone

on

eath.

You

know

each

is

pretty

pretty

risky.

You

know

you've

seen

days

when

it

could

be

down

five

or

ten

percent.

B

So

we,

if

we

loan

someone

a

million

dollars

in

each

you

know

we

probably

want

to

have

what

a

at

least

a

million

three

a

million

for

you

know

you've

got

this

extra

collateralization,

so

you

know

things

go

a

little

sideways.

You

know

prices

of

the

east

decline.

You

still

have

enough

to

get

out

of

there

timely

and

get

all

your

money

back

again.

B

These

are,

I

think,

defining

principles

of

crypto

lending

and

also,

I

think

these

you're

gonna

see

these

are

defining

principles

in

most

lending

and

now

these

next

three

are

defining

principles

in

crypto,

but

less

so

in

our

real

world

assets.

One,

it's

fungible,

you

know

like

a

bitcoin

is

a

bitcoin.

You

know

each

is

so

the

secure

assets

are,

you

know,

they're,

all

homogenous,

at

least

in

their

group.

This

is

all

bitcoin.

This

is

all

leave.

We

know

exactly

what

it

is.

You

know,

there's

nothing

really

idiosyncratic

too

transparent.

B

The

prices

of

these

you

know

be

a

bitcoin

or

eth

are

observable

and

frequently

updated.

You

know

these

things

tend

to

trade

24

7

worldwide.

So

you,

you

know,

we

know

as

a

lender

what

the

price

is

at

any

given

time,

and

you

know

we

can

see

if

the

the

debt

ceilings

are

starting

to

come

under

pressure.

You

know,

is

it

time

you

know

to

have

a

liquidation,

you

know,

does

it

hit

the

trigger

level

again?

This

is

a

very

big

deal

because

you

know

what

your

collateral

is.

B

You

know

what

it's

worth

and

you

know

you

can

get

out

quickly

and

you're

over

collateralized

and

finally,

when

I

said

you

know

you

can

get

out

quickly.

That

implies

the

last

point:

liquidity,

the

the

working

assumption,

which

is,

I

think,

roughly,

has

been

proven,

is

the

asset

can

be

sold

near

near

the

market

price

pretty

easily.

You

know,

at

least

in

a

reasonable

scale.

You

know

if

I

wanted

to

move

10

billion.

No,

but

you

know

when

we

want

to

move

several.

You

know

tens

of

millions

out

of

a

big

vault.

B

It

can

be

done

so

from

my

perspective,

I'm

gonna

I'm

claiming

and

I'd

love

to

hear

people's

views

to

the

contrary

that

this

is

really

what

makes

crypto

lending

you

know.

Very.

You

know

we

are

a

good,

safe

strategy

and

why

we're

making

money?

You

know.

I

think

these

are

very

important

principles,

and

I

I

imagine

if

you

asked

our

risk

folks

or

even

our

growth

folks,

do

you

want

to

start?

You

know

lessening

some

of

these

key

principles

around

lending

into

crypto.

I

think

they

would

be

concerned.

They'd

say

eric.

B

You

know

these

are

important.

This

is

how

we

make

sure

we

get

our

money

back,

because

there's

a

saying

in

lending

like

lending

money

is

easy

getting

paid

back

the

hard

part.

So

these

are

all

principles

to

make

sure

we

get

paid

back

all

right

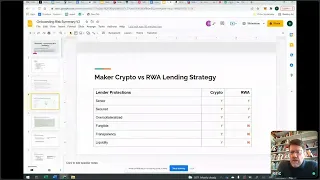

if

we

flip

to

the

next

slide.

Let's

talk

a

bit

about

the

crypto

which

we

just

discussed

versus

real

world

lending

strategy

in

the

real

world.

B

You

see

I've

lined

up

the

same

basic

items

on

the

left

and

then,

where

do

they

overlap

and

where

they

don't

real

world

is

senior

we

want

to

be.

You

know

the

first

lender

to

get

paid

back,

it's

typically

secured.

You

know

we

want

to

take

collateral

it's

over

collateralized.

You

know

we

want

more

collateral

than

what

the

loan

is.

So

if

there's

some

losses,

you

know

someone

else

eats

those

before

we

ever

get

hurt.

B

B

So

you

know

everything

is

a

bit

of

a

snowflake

next

transparency

around

pricing.

Typically,

you

know

most

loans

aren't

actively

sold.

You

know

at

least

a

consumer

loans.

You

know

five

thousand

dollar

credit

card

or

something

or

even

small

business

loans.

Maybe

fifty

hundred

100

000,

you

could

get

a

bid

for

them,

but

there's

not

really

an

active,

clear

market.

You

know

to

get

it

priced.

You

know.

Typically,

that's

why

you

get

these

financing

structures.

B

If

you

have,

you

know

100

million

dollars

of

small

business

loans,

you

put

them

all

together

in

a

pool,

and

you

know

then

you

issue

bonds

against

them,

so,

instead

of

selling

them

one

by

one

you're,

creating

this

more

complicated

structure,

we'll

talk

more

about,

you

know

how

we

need

to

create

that

structure.

So

the

market,

you

know

likes

it.

But

again

you

don't

really

have

active

pricing

in

near

the

same

way.

That's

a

big

difference

and

then

related

to

that

is

liquidity.

B

You

know,

if

it's

not

priced

and

not

necessarily

well

understood,

it's

not

easy

to

sell.

You

know

if

you

have

your

400

auto

loans

and

you're

like

all

right.

I'm

done

with

this.

I

want

out

your

eventually

go,

find

a

bid,

but

you

know

it

could

take

weeks

or

months.

You

know,

and

maybe

it's

90

cents

on

the

dollar.

You

know

there's

no

idea

that

boom

you're

out

the

door

and

gone

so

these

are

all

you

know

very

important

principles.

B

Let's

keep

going

here

all

right.

So

then

what

does

rwa

do

given

that

we

don't

have

the

fungibility

the

transparency

on

pricing

or

liquidity

to

sell

kind

of

at

will

that

crypto

does

here,

here's

you

know

from

my

perspective

and

actually

my

team

roughly.

What

do

we

layer

on

as

risk

bit

against,

given

that

we

don't

have

these

other

key

things

that

the

crypto

folks

who

are

making

loans?

Do

we

want

quality

cash

flowing

assets?

B

You

know.

So

if

you

have

a

pool

of

credit

cards,

you

know

you

have

a

pretty

good

sense

of

how

good

the

borrowers

are.

You

know

and

how

much

money

you

should

get

paid

back.

You

know

you

don't

want

assets

where

you

don't

understand

the

performance.

You

know

that's

probably

like

the

worst

thing,

because

if

you

step

back

a

bit

a

lot

of

what

we're

doing

in

rwa

is

we're

not

lending

against

a

price.

You

know

market

observable

for

the

crypto

collateral

and

we

know

we

get

out

at

the

market

price.

B

What

we're

basically

saying

is

look

we're

putting

a

pool

of

cash

flowing

assets

together

and

the

principal

and

interest

generated

by

them

over

time

is

more

than

enough

to

safely

pay

off

our

loan.

So

if

it's

a

two-year

loan,

you

know

we'd

want

to

have

you

know

a

comfortable

margin

from

this

pool

of

credit

cards.

You

know

that

even

if

you

know

there's

some

economic

distress

that

we're

still

going

to

get

paid

off,

you

know

timely,

you

know

so

that's

a

big

deal

and

then

it's

not

just

quality

cash

flowing.

B

You

know,

in

terms

of

like

the

deal

structure.

You

know

you

typically

want

a

diversified

pool

with

stable.

You

know

so

in

terms

of

diversified.

You

wouldn't

want

everyone.

You

know

to

necessarily

live

in

california

in

the

same

zip

code.

You

know

it's

going

to

depend

by

deal,

but

you're

typically

you'll.

Think

about

a

few

key

risks

then

diversify

across

it,

be

it

geography

or

something

like

that.

So

I

think

I

I

wrote

this

same

thing

twice,

but

so

we

want

a

diversified

pool

which

you,

you

know

you

don't

have

in

crypto.

B

We

want

a

pool

that

generates

stable,

predictable

cash

flows.

I'm

sorry,

we

don't

have

that

in

crypto.

I've

been

updating.

This

apologies,

that's

it

say.

No,

you

know

the

asset

pool

generating

stable,

predictable

cash

flows

is

not

is

no

in

crypto.

You

know

there

are

no

cash

flows

unless

you

sell

it

all

right.

So

that's

a

big

deal,

as

I

said

we

want

to

be

able

to

have

our

pool

of

assets

generate

enough

cash

flow

to

pay

our

loan

off

safely.

Over

time.

B

Also,

you

know

there's

in

the

deal

structure,

you're

going

to

have

credit

enhancement

which,

which

is

in

some

ways

it's

very

similar,

same

thing

as

over

collateralization,

but

yeah

there's

other

some.

You

know

kind

of

more

fancy,

ways

to

slice

and

dice

risk.

You

know

we'll

come

back

to

it.

You

know,

but

there's

a

lot

of

different

ways

to

try

to

mitigate

risk

using

structural

things

and

then,

finally,

again

I'll

say

this

is

within

deal

structure.

You

want

to

align

the

borrower

as

best

you

can

with

maker

the

lender.

You

know.

B

B

You

know

that

the

borrower

knows

a

lot

more

about

his

business

and

has

a

lot

of

decisions

to

make

that

you

can't

tell

him

what

to

do

so

as

much

as

you

can.

You

want

to

create

a

scenario

where

he's

aligned

to

make

decisions

that

are

in

your

interest

and

we'll

talk

about

things.

But

alignment

is

a

big

one.

You

know

there's

a

classic

joke

in

like

chicago.

You

know

where

chicago

has

the

trading

pits,

they

call

it

an

o'hare

trade

where

the

the

joke

is

look

go

to

like

the

board

of

trade.

B

Take

the

biggest

naked

like

option

position.

You

can.

You

know

on

the

most

volatile

commodity,

like

oil

or

crypto.

If

they

would

let

you

if

you

could

put

like

10

000

down

and

you'll

they'll,

give

you

100

to

1

leverage.

So

you

take

a

10

million

position.

You

take

the

biggest

position

you

can.

Then

you

drive

to

the

airport.

O'hare

is

the

international

airport.

You

know

you

call

and

see.

If

the

position

is,

if

it's

moved

big

time

in

your

favor

you're

rich,

you

come

back,

you

retire.

B

B

B

B

We

have

a

preference

for

investment

grade,

it

doesn't

have

to

be,

but

what

does

it

mean?

Historically

speaking,

you

know

you

look

at

the

data,

it

means

the

chance

of

a

debt

instrument

or

a

loan.

You

know

defaults,

you

know

comfortably

under

one

percent

a

year.

You

know

there's

specific

grades

within

that,

but

just

think

something

needs

to

default

less

than

one

percent

a

year.

You

know

the

other

way.

You'll

see

like

rating

agencies

say

that

is

it's

highly

likely

to

repay

the

loan

as

contractually

specified

I.e.

B

It

makes

all

of

its

payments

and

doesn't

default.

You

know

the

rating

agencies

and

credit

investors.

You

know

all

kind

of

use

this

similar

view

of

things.

They

might

have

little

differences,

you

know,

but

they

all

tend

to

think

about.

You

know

what

is

investment

grade

and

and

kind

of

have

an

idea

of

what

an

investment

grade

deal

looks

like

across

a

number

of

key

dimensions.

You

know

people

aren't

perfectly

agree,

but

it

is

a

rough

language.

You

know

that

will

be.

B

You

know

talked

about

and

argued

about

all

right,

so

that's

roughly

investment

grade

risk

just

think.

It's

very

likely

to

get

paid

back.

You

know

it

probably

defaults

less

than

one

percent

a

year

in

terms

of

the

rwa

risk

assessment.

You

know,

how

do

we

do

this?

Well,

so

we

look

at

an

asset

manager

or

a

borrower.

Go

across

some

first,

some

key

operating

areas.

What

operating

areas

are

most

important?

B

How

do

they

source

the

collateral

or

the

assets?

You

know

if

it's

going

to

be

unsecured

personal

loans

like

sofi,

you

know:

where

do

they

find

them

all

right?

You

really

want

to

understand

how

they're

getting

them,

and

is

it

consistent

because

at

the

end

of

the

day

we're

going

to

keep

coming

back

to?

We

want

stable

cash

flows

from

the

pool

of

these

loans,

so

you

want

to

have

a

stable

process.

You

don't

want

them

to

source

everything

one

month

from

one

channel

and

then

the

next

month

they

go

somewhere.

B

That's

completely

different

and

source

it

all

there.

So

the

performance

you

know

between

the

two

pools

is

very

different.

You

don't

like

that.

How

do

they

underwrite

it?

You

know

because

they're

ultimately

going

to

be

saying

yes

or

no.

You

know

I

I

want

to

extend

a

loan

or

I

don't

that's

a

big

deal.

So

how

do

they

understand

and

manage

their

risk?

B

Then?

Next,

how

do

they

manage

and

service

the

collateral?

You

know

once

they've

invested

in

something

you

know:

how

do

they

manage

the

ongoing

loan

and

if

there's

trouble,

you

know

what

do

they

do

and

then

also

we

want

to

look

at

you

know

at

their

investment

platform.

You

know

what

how

what

size

of

business

can

it

comfortably

service

and

and

if

they

you

know,

their

loan

is

three

times

bigger

than

what

they're

currently

doing.

How

are

they

going

to

get

there?

B

You

know,

because

at

the

end

of

the

day

is

a

lender,

you're

you're

only

going

to

add

best

cases,

you

get

your

principal

and

your

interest

back.

You

know

if

their

business

gets

10

times

bigger.

The

equity

guys

have

made

a

home

run.

You

know

you,

maybe

you've

got

a

bigger

loan,

but

you

you

get

nowhere

near

the

same

upside

as

the

equity

guy.

B

So

it's

something

to

keep

in

mind

and

then

also

a

big

deal

here

is,

as

we

look

at

you

know

the

collateral,

the

underwriting,

the

managing

and

servicing

you

you

like

to

look

at

their

historical

performance

with

the

same

or

some

similar

collateral.

You

know

what

is

the

best

predictor

of

their

future

returns.

It's

typically

going

to

be

based

on

what

have

they

done

for

the

last

number

of

years.

B

You

know

it's

almost

like,

like

in

sports.

You

know

when

someone

has

shown

an

ability

to

do

something

for

several

years.

Usually

that's

a

pretty

good

indicator

of

how

it'll

go

in

the

future

and

then

in

terms

of

the

principles

that

this

is

really

looking

at.

You

know,

as

we

went

through

the

key

rwa

principles,

you

know

on

the

right

again:

it's

quality

cash

flowing

assets,

that's

what

we

want

them

to

be

originating.

B

We

want

a

nice,

stable

pool

with

predictable

cash

flows,

and

then

we

also

want

them

to

be

aligned

with

maker,

we'll

come

back

more

on

alignment,

but

they

have

lots

of

little

decisions

around

sourcing

underwriting

and

so

forth,

and

we

can't

micromanage

those

decisions

as

a

lender.

Even

as

a

trad

deploy

lender,

you

don't

want

to,

but

particularly

you

know,

even

more

so

is

a

decentralized

lender,

so

we

need

to

construct

a

structure

that

makes

them

want

to

do

things.

That's

in

our

interest,

all

right

risk

assessment.

B

So

then

we

look

at

them

also

in

a

number

of

non-operational

areas.

You

know

we

just

talked

about

the

operations,

so

we

also

look

at

management

and

ownership.

You

know

management,

you

know

a

big

one.

Is

you

know,

what's

their

experience

and

track

record

in

this

area,

you

know

you

like

to

work

with

guys

who've

done

this

before

and

done

it

well

and

and

then

also

teams

that

have

worked

together

before

you

know,

there's

always

some

risk

in

putting

a

new

team

together.

That's

never

worked.

B

You

know

together

before

because

they

might

just

not

get

along.

You

want

to

know

the

financial

strength

of

their

business.

Do

they

have

enough

capital

so

that

they

can?

You

know,

focus

on

originating

and

servicing

good

collateral

for

you.

Are

they

going

to

be

running

out

to

have

to

raise

new

equity

in

six

months

and

might

take

the

eye

off

the

ball?

You

know

and

not

make

good

investment

decisions

for

you

also.

You

know,

as

I

mentioned,

what's

their

alignment

with

you,

it's

a

big

deal

and

are

there

any

potential?

B

You

know

conflicts

of

interest.

You

know

why

might

management

or

ownership

not

really

be

thinking

in

your

best

interest?

They

could

have

other

goals.

You

know

that

need

at

least

be

disclosed

and

understood,

and

again

on

these

non-operational

things

again

we're

trying

to

make

sure

that

they're

focused

on

generating

quality

cash

flowing

assets.

You

know

stable,

predictable

cash

flows

and

they're

aligned

reasonably

with

the

lender

being

maker

here,

okay

and

then

there's

so

essentially,

there's

three

sets

here

of

the

risk

assessment

I

did

operational.

B

Then

I

did

kind

of

non-operational

things

just

more

looking

at

their

business

and

now

we

also

look

at

the

financial

structure

and

the

legal

structure

of

the

specific

deal.

You

know

this

is

where

you

know

everything

comes

together,

they're

making

a

proposal

and

you

look

at

how

it

all

works

together.

You

know,

and

typically

when

you're

looking

at

this

we're

going

to

want

to

see

that

is

it

creating

a

diversified

asset

pool

with

stable,

predictable

cash

flows.

B

Is

there

good

credit

enhancement

and

other

risk

mitigants,

and

is

it

aligning

the

borrower

with

maker?

You

know

at

least

to

a

reasonable

degree.

You

know

these

are

key

key

points

and

I

hope

I

sound

repetitive.

That's

my

intent.

You

know

lending

good

lending

practices,

it's

not

rocket

science.

You

know,

there's

just

a

number

of

key

things

that,

like

around

alignment

and

diversification,

you

just

you,

you

consistently

want

it

done.

Well,

you

know.

B

Through

the

centuries

we've

seen

lots

of

people

kind

of

skip

on

these

principles

and

it

generally

comes

back

to

haunt

you

all

right.

Let's

talk

a

bit

about

how

do

you

make

an

investment

grade

loan

here

from

a

non-investment

grade

pool?

So

the

idea

is,

let's

just

give

an

example.

So

there's

a

sponsor

or

an

arranger

who

wants

to

buy

a

pool

of

loans,

say

there's

10

loans.

B

Each

one

is

10

of

the

pool.

Let's

make

this

real

simple

and

then

each

loan

has

a

5

chance

of

defaulting.

So

I

would

I

I

want

to

note

that

to

be

investment

grade,

you

know

you,

you

want

to

have

less

than

a

1

chance

of

defaulting,

so

each

individual

loan

is

clearly

not

investment

grade,

but

is

there

a

way

to

put

this

sucker

together

in

a

structure

that

we

can

make

part

of

it

investment

grade?

That's

what

a

lot

of

structured

finance

is

about.

B

So,

let's

take

the

first

one,

let's

say:

make

your

lens

100

to

the

sponsor

to

buy

the

loan

pool.

So

the

sponsor

you

know,

tells

us

he's

gonna,

do

a

good

job,

but

he's

not

putting

his

own

money.

In

I

mean

he's

got

his

own

business

but

we're

all

of

the

all

of

the

money.

So

if

you

come

and

look

you

know

total

collateral,

let's

just

call

it

100

these

10

loans

and

then

the

maker

loan

down

here

below

is

a

hundred

percent

and

the

sponsor

puts

in

no

equity

right.

B

So

it's

essentially

it's

all

our

capital

and

then

can

we

trans

or

what

will

the

the

risk

of

this

group

of

10

equal

size

loans

be

to

us?

You

know,

as

the

lander

will,

the

annual

default

rate

be

under

one

percent.

You

know

I

think

people

are

probably

going

to

guess.

No,

but

let's,

let's

take

a

look,

so

here's

some

basic

statistics

on

this

group

of

10

loans,

equal

sized

five

percent

probability

of

defaulting

each.

B

What's

the

chance,

no

deals

default,

none

of

the

loans

default.

It's

basically

you

see

here

60,

so

60

of

the

time

the

loan

performs.

You

overhear,

why

means

it

alone

performs

and

it

doesn't

default

and

there's

equity

sponsor,

essentially

they've

put

nothing

in,

but

you

know

in

theory,

should

they

be

covering

some

loss,

so

there's

zero

default

and

everything

goes

good

in

the

first

scenario,

right

with

no

losses,

that's

60

of

the

time.

B

What

about?

If

there's

one

of

the

10.

you

know

this

is

just

your

basic

probabilities

here.

If

one

defaults,

that

is

going

to

happen

almost

32

percent

of

the

time

so

and

if

that

happens,

we're

we

have

no

first

loss

capital

under

us,

so

the

sponsor

equity.

In

a

sense

there

is

no

equity,

but

it's

underwater

and

does

the

loan

perform?

No,

it

doesn't

perform

right.

So

one

of

the

10

is

defaulted

and

we

absorb

that

loss.

That's

not

great!

For

maker.

B

B

No

more

than

zero

defaults

is

60.,

then,

what's

the

chance

of

no

more

than

one

default.

That's

just

the

sum

of

zero

defaults,

plus

one

default,

so

I

sum

fifty

nine,

nine

and

thirty

one

five.

So

ninety

one

point

four

percent

of

the

time

we

get

no

more

than

one

default,

so

that's

still

not

investment

grade.

You

know

we

need

to

be

like

99

percent

no

defaults.

So

if

we

come

down

to

two

defaults,

then

we

sum

you

know

the

599

plus

the

31.5,

plus

the

7.5.

B

We

get

98.8

so

we're

almost

at

99..

So

in

essence

you

know

to

be

investment

grade.

This

is

telling

us

you'd

have

to

be

able

to

absorb

two

defaults

or

less

you

know,

and

so

it's

kind

of

the

ideas

I'm

trying

to

plan

in

people's

heads

here

is

you

somehow

need

to

put

in

enough

capital?

First

lost

capital?

That's

not

the

maker

loan

that

will

absorb

this

first

20

default.

You

know

to

create

something

quasi

investment

grade.

You

need

to

do

a

little

better

than

that.

The

sponsor

puts

no

money

in

so

then.

B

B

So

again,

it's

100

of

the

assets

same

asset

side

of

the

balance

sheet

maker

now

only

puts

an

80

and

the

sponsor

puts

in

20

20.

This

is

a

big

difference

and

then

it's

not

put

in

in

in

a

pro

rata,

we

don't

share

losses

and

and

income

equally

with

the

sponsor

equity,

the

sponsor

absorbs

the

first

losses

and

maker

will

only

take

a

loss

after

the

the

sponsor's

capital

is

all

gone.

B

This

is

essentially

what

senior

means

with

a

senior

loan

we're

senior

to

their

capital,

so

they

eat

the

losses.

This

is

a

typical

lending,

a

lending

approach,

and

then

so

the

question

becomes,

you

know,

is

this

investment

in

grade

I.e?

You

know,

is

not

this

whole

thing,

but

is

the

maker

loan

investment

grade?

Does

it

have

less

than

a

one

percent

probability

of

default?

Let's

take

a

look.

B

B

B

If

there's

one

loss

that

we're

assuming

you

know,

there's

no

recovery,

so

the

10

percent

of

the

capital

disappears,

but

the

sponsor

absorbs

the

loss

right.

So

then

their

sponsor

equity,

after

the

loss

is

10

percent.

It

still

performs.

Why

does

it

perform

because

the

sponsor

is

taking

the

first

loss,

we're

not

taking

it?

Even

if

there's

two

losses

that

means

20

of

the

assets

disappear

without

us

getting

paid

back.

B

B

Thirty

percent

of

the

pool

is

gone,

the

sponsor

only

put

in

twenty

percent.

So

now

the

sponsor

is

gone,

but

that

additional

10

percent

comes

to

us

and

we

take

a

loss.

It

doesn't

perform

right.

I

I

hope

this

is

clear.

This

is

kind

of

the

break

right

here,

but

you

can

see

how

much

more

resilient

this

is.

How

often

do

you

get?

Three

losses

are

three

three

defaults

or

more

in

the

pool.

Essentially

it's

a

little.

You

know

a

little

over

one

percent.

B

It's

like

one

point,

two

percent

of

the

time,

so

it's

not

quite

investment

grade,

but

it's

very

close.

So

if

we

flip

back,

we

can

see

when

there's

no

capital

under

us

zero

defaults

is

the

only

time

our

senior

our

senior

loan

performs

when

there's

20

percent

first

loss

under

us.

You

know

we

make

it

all

the

way

up

to

two

defaults,

which

is

a

big

deal

right.

You

know

this

is

one

of

the

key

things

in

structured

finance.

B

How

would

we

think

about

montalis?

And

I

don't

mean

to

pick

on

them,

but

it

is

a

well-known

one

in

in

the

in

the

community

and

it's

you

know,

there's

I

think,

there's

a

vote

coming

and

we

believe

you

know

in

terms

of

radical,

defy

transparency.

We

want

to

be

transparent,

fully

transparent

on

how

we

look

at

things

you

know

and

have

a

discussion.

You

know

maybe

we're

missing

something.

So

what

is

montales?

B

They

aim

to

do

wholesale

wholesale

lending

in

the

uk

to

small

medium

enterprises

and

with

a

green

focus,

which

we

like

it's

good

to

be

a

green

focus.

Initially

they

asked

for

400

million.

They

come

back

since

and

said

now,

they're

asking

for

40

million,

you

know

so

it's

it's

not

a

huge

amount,

but

it's

real

money.

40

million

is

over

half

of

our

capital

surplus,

their

their

request.

B

Their

proposal

is

to

pay

a

two

percent

stability

fee

to

us

and

then

also

this

look

we'll

see

this

later,

but

they

would

get

a

one

percent

management

fee

to

run

their

business

and

they

get

20

of

the

profits.

You

know

the

one

in

20

is,

you

know

ballpark

and

how

these

you

know

how

some

of

these

deals

can

be

done.

So

when

rwa

rwf

same

thing

thinks

about

this,

how

do

we

assess

monica's

proposal?

What

are

the

glasses

we

wear?

Hopefully

this

is

sounding.

This

is

gonna

sound

repetitive.

B

B

So

then

I

think

you

want

to

think

about

why

you're

doing

it-

and

it

very

well

could

be

a

good

reason

to

do

it

like

the

green

focus

and

then

the

next

question

is

because

is

this

transaction

a

good

standard

for

other

transactions?

You

know

once

we

approve,

at

least

from

the

risk

guys

that

we

don't

approve

once

we

bless

it

and

say

we

like

it,

we

know

we're

going

to

get

lots

of

other

folks

coming

and

wanting

you

know

same

basic

standard.

B

You

know

so

once

you

set

a

standard

as

a

you

know,

as

a

lender,

you'll

have

a

lot

of

folks

expecting

to

come

with

a

very

similar

standard.

So

you

know

you

you

want

to

be

waving

in

you

know

all

that

kind

of

business

and

then

finally,

and

I'll

talk

about

this

more

towards

the

end.

Would

it

be

viewed

as

arm's

length?

You

know

we'll

talk

about

it,

but

arm's

length

is

basically.

B

Is

it

viewed

as

kind

of

like

a

a

reasonable

market

transaction

where

both

sides,

the

lender

and

the

borrower,

are

acting

independently

in

their

own

interest?

You

know

this

is

something

I

think

we

want

to

be

careful

with,

at

least

from

our

perspective.

You

know.

Risk

in

the

rwa

group

is,

you

know

in

traditional

finance,

you've

seen

a

lot

of

times.

People

get

in

trouble

when,

when

a

company's,

you

know

making

a

loan

to

some

subsidiary,

and

it's

not

really

doing

it

at

market

terms.

B

You

know

and

there's

there

can

be

a

question

of.

Is

there

some

insider

dealing

and

you

know

who's

kind

of

getting

the

better

deal

and

why

I

mean

I

think

the

optics.

Do

this

really

matter

and

we'll

come

back

to

it,

but

it's

certainly

it's

something

to

keep

in

mind

all

right.

Oh

sorry,

and

then

yeah,

I

I've

kind

of.

I

I've

messed

up

my

slide

order,

but

I

I

do

want

to

make

just

to

review

how

we're

gonna

look

at

monitalis,

so

we

talked

about

structuring

investment

grade

loan.

B

These

are

all

important

and

I

just

want

to

note

and

kind

of

a

shout

out

to

christian

and

the

legal

side.

We

don't

just

say:

hey

here's,

a

quick

term

sheet.

You

know

all

of

this

is

done.

Making

sure

all

of

these

steps

are

done,

takes

a

lot

of

legal

structure

and

analysis.

It's

it's.

You

know,

unlike

crypto,

where

you

can

just

take

their

crypto

collateral

in

a

vault

and

then

liquidate.

If

you

need

this,

all

you

know

has

to

have

these

agreements

and

the

collateral.

B

You

know

we

need

to

have

legal

agreements

that

we

can

actually

take

the

collateral

if

needed

and

enforce

our

rights

and

remedies.

It's

it's

a

pain

in

the

neck,

but

you

to

be

a

good

lender.

You

really

need

to

have

all

these

rights

and

remedies,

and

if

you

don't

it,

it's

troubling

and

that's

a

good

way

to

lose

money.

B

Okay.

So

when

we

think

about

monetalis

what

are

the

key

risks?

Let's

first

structure,

you

know

how

we're

going

to

think

about

this

one.

The

facility

risk

the

money.

You

know

we

call

a

loan

a

facility.

If

monetaris

and

its

investments

underperform,

you

know

we

could

lose

capital,

that's

clearly

a

obvious

risk.

I

think,

there's

a

more

subtle

one,

that's

ultimately

probably

more

important

longer

term

for

a

maker

when

we

think

about

how

we're

lending

is.

B

What's

the

stability

risk

to

the

die,

you

know

at

the

end

of

the

day,

the

market,

you

know

folks

holding

die,

you

know,

look

at

it

and

say

this

is

convertible

one

for

one

into

dollars,

but

that's

only

true

if

there's

really

good

collateral

backing

it,

you

know

right

now

we

have

a

lot

of

usdc,

that's

good

stuff.

What,

if

we

all

put

it

into

say,

bitcoin

could

be

worth

a

whole

lot

more

in

a

few

months

could

be

worth

a

whole

lot

less.

B

You

know

that

would

put

it

stability

risk,

so

the

market

really

wants

to

see

that

we've

got

solid

collateral

with

a

good

structure

and

and

a

good

manager.

Your

good

managers

who

know

what

they're

doing

and

you

know

if

you,

if

you

ever

pay

attention

to

kind

of

the

history

of

bank,

runs

you'll,

see

banks

getting

into

trouble

when

people

don't

think

their

assets

are

good

and

then

people

trying

to

get

their

money

out

quickly,

because

if

there's

a

perception,

there's

not

enough

good

collateral

to

back.

You

know

your

deposits.

B

You

want

to

be

the

first

one

to

get

paid

back,

because

maybe

the

last

guy

isn't

going

to

get

paid

back

at

all,

and

so

there's

clearly

a

parallel.

You

know

in

kind

of

our

world

where

someone

thinks

to

die,

isn't

worth

100

on

average.

You

want

to

be

the

first

guys

to

get

100

cents

back

and

then

maybe

the

last

guys

get

much

less

and

we

do

not

want.

We

do

not

want

to

create

that

perception

or

risk,

and

a

lot

of

it

has

to

do

with

perception

all

right.

B

So

we

think

about

the

facility

risk

of

monetalis

were

looking

really

at

three

areas.

One

is

the

manager

themselves.

Two

is

the

asset.

You

know

they're,

making

loans

against

a

green,

small

business

collateral

and

three

it's

the

structure.

It's

the

deal

itself,

you

know

and

and

we'll

go

through

these

three

and

then

typically,

if

there's

a

major

deficiency

in

any

you

know

kind

of

these

areas,

it's

usually

not

investment

grade

investment

grade

has

a

numerical

element

but

there's

also

kind

of

a

qualitative

element

where

you'd

say:

okay,

let's

look

at

this

manager.

B

This

manager,

you

know,

has

never

managed

this

kind

of

asset.

Before

you

know

it's

hard

to

put

an

investment

grade

number

on

it

because

you'd

say

well,

what's

you

know?

What's

the

chance,

the

collateral

is

going

to

perform

really

well,

and

you

say

well,

what's

his

track

record

and

they

say

well,

he

doesn't

have

a

track

record.

You

know

in

this

or

a

similar

type

of

collateral,

so

it

gets

hard

to

make.

You

know

a

very

confident

statement.

You

know

about

the

consistency

of

the

cash

flows,

to

pay

you

back,

okay,

but

yeah.

B

At

the

end

of

the

day,

we're

going

to

think

about

manager,

risk

asset

risk

and

structural

risk.

So

let's

go

through

them,

one

by

one,

all

right

manager.

How

do

we

look

at

monitalis

in

their

manager?

One?

I

think

you

know

alessio

and

alan

are

very

talented

guys.

You

know

alan

has

a

lot

of

private

equity

experience.

B

This

is

all

good,

very,

very

respectable,

but

neither

one

has

ever

really

been

the

guy

running,

a

private

credit

fund

asset

finance

manager,

so

they

don't

really

have

a

track

record

and

you

know

you

can't

say

wow

over

the

last

four

years.

You

know

here's

what

they

did

across

their

deals,

so

it

gets

very

hard

to

predict

their

performance

given

they've.

Never

really

done

this

specific

thing

before

that's

definitely

a

concern.

B

Next

is

they're

a

startup

asset

manager.

It's

a

business

model

that

you

think

probably