►

From YouTube: Focus On #10 | MIP6 vs. TradFi

Description

Forum Post: https://forum.makerdao.com/t/focus-on-10-mip6-vs-tradfi/14628

Focus On hosted Eric Rapp @Eumenes from @Real-World-Finance and Christian Petersen @christiancdpetersen from the incubating Legal & Transaction Services Core Unit to discuss the MIP6 process vs. TradFi deal assessments.

The team first discussed the MIP6 process by reviewing the framework for fact-based assessments and the role of RWF core unit(s). The team then explored comparable aspects of TradFi Structured Finance Transactions and how the roles of borrowers & lenders translate to MakerDAO’s MIP6 framework.

A

We

try

to

address

that

diversity

and

that

diversity

is

great.

It

just

makes

things

a

bit

more

complicated.

We

try

to

address

some

of

the

complication

that

arose

from

that

diversity

by

publishing

in

mid-january,

a

methodology

for

structured

finance,

and

that

was

to

identify

some

general

principles

that

six

applicants

could

try

to

follow

when

submitting

an

application

again,

trying

to

homogenize

a

little

bit.

A

The

process

which

goes

to

my

next

point,

which

is

finance

agreements

themselves,

are

not

homogenous,

and

what

I

mean

is

we

don't

prepare

the

initial

terms

and

conditions,

and

that

means

that

the

terms

and

conditions

are

going

to

vary

between

six

applications.

Unfortunately,

finance

agreements,

even

in

the

real

world,

let

alone

in

t5,

are

not

like.

A

Some

of

the

applications

are

many

of

not

that

we're

getting

better

many

knit

six

and

self-contained

mip

applications

actually

do

not

provide

a

fully

defined

transaction

structure,

although

none

of

them

actually

provide

a

strath

transaction

documents

or

even

a

term

sheet

to

facilitate

a

comprehensive

and

mean

meaningful

review

and

you'll

see

why

this

is

important

in

the

next

few

slides.

So

next

slide.

A

B

A

By

the

way,

there's

hundreds

of

terms

in

a

transaction,

but

just

for

example,

you

have

term

one.

So

the

first

thing

we

do

is

determine

whether

that

term

is

quote

acceptable.

Okay,

what

does

acceptable

mean

acceptable

means

that

we

look

at

that

term

based

on

reasonable

market

standards.

So

if

it's

a

real

estate

deal,

we

kind

of

try

to

understand

what

the

real

estate

market

has

for

that

particular

standard.

A

A

A

A

Well,

what

if

term

one

is

better,

it's

actually

better.

So

it's

not

just

acceptable,

but

it

would

be

better

for

maker

if

the

term

is

modified

to

include

b.

So

it's

now

term,

one

plus

b,

is

that

okay,

you

know

is,

is

our

role

to

look

out

for

the

best

interests

of

maker

by

proposing

a

term

that

may

be

better

for

maker

than

just

term

or

term

one

plus

a

you

know

what,

if

the

term

isn't

acceptable

at

all,

you

know:

can

we

counter

propose?

A

A

So

what

is

reasonable?

What

is

market,

whose

market

standard

and

are

any

of

the

counter

proposals

in

examples?

Two

three

or

four,

where

we

are

quote

countering,

is

that

a

private

entanglement,

the

term

private

entanglement

seems

to

be

thrown

a

lot

around

a

lot

of

the

community.

Are

we

engaged

in

private

entanglement

because

we

are

proposing

a

term

that

may

be

more

beneficial

to

maker?

A

B

A

Of

the

story,

we

move

on

to

the

next

next

point

and

then

give

a

response

to

the

community

on

a

point

by

point

basis

that

this

term

is

not

acceptable

or

you

know.

Are

we

at

that

point

exceeding

our

role

as

assassin

you

know

in

in

the

real

world?

You

would

negotiate,

you

would

say:

okay.

Well,

I

get

term

one

but

yeah

term,

one

a

is

better

or

term

one

b

is

better

for

maker.

A

A

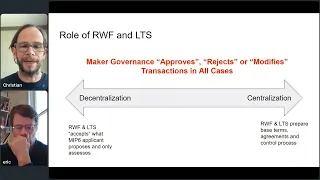

And-

and

it

really

all

comes

down

to

a

little

bit

of

a

debate

regarding

decentralization

and

centralization,

and

the

role

of

the

real

world

finance

and

transaction

and

services

core

units

in

this

process.

Now,

as

a

lawyer

to

me,

everything

is

on

the

spectrum

and

I

can

find

a

point

all

along

that

spectrum.

A

But

first

and

foremost,

I

want

to

make

sure

everybody

understands.

We

are

very,

very

clear

abundantly

clear

that

we

do

not

approve

reject,

or

you

know

that

basically

maker

governance

approves

rejects

or

modifies

transactions

in

all

cases,

all

we

can

do

is

in

some

sense,

try

to

get

the

best

deal

for

maker

and

make

a

recommendation.

A

A

There's

an

extremist

centralization

where

we

prepare

the

underlying

agreements,

we

control

the

entire

process

and

then,

frankly,

in

the

real

world.

Most

lenders

are

on

this

side

of

central

organization.

Now,

even

even

as

much

as

whose

council

prepares

the

documents,

typically

typically

lender's

counsel

will

prepare

the

documents.

That

means

we

would

in

theory,

if

we

were

the

lender,

control

the

entire

process.

You

know

we've

taken

the

you

that

we

that's

perhaps

too

much

centralization.

B

A

C

The

christian

can

I

give

an

example

on

that

christian's

point.

Let's

say

it's

a

term

that

really

matters

in

the

perspective

borrower

comes

and

they

want

100

advance

rate.

You

know

I

wanted

to

you

know

so

you

know

essentially

when

they

make

a

loan

to

someone

else.

We

give

them.

You

know

100

cents

on

the

dollar,

so

they

have

really

no

equity,

no

skin

in

the

game,

and

you

know

perhaps

the

real

in

the

real

world

market.

C

Maybe

they

ought

to

begin

80

advance

rate

typically

and

they

come

to

us

and

ask

maker

and

ask

for

100.

You

know

I

mean

it's

really

a

fundamental

question

of

how

is

maker

going

to

think

about

that

one.

It's

it's!

It's

way

off

market.

You

know

if

the

real

world's

saying

it's

80

and

they

want

20

more

advance

rate.

What

they're

really

saying

is

hey.

We

want

to

be

cheap

and

not

you

have

to

spend

the

equity

out

of

our

pockets.

You

know.

C

Normally

you

need

to

raise

equity,

you

know

to

help

build

your

business

and

you

know

give

the

lender

some

cushion

some.

You

know

first

loss

position

and

they're,

basically

telling

maker

hey.

We

don't

want

to

do

that.

You

know

we

want

to,

you,

know,

have

all

the

upside

and

you

get

all

the

downside,

and

so

how

do

you?

How

is

maker

supposed

to

you

know

make

a

decision

on

that

I

mean

to

some

of

us

who've

been

in

the

business

a

long

time.

C

I

mean

it's

kind

of

absurd,

you

know,

but

we

do

get

these

asks.

You

know,

and

it's

really

I

guess

we

want

to

ask

maker

as

a

community.

You

know

how

do

you

want

to

think

about

these

things

and

respond

to

them?

You

know

I

mean,

because

I

can

tell

you

yeah,

it

looks

stupid

or

it

looks

ridiculously

off-market,

but

you

know

it's

not

my

place

to

say

no,

I

mean

I'll

just

say:

hey

it's

ridiculously

off-market.

C

C

You

know

that

no

smart

lender

from

my

perspective

in

this

business

20

years

would

do

they'd,

laugh

at

you

and

say:

leave

okay

next

slide,

please

all

right

so

when

in

the

traditional

world,

let's

talk

about

how

they

do

a

structured

finance

transaction,

you

know

what's

the

process,

you

know

how

do

they

do

things?

What

do

they

look

for?

First?

You

know,

let's

think

about

what

are

the

lender

and

the

borrower

looking

for

what

are

their

priorities,

then

we're

going

to

talk,

you

know.

Typically,

you

know

the

borrower.

C

You

know

it's

going

to

be

seeking

financing.

You

know,

then

the

borrower

is

going

to

prepare

and

propose

some

type

of

offering

you

know

to

potential

lenders,

and

usually

you

don't

go

to

just

one

lender.

You

know

I'm

having

been

on

the

other

side

of

this.

You

know

we

probably

start

out

with

10

or

15

potential

lenders

and

you

funnel

it

down.

You

know

you

typically

want

to

go,

get

a

few

different

offers

and

have

some

idea

of

getting.

C

You

know

the

best

terms

out

there

you

know

so

in

a

sense,

I

get

a

little

worried

when

lenders

come

only

to

us,

you

know

and

we

seem

to

be

their

only

target

to

get

funds.

You

know

it

puts

us

in

a

weird

spot,

but,

assuming

like

the

borrower,

presents

something

that

that

makes

ballpark

sense.

You

know

they

will

engage

with

the

lender

the

potential

lender.

You

know,

I

call

this

an

initial

engagement

and

you

know

then

the

we'll

talk

about

these

steps.

More

then

they'll

go

on.

You

know

if

they

both

agree.

C

Roughly

on

here's

a

deal,

you

will

call

that

a

term

sheet.

You

know

it's

a

written

agreement

that

that

isn't

binding

but

in

a

sense

both

sides

you're

saying

here's,

the

rough

terms.

We

think

a

deal

can

be

done

at

and

let's

do

a

lot

more

work

and

make

sure

it

works

and

I'd

say,

probably

more

often

than

not.

The

term

sheets

actually

go

on

and

closes,

but

sometimes

particularly

you'll

find

lenders

may

back

out

because

they'll

find

what

they

were

told

by

the

borrower.

You

know

in

the

early

stages.

It

isn't

really

quite

true.

C

C

Then

let's

talk

a

bit

about.

You

know

the

kind

of

key

terms

and

there's

many

of

them

and

then

also,

let's

talk

about

trad

five

versus

the

defy

on

boarding

process.

You

know

just

to

step

back

and

think

of

some

of

these

points.

There's

definitely

some

there's.

Definitely

some

key

points

to

think

about.

So

next

slide,

please

all

right.

So

what

are

the

priorities?

C

Well,

as

a

lender,

you

know

you

want

quality

collateral

right,

that's

very

highly

repaid

likely

to

repay

the

loan.

You

know

you're,

not

in

the

business

of

losing

money,

and

if

your

typical

lender,

you

know

stuff

we're

looking

at,

is

probably

getting

two

to

four

percent

interest

rate

a

year.

You

you,

you

can

have

very

few

losses.

You

don't

even

break

even

just

think

about

that.

C

If

you

get

a

two

percent

annual

interest

rate

and

you

suffer

a

five

percent

loss

a

year

on

average

you're

giving

away

three

cents

out

of

your

pocket

a

year

right,

you

know

that

just

doesn't

work.

So,

if

you're,

if

you're

going

to

have

a

low

single

digit

interest

rate,

that's

telling

you

your

interest.

Rate's

gotta,

I

mean

your

risk

levels

got

to

be

low,

and

so

the

lender

wants

to

have

people

that

repay

them.

They

also

want

an

efficient,

transparent

and

consistent

review

process.

Why

do

you

want

this?

C

It's

not

just

you're

a

good

person,

though

I

think

this

is

fair.

You

want

to

attract

quality

borrowers.

You

know

good

borrowers

want

to

work

with.

You

know

good,

reasonable

lenders.

You

know

you

don't

expect

the

the

borrowers.

Don't

expect

the

lender

to

be

your

friend,

but

you

want

to

know

where

they're

coming

from

you

know

and

think,

like

it's

a

reasonable

process,

you

know

where

both

parties

are

engaging

in

good

faith

and

trying

to

get

to

a

good

result,

I.e

a

transaction

and

what

are

the

borrower

priorities?

C

Well,

of

course

you

know

they

want

a

good,

predictable

review

process.

They

want

to

engage

with

lenders.

You

know

that

they

think

they

have

a

good

chance

of

doing

business

with

the

borrower

wants

to

have

someone

that

once

they

agree

kind

of

on

key

terms

or

come

to

a

term

sheet

that

the

lender

has

a

reputation,

that's

earned

that

they,

actually

you

know

they

they

will

close

on

the

kind

of

term

sheet

they

they

close

at

most

of

their

term

sheets.

C

You

know

they

don't

walk

away

in

the

middle

of

transactions

unless

there's

a

really

good

reason,

yup

and

so,

and

when

you

think

about

once

the

term

sheets

agreed

to

that's

when

you

start

spending

a

lot

of

legal

bills,

actually

documenting

things,

and

typically

the

borrower

pays

this.

So

again,

they

only

want

to

start

working

on

legal

documents

with

lenders

that

are,

you

know,

have

a

good

reputation

and

it's

earned

for

following

through

once

they

say

they

like

a

transaction

next

slide.

Please.

C

So

how

does

it

start

well?

The

borrower,

for

some

reason

needs

financing

and

how

do

they

do

this

they're

going

to

prepare

a

financing

proposal

for

potential

lenders?

You

know

essentially,

like

a

memorandum

saying

you

know,

here's

who

we

are,

here's,

why

we

want

financing

here's,

what

it's

going

to

be

used

for

and

then

typically

they'll

make

it

kind

of

a

term

sheet

proposal.

You

know

maybe

a

five

to

ten

page

document

outlining

key

terms.

You

know

a

number

of

the

key

terms.

They

might

leave

the

specifics

blank.

C

You

know,

but

they're

just

trying

to

show

the

lender

roughly

what

they're,

looking

for?

Typically

a

borrower

may

invest,

engage

in

investment

bank

kind

of

think

of

this

as

a

structuring

agent

to

guide

them.

When

would

they

engage

in

investment

bank

because

you

know

investment

banks,

it's

not

cheap

you'll,

probably

charge

you

at

least

one

percent

of

the

transaction.

So

it's

a

hundred

million

dollars

to

go

charge

you

a

million

dollars.

Well,

if

it's

the

inexperienced

borrower

who's

not

used

to

this.

You

know

the

investment

bank

typically

will

be

an

expert.

C

You

know

in

this

asset

class,

and

so

not

only

do

they

know

the

asset

class,

but

they

know

a

whole

bunch

of

potential

lenders.

So

they're

going

to

you,

know

kind

of

take

you

out

and

introduce

you

to

maybe

15

20

lenders

that

they

think

are

relevant

to

what

you

want

to

do

and

they

also

help

you

put

together.

You

know

your

proposal,

two,

it's

a

very

complex,

complex

transaction.

C

You

know,

even

if

you

know,

you've

done

transactions

before,

if

you're,

adding

something

really

sophisticated.

Often

you

want

to

get

these

hired

experts.

They

just

know

how

to

do

these

things

really.

Well,

I

mean

that's

their

expertise,

they

live

on

it.

I

mean

it's

like

kid

with

christian

there's,

a

reason

like

one

of

the

lawyers

we've

used

is

sherman

sterling

he's

a

great

lawyer.

He

lives

in

a

5

million

house.

Why

did

you

live

in

a

5

million

dollar

house

because

he's

exceptionally

good

at

what

he

does

and

people

want

his

advice?

C

You

know-

and

I

I

don't

begrudge

him

his

money-

he's

really

good

and

finally,

if

you're

reaching,

if

you're,

not

just

looking

for

one

lender,

if

you're

looking,

maybe

more

securitization

where

you're

you're

gonna

have

dozens

of

more

public

bond

investors

buying

your

deal

or

investing

in

your

deal,

then

you

probably

are

gonna

want

an

investment

banker,

because

they're

gonna

know

the

the

investor

base

to

reach

out

to

you

know.

If

it's

public

bond

securitization,

they

could

be

reaching

out

to

100

investors,

you

know

and

they

have

a

whole

sales

distribution

arm.

C

You

know

that's

very

valuable.

You

know

most

companies

don't

have

their

own

bond

sales

distribution,

and

so

what

are

investment?

Bankers

good

at

I

pretty

said

said

this

thing,

so

let

me

just

kind

of

highlight

it:

they

they

know

asset

finance,

capital

markets.

This

is

what

they

do.

They

know

where

the

potential

lenders

are.

C

They

know

what

reasonable

terms

are

for

transactions.

You

know

when

you

think

about.

If

I'm

like

an

auto

lender,

you're

looking

to

go,

you'll

get

a

bank

line

against

my

portfolio

of

auto

loans.

I

might

not

know

roughly

what

the

terms

are.

The

investment

bankers

go

say:

look,

you

know

you

probably

will

get

75

to

80

leverage.

You

know

kind

of

outline

the

whole

range

of

what's

reasonable

and

help

guide

you

in

the

negotiations,

and

you

know

if

you

want

to

push

one

point

in

the

negotiations.

C

They'll

probably

say

okay,

but

maybe

you

ought

to

give

up

something

else.

If

you

really

want

that

one

point

so

they're

just

experts

in

kind

of

knowing

where

the

market

does

things

and

they're

very

good

at

kind

of

backdoor

channeling

with

lenders,

you

know

to

be

kind

of

a

middle

person

in

the

negotiations.

C

It

helps

keep

things

get

from

kind

of

too

tense

when

the

lenders

like

I

want

this

and

the

borrower's

like

is

no

it's

good

to

have

that

middle

guy

kind

of

keep.

You

know

things

calm

they're

also,

as

I

said,

very

good,

at

structuring

and

negotiating

deals,

and,

finally,

I

think

it's

underappreciated,

but

they're

very

good

at

managing

a

transition

from

beginning

to

end.

You

know

it's

not

easy

to

do.

You

know,

there's

lots

of

commercial

terms,

legal

terms.

C

All

these

different

things

have

to

be

done

and

part

of

what

they

do

is

just

manage

the

whole

process,

which

is

very

valuable,

next

slide,

please,

so

how

does

it

go?

Well?

The

borrower

starts

by

preparing

and

proposing

they

put

together

this

financing

proposal

to

potential

lenders.

What

is

it

going

to

cover?

You

know

their

origination

platform?

You

know

they

just

goes

like

what

do

they

need

the

money

for

you

know

who

are

they

owned

by

who's?

Who

are

their

management?

How

do

they

originate

assets?

You

know

loans,

how

do

they

underwrite

them?

C

What's

their

credit

process?

How

do

they

serve

them?

I'm

service

them.

You

know

you

monetize

monetize,

the

payments

they're

going

to

want

to

also

prepare

how's

their

assets

performed.

Historically,

you

know

when

lenders

look

at

borrowers,

what's

your

best

predictor

of

how

their

portfolio

of

assets

will

perform,

probably

how

they've

done

over

the

last

four

or

five

years

and

then

it'll

also

have

some.

You

know

commercial

terms

and

legal

structure

proposed.

C

C

So

if

there,

if

the

borrower

doesn't

know

much,

you

typically

would

expect

a

borrower

to

have

a

smart

legal

counsel

to

guide

them

on

legal

structure

and

then

some

kind

of

asset

finance

banker

who

can

guide

them

on

how

this

is

done.

You

know

it's

a

complex

series

of

things

to

be

done

and

if

the

borrower

really

doesn't

have

a

good

idea,

what

they're

doing

it's

very

very

time

consuming

and

difficult

to

close

a

transaction.

You

know

with

inexperienced

borrowers

without

the

right

counsel.

C

I

mean

a

number

of

lenders

will

probably

just

choose

not

to

engage

it's

just

too

difficult

next

slide.

Please

all

right:

the

initial

engagement,

the

borrower

approaches

the

lender.

You

know

with

their

proposal

the

lender

is

going

to

have

an

initial

discussion

review

with

the

borrower.

So

what

is

the

lender

going

to

do?

I

mean

I've

been

more

in

the

lending

seat

than

the

borrowing

seat,

but

so

and

since

the

lender

wants

to

say,

hey,

does

this

asset

and

proposal

meet

my

risk

appetite?

C

If

I

only

want

short

duration

assets

or

only

investment

grade

assets,

you

know,

does

it

check

those

boxes?

At

the

end

of

the

day,

when

you're

a

lender,

you're

really

looking

to

to

throw

everything

out

really

quickly,

that

doesn't

mean

your

key

hurdles.

You

don't

want

to

spend

any

more

time

than

you

have

to

on

stuff.

That's

not

going

to

make

it

so

does

it

meet

your

risk

appetite

and

then

also

you're,

going

to

look

at

what

what

the

proposal

terms

are.

C

You

know

if

it

meets

your

risk

appetite

is:

is

the

borrower

asking

for

kind

of

ballpark

terms

that

seem

reasonable

to

you?

You

know

if

you

like,

auto

loans,

but

they

want

a

95

ltv

and

you

know

85

percent

about

as

high

as

the

market

goes.

It's

probably

not

worth

spending

a

lot

of

time

on

them

and

once

you

tell

them

that

and

if

they

don't

change

your

view,

you

probably

want

to

move

on,

and

then

the

lenders

go.

Assuming

the

the

lender

says.

C

This

is

in

my

risk

appetite

and

the

borrower

is

asking

terms

that

seem

reasonable

enough.

Ballpark

that

they're

going

to

do

the

lender

will

do

some

initial

diligence

on

the

borrower

and

the

proposal.

You

know

looking

at

the

key

issues

and

cheap

key

risks

and

terms,

then

the

negotiate.

The

lender

will

negotiate

the

key

commercial

terms

in

legal

structure.

This

is

going

to

go

into

a

term

sheet

which

again

it's

signed

by

both

parties,

but

it's

more

just

an

indication

of

serious

interest.

It's

it's

not

really

legally

binding.

But

again

it's

a

reputational

thing.

C

C

Let's

go

document

the

key

commercial

and

legal

terms,

it's

probably

typically

three

to

20

pages,

so

there

can

be

a

fair

amount

of

depth

in

it.

If

both

parties,

you

know,

agree

to

it,

and

you

know

you're,

typically

not

going

to

produce

one

unless

you

think

you're

going

to

get

there,

then

it's

accepted

in

essence,

most

parties

sign

it.

The

lender

then

begins

to

do

confirmatory

diligence,

which

is

basically

just

trying

to

confirm

all

the

points.

You

know

that

they

think

is

true.

C

You

know

the

borrowers

presented

a

lot

of

things

and

said:

hey,

you

know.

Our

annual

loss

rates

are

four

percent

and

maybe

you've

seen

some

high-level

data,

but

typically

say

the

lender.

You

know,

might

actually

go

in

and

look

at

the

underlying

data

or

actually

might

probably

will

you

know,

maybe

even

get

it

audited.

So

if

the

borrower

says

it's

a

four

percent

loss

rate

and

the

audit

shows

it's

a

12

loss

rate,

you

could

lose

a

deal

like

that

right,

but

both

sides

are

usually

professional

and

try

to

be.

C

You

know,

open

and

up

front,

because

that's

a

bad

outcome

for

everyone.

Then

the

lenders

council

typically

starts

drafting

legal

documents.

This

is

expensive

right,

so

you

don't

want

to

start

this

step

until

you

think

you're

close

to

getting

there.

Then

the

parties

are

going

to

negotiate

the

remaining

items

in

the

legal

documents.

You

know

with

counsel

on

both

sides

and

even

though

the

term

sheet

might

be

20

pages

by

the

time

you're

done

with

these

transactions.

C

I

would

christian,

there's

probably

at

least

gonna,

be

four

or

five

documents

and

hundreds

and

hundreds

of

pages,

so

there's

lots

of

other

points

and

some

of

them

material

that

still

have

to

be

discussed.

Is

that

fair,

correct,

yeah?

And

so

there's

a

lot

there,

and

usually

it's

going

to

be

aimed

to

be

closing

this

within

90

days.

You

know

it's

just

you

you

want

to

drive

to

a

close.

You

want

a

sense

of

urgency.

C

You

know

sometimes

people

will

have

to

extend

it,

but

the

goal

is

you

know

to

really

get

this

thing

done

and

then

typically,

a

borrower

in

the

real

world

will

agree

to

an

exclusive

negotiation

period

with

the

lender,

because

if

you're

a

lender-

and

you

say,

look

if

everything

you

told

me

is

true

I'll

do

this

deal

at

these

proposed

terms.

You

don't

want

the

borrower,

then

doing

that

with

three

other

lenders

and

then

they

finally

get

to

the

last

minute.

You

know

and

they

say.

Oh

sorry,

we

have

a

better

deal.

C

So

it's

typically

a

lender's

gonna

want

that

kind

of

exclusive

period

for

say

three

months

and

again

it's

really

a

question

of

operating

in

good

faith.

You

know

and

there's

some

games

going

on

around

here,

but

I

I

typically

find

that

it's

just

better

to

work

party

with

parties

that

are

transparent

and

really

kind

of

follow

this

rough

process.

So

you

know

they're

reliable.

You

know

and

kind

of

a

game.

Theory

sense.

It's

not

just

one

transaction.

If

it's

just

one

transaction,

maybe

someone's

going

to

try

to

screw

you

as

much

as

they

can.

C

But

if

this

is,

if

you're,

probably

working

with

them

over

the

years,

you

know

you

understand

that

both

sides

need

to

have

something

to

make

sense,

and

you

really

should

treat

each

other

well,

because

you

want

to

preserve

a

valuable

long-term

relationship

next,

one,

please

all

right,

post

term

sheet

to

closing.

So

we've

already

started

talking

about

this.

Now,

how

do

you

get

to

closing

a

transaction

from

the

term

sheet?

You

know

the

lender.

C

Does

the

confirmatory

diligence

the

parties

complete

the

remaining

negotiating

items,

and

this

can

be

a

fair

amount

in

the

legal

documents?

The

lender's

counts.

Typically,

will

be

the

one

drafting

it.

You

know

the

lender

in

the

real

world.

This

is

centralized

likes

to

be

in

control

of

drafting

the

documents.

Why?

Because,

then

they

they

get

to

be

written

just

the

way

they

want

them.

C

That

really,

you

know,

addresses

the

risk

in

the

tightest

manner

they

you

know,

they're

comfortable

with

you

know

you

can

have

the

borrower

doing

the

documents,

but

it

just

it

makes

it

harder

if

you're

the

lander,

because

the

borrower

potentially

will

write

dozens

of

points

to

his

advantage,

and

you

know

you

might

have

to

go

back

to

all

many

many

many

points

and

say

no,

no,

no,

no,

no,

and

that

can

be

a

mess,

and

this

again,

needless

to

say,

presents

issues

and

decentralized

finance.

Whether

this

could

be

negotiation

or

not.

C

You

know

from

my

own

perspective

and

experience

a

borrower

writing

their

own

documents

without

really

an

active

kind

of

oversight

from

the

lender

is

just

a

it's

a

train

wreck

waiting

to

happen.

You

know,

there's

a

reason

why

it's

not

done

in

the

traditional

world.

I

personally

think

it's

an

exceptionally

good

way

to

lose

money

and

then

transactions

once

they

get

to

term

sheet.

I'd

say

more

often

than

not

close,

but

they

still

might

not.

Why

and

as

I've

already

hinted,

the

lender's

diligence

might

discover

some

important

undisclosed

risk.

C

You

know

say

the

one

of

the

owners

of

the

company

you

know

has,

like

you

know

some

criminal

conditions

on

fraud.

I've

seen

this

there's

lots

of

little

ways.

Things

can

go

sideways

or

the

borrower

and

the

lender

cannot

agree

on

some

open

points.

You

know

they

weren't

specified

in

the

term

sheet.

There

are

still

other

points

to

matter

and

you

try

to

get

those

up

front

at

the

beginning

of

the

term

sheet,

but

you

don't

always

cover

everything.

You

know

it's

just

it's

the

nature

of

the

process.

C

I

just

threw

down

like

off

the

top

of

my

head,

some

of

the

key

terms

and

transactions,

and

this

is

by

no

means

everything.

This

is

probably

maybe

five

percent.

I

don't

know

these

are

key

ones,

but

there's

so

many

more

so

so

I

really

want

people

just

to

think

when

you

do

a

structured

finance

transaction.

C

There's

many

many

important

terms.

You

know

with

that

or

material.

If

you

will,

let

me

give

you

a

quick

list

of

some

of

these.

You

know

how

big

is

the

loan?

How

long

is

the

loan?

What's

the

advance

rate,

you

know?

What's

the

interest

rate,

you

know

those

are

all

kind

of

obvious.

What's

the

credit

policy,

you

know,

how

did

they

decide

on

making

their

loans

to

if

it's

auto

lender,

you

know,

how

do

they

underwrite

people

are

they

allowed

to

approve

or

change

the

credit

policy

with

without

your

approval?

C

That

would

be

a

big

problem,

because

you

know

you

signed

up

to

them

doing

this

historically

and

they

say

oh,

we

certainly

want

to

do

a

whole

lot

more

risk

too.

You

know,

so

you

don't

want

them

to

be

able

to

change

it.

Materially

without

your

approval,

what's

the

servicing

policy,

you

know

how:

how

do

they

service

delinquent

assets?

You

know,

do

they

have

to

get

your

approval

to

amend

the

servicing

policy?

C

Do

they

need

a

backup

servicer?

How

need

how

does

the

underlying

loans

need

to

perform?

Are

there

triggers?

You

know

if

things

aren't

going

well

well,

where

are

the

triggers

what

levels

and

then,

if

the

triggers

are

hit

or

other

things

are,

you

know,

go

wrong

like

you

know

what

are

the

events

of

default

to?

Let

the

lender

come

in

and

shut

down

the

situation?

C

You

know

these

are

very

important.

You

know

when

things

go

sideways,

you

know

you

need

you

as

a

lender

want

to

be

able

to

come

in

and

get

control

of

the

collateral,

and

you

know

if

needed,

shut

things

down

and

liquidate.

There's

a

whole

lot

going

into

this

and

then

also

what

are

the

priority

of

payments.

C

You

know

who

gets

paid

when

in

your

typical

monthly

waterfall,

you

know

if

so,

every

month,

all

the

cash

from

the

loans

outstanding

comes

into

an

account

you

know

and

who's

getting

paid

when

very

important

does

the

originator.

You

know

write

reps

and

warranties

as

to

you

know

like

all

of

the

underlying

asset

loans

they

make,

are

actually

done

in

accordance

with

their

credit

policy.

You

know,

for

instance,

if

they

do

some

sloppy

things

that

are

out

of

policy,

they

should

be

expected

to

require

required

to

buy

them

back

at

par.

C

You

know

I

could

go

on

and

on

and

all

these

things

I

think

my

just.

I

want

to

make

the

point

that

there's

there's

so

many

important

elements

you

know

to

deal

with

here

and

I

I

kind

of

say

this

is

a

joke.

But,

let's

say

maker,

you

know

made

a

loan

to

christian

and

I

and

christian-

and

I

aren't

special

we're

just

experienced

the

maker-

got

his

top

20

or

30

terms,

and

we

got

to

figure

out

the

rest

of

the

terms

say

it's

a

billion

dollar

loan.

C

The

loan

would

perform.

You'd,

never

see

a

penny

back,

but

we

wouldn't

have

broken

it.

We

just

have

our

own

islands

and

be

very

comfortable,

not

because

we're

that

smart,

we

just

we've

been

in

this

long

enough.

You

know

how

to

carve

things

out

so

there's

so

many

ways

to

carve

out

risk

and

reallocate

it.

You

know

so

it

just

don't.

When

you

look

at

these

things,

don't

think

the

top

15

or

20

key

terms

are

enough.

C

A

And

eric,

I

would

just

add

on

this

particular

point-

I

mean

these

go

to

the

discussion

I

had

at

the

beginning

in

terms

of

negotiation

right

there

there

are,

you

know

tens

of

dozens,

hundreds

of

these

points

and

we

in

our

review

will

need

to

determine

whether,

for

instance,

the

events

of

default

are

the

market

which

ones

are

missing,

which

ones

maybe

should

we

have

given

that

the

borrower

is

borrowed

or

x?

What

are

the

peer

periods?

Are

there

any

cure

periods?

Are

they

too

long?

A

A

C

The

other

thing

I'd

say

is

like

again

think

of

my

auto

you're,

an

auto

lender.

We

think

of

making

a

loan.

You

know,

100

million

dollars

maker

does

to

the

auto

lender

and

they

give

us

100.

You

know

120

million

of

auto

loans,

the

kind

of

the

thought

experiment.

How

I

look

at

this

is

they

give

us

120

million

of

auto

loans,

and

we

put

a

corral

or

a

fence

around

it.

C

Then

the

question

is

think

of

every

way

we

could

lose

money

with

that

collateral,

deteriorating

or

slipping

out

of

the

fence.

So

most

of

what's

going

on

here

is:

how

do

you

make

sure

the

collateral

in

that

fence

is

what

they

tell

you?

It

is,

and

how

do

you

make

sure

it's

well

maintained

and

it

doesn't

leave

the

fence,

you

know

and

all

the

cash

from

it

goes

to

you

if

needed

and

on

one

hand

that's

pretty

intellectually

easy.

On

the

other

hand,

there's

a

lot

of

moving

parts

to

make

sure

that

happens.

C

That's

really

kind

of

probably

the

essence

of

the

structured

finance

game.

You

know

how

do

you

kind

of

identify

and

control

the

collateral?

That's

backing

your

loan,

you

know

it's

so

much

more

complicated

than

in

crypto

lending.

You

know,

crypto

lending,

you

know,

there's

a

real

beauty

of

being

able

to

take

wrapped

rap

btc.

You

know

into

our

vault,

you

know

liquidate

if

needed.

You

know

we

just

you,

don't

have

that

in

the

real

world,

so

yeah

next

slide.

Please!

C

Here's

just!

I

want

to

give

a

rough

sense

and

here's

some

off-market

transaction

examples

with

some

of

the

points

I've

made.

You

know

and

then

just

think

about

how

should

maker

be

dealing

with

these

potential

situations,

because

all

of

these

things

under

borrower

proposal

we

could

get

maker

could

get

asked

you

know,

and

how

does

it

want

to

be

able

to

decision

or

negotiate

these?

You

know

what

if

they

propose

a

billion

dollar

loan,

you

know

and

typically

the

market

might

give

them

100

million

because

they

never,

you

know,

done

more

than

50

million.

C

You

know

their

books,

you

know

maybe

60

million

and

they

could

grow

to

100

million

in

18

months.

You

know,

no

sane

lender

would

give

them

a

billion,

but

they

can

ask.

You

know

what

about

advance

rate,

as

I've

talked

about

early

on.

Maybe

they

asked

for

100

advance

rate

where

the

market's

more

80,

you

know

and

there's

good

reasons,

the

market's

80..

You

know

they

need

to

have

a

first

loss

position.

You

know

we're

not

their

equity,

typically

as

a

lender.

How

does

maker

want

to

address

that?

C

C

What

about

approving

changes

to

the

credit

policy

where

the

market

would

say?

Yes,

the

lender

has

to

approve

the

borrower

changing

their

credit

policy,

but

they

don't

want

to

approve.

It

won't

want

us

to

have

approval.

We

got

deals.

This

has

been

asked

what,

if

the

asset

performance

triggers,

are

pretty

loose

so

think

about

this.

You

got

all

your

loans

in

the

fence,

but

they

start

going

really

bad

before

the

lender

can

do

anything.

You

know.

Tighter

triggers

means

you

step

in

sooner

yeah.

We

certainly

get

proposed

weak

performance

triggers.

C

I

could

go

on

and

on

about

all

these,

but

there's

just

many

things.

They

can

propose

that

are

think

not

only

off

market

but

underneath

off

market.

What

does

it

mean

too?

It

typically

means

there's

a

higher

level

of

risk

there

you

know,

and

if

the

market

wouldn't

do

it

or

if

there's

a

higher

level

of

risk,

it'd

be

priced

differently.

C

C

A

Yeah,

so

this

is

really

just

a

slide

to,

I

think

summarize,

in

a

way

how

traffic

and

defy

on

board

an

asset

and

we've

covered

a

little

bit

of

it,

but

I

want

to

make

maybe

make

it

a

more

pointed

comparison.

You

know,

trap

by

institutions

have

a

structure,

very

well-defined

collateral,

onboarding

process.

We

have

a

mid-6

which

is

is

developing

into

a

structured

collateral,

onboarding

process,

but

yeah

frankly

we

haven't.

A

We

sort

of

do

right.

I

mean

there's

this

theory

for

cleaning.

There's

a

you

know,

theory

for

clean

money,

but

even

that

is

fairly

broad.

What

is

clean

money?

You

know

what

is

the

risk

tolerance

that

we're

prepared

to

accept

in

clean

money?

You

know,

would

clean

money,

for

instance,

and

then

I

spent

my

career

in

energy.

So

does

clean

money,

you

know,

involve

liquefied

natural

gas

because

it

will

reduce

coal

consumption

in

europe.

Well,

gases

and

methane.

A

You

know

is

clean.

Money

would

clearly

include

green

hydrogen,

but

you

know:

there's

not

been

a

green

hydrogen

project

implemented

on

a

project

finance

spaces

to

date.

So

there's

a

whole

bunch

of

technology

and

commercial

risk

is

that

a

risk

that

maker

would

be

prepared

to

accept

most

traffic

institutions

will

have

a

benchmark

in

which

they

can

review

transactions.

A

They

would

have

a

separate

business

development

team

that

initiates

the

engagements.

They

would

have

a

deal

team

that

performs

the

the

structuring

and

the

negotiation

of

the

transaction

and

then

ultimately,

they'll

have

an

investment

committee

that

has

kind

of

the

ultimate

decision

power

and

that

investment

committee

is

comprised

typically

of

senior

experienced

professionals

within

the

institution.

A

A

We

have

the

clean

money

thesis

there's

a

question

as

dsg.

What

is

the

esg?

It's

the

brainwashing

and

like

we

seem

to

be

investing

or

having

applicants

that

are

proposing

assets

and

highly

committed

highly

competitive

markets

like

the

us,

so

we're

competing

against

commercial

banks,

particularly

in

such

areas

of

solar

financing

and

another

green

financing.

A

You

know

we

want

to

use

market

type

of

structures

and

pricing

as

a

benchmark.

You

know,

I

think

what

is

clear

is

the

growth

core

unit

is,

is

undertaking

the

business

development

role

and

we

have

been

working

closely

with

the

growth

core

unit

to

really

give

them

an

idea

of

okay.

You

know

you

guys

are

the

business

development

folks,

here's

kind

of

some

of

the

things

you

need

to

be

looking

at,

because

that

has

typically

not

been

the

function

of

growth

or

unit

to

be

onboarding

real

world

assets.

A

A

I

think

there's

still

an

open

issue

as

to

the

role

of

real

world

finance

and

the

incubating

legal

transaction

services

core

unit

now

is

the

assessment

role.

Output

for

incomplete

map

commits

to

you

know

often

structuring

a

negotiation

as

needed

is

that

okay

is

the

community

on

board

that

the

real

world,

finance

and

lts

core

units

will

be

delegated

some

level

of

authority

to

structure

and

negotiate

transactions?

A

A

We

are

using

sessions

like

this

to

really

be

able

to

find

a

way

to

communicate

with

the

community

find

a

way

to

communicate

with

delegates.

Do

it

through

multiple

means

again,

some

people

adopt

information

or

absorb

information

better.

If

it's

in

writing

some

people

absorb

information

better.

If

it's

in

a

presentation,

if

it's

in

writing,

is

it

a

memo?

Is

it

a

slide?

A

You

know

we're

trying

to

find

our

way

to

really

be

able

to

support

the

delegates

and

the

community

and

the

decision

making

process.

So

it's

it's

a

continued.

It's

a

continual

process,

we're

not

perfect,

but

we

recognize

that

we

want

to

get

to

a

place

that

has

a

little

more

structure

and

give

the

community

and

delegates

confidence

that

there

is

a

structure

that

we're

following

next

slide.

A

So

then,

what

I'd

like

to

discuss

is

the

self-contained

mips

that

have

been

proposed

because,

frankly,

these

are

outside

of

the

process

that

we

have

been

actually

directly

contrary

to

the

process,

we've

been

trying

to

establish,

there's

nothing

wrong

with

a

self-contained

myth,

but

for

people

to

recognize

when

you're

seeking

to

develop

a

process

that

is

transparent.

That

is

efficient.

That

is

understood,

albeit

not

perfect,

yet

having

self-contained

met

with

a

prioritization

built

into

them

kind

of

throws

that

endeavor

a

bit

into

doubt.

A

So

several

of

the

recent

myths

have

sought

to

skip

to

step

five

of

the

caudal

onboarding

process

and

there's

a

link

specifically

there

to

what

step

5

says

and

step.

5

says

here

that

you

know:

domain

collateral

assessments

are

created

and

published

in

the

maker

forum,

while

awaiting

the

posting

of

a

governance

poll

in

the

following

monday.

A

We

are,

then,

the

various

teams

we

need

to

provide

an

in-depth

evaluation

of

the

collateral

type,

with

the

goal

of

the

assessment

to

provide